The Government, late on Friday night (!) before the school holidays, has issued a consultation on the formation of a new entity to help address housing affordability. The National Housing Finance and Investment Corporation is central to the Government’s plan for housing affordability.

Actually, this simply extends the “Financialisation of Property” by extending the current market led mechanisms, on the assumption that more is better. Financialisation is, as the recent UN report said:

… structural changes in housing and financial markets and global investment whereby housing is treated as a commodity, a means of accumulating wealth and often as security for financial instruments that are traded and sold on global markets.

So, we are not so sure. Also, we are not convinced housing supply problems have really created the sky-high prices and affordability issues at all. And, by the way, the UK, on which much of this thinking is based, still has precisely the same issues as we do, too much debt, too high prices, flat incomes, etc.

Anyhow, the Treasury consultation is open for a month. We will take a look at the three elements to the proposal:

- The National Housing Finance and Investment Corporation (NHFIC) – a new corporate Commonwealth entity dedicated to improving housing affordability;

- A $1 billion National Housing Infrastructure Facility (NHIF) which will use tailored financing to partner with local governments in funding infrastructure to unlock new housing supply; and

- An affordable housing bond aggregator to drive efficiencies and cost savings in the provision of affordable housing by community housing providers.

They argue that Australians’ ability to access secure and affordable housing is under pressure and that housing supply has not kept up with demand, particularly in our major metropolitan areas, contributing to sustained strong growth in housing prices. This is impacting the ability of Australians to purchase their first home or find affordable rental accommodation.

The average time taken to save a 20 per cent deposit on a house in Sydney has grown from five to eight years in the past decade, while the time taken to save a similar deposit in Melbourne has grown from four to six years over the same period. Half of all low-income rental households in Australia’s capital cities spend more than 30 per cent of their household income on housing costs. Meanwhile, across Australia, community housing providers (CHPs) currently provide 80,000 dwellings to low-income households at sub-market rates, and around 40,000 Australians are currently on waiting lists for community housing and an additional 148,000 are on public housing waiting lists.

The National Housing Finance and Investment Corporation is central to the Government’s plan for housing affordability

In the 2017–18 Budget, the Government announced a comprehensive housing affordability plan to improve outcomes across the housing continuum, focused on three key pillars: boosting the supply of housing and encouraging a more responsive housing market, including by unlocking Commonwealth land; creating the right financial incentives to improve housing outcomes for first-home buyers and low-to-middle-income Australians, including through the Government’s First Home Super Saver scheme; and improving outcomes in social housing and addressing homelessness, including through tax incentives to boost investment in affordable housing.

The Government’s plan includes establishing:

- the National Housing Finance and Investment Corporation (NHFIC) — a new corporate Commonwealth entity dedicated to improving housing affordability;

- a $1 billion National Housing Infrastructure Facility (NHIF) which will use tailored financing to partner with local governments (LGs) in funding infrastructure to unlock new housing supply; and

- an affordable housing bond aggregator to drive efficiencies and cost savings in CHP’s provision of affordable housing.

These measures are important but can only go so far in improving housing affordability. As noted by the Affordable Housing Working Group (AHWG), further reforms to increase the supply of housing more broadly have the capacity to improve housing affordability and alleviate some of the pressure on the community housing sector. To this end, they would be complemented by the development of a new National Housing and Homelessness Agreement with an increased focus on addressing housing affordability.

The Government’s objectives for the NHFIC reflect its priorities to improve affordable housing outcomes for Australians. The NHFIC intends to grow the community housing sector, and increase and accelerate the supply of housing where it is needed most.

Governance of the National Housing Finance and Investment Corporation

Entity structure – The NHFIC is expected to be established through legislation as a corporate Commonwealth entity. It will be a body corporate that has a separate legal personality from the Commonwealth, but will be subject to an investment mandate prescribed by the Treasurer that reflects the Government’s objective of improving housing outcomes. It is currently envisaged that both the NHIF and the affordable housing bond aggregator functions would be established as separate business lines within the single corporate entity. The final structure of the NHFIC will be determined in accordance with the Commonwealth Governance Structures Policy administered by the Department of Finance. The Governance Structures Policy provides an overarching framework to ascertain fit-for-purpose governance structures for all entities established by the Government. The NHFIC Board may also engage third-party providers with the requisite expertise to provide treasury, loan administration and other back-office support for its bond aggregator and/or NHIF business lines.

NHFIC Board

The Government intends to appoint an independent, skills-based Board to govern the NHFIC. Board members are expected to be selected by the Government on the basis of expertise in finance, law, government, housing, infrastructure and/or public policy. The Board will be responsible for the entity’s corporate governance, overseeing its affairs and operations. This includes establishing a corporate governance strategy, defining the entity’s risk appetite, monitoring performance and making decisions on capital usage. The Board will be responsible for ensuring that investment decisions made for the NHIF and the bond aggregator comply with the NHFIC investment mandate. The Board will also ensure that the NHFIC is governed according to best-practice corporate governance principles for financial institutions, including compliance with the Public Governance, Performance and Accountability Act 2013 (PGPA Act).

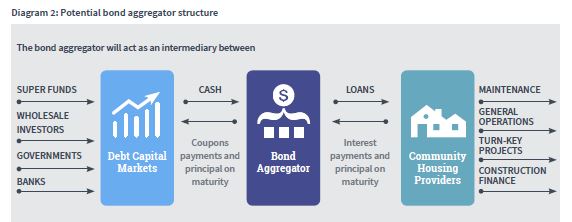

The affordable housing bond aggregator

The NHFIC will also operate an affordable housing bond aggregator designed to provide cheaper and longer-term finance to CHPs. CHPs are an important part of the Australian housing system. They provide accommodation services for social housing, managing public housing on behalf of state and territory governments. They also own their own stock of housing, which they offer to eligible tenants at below market rents. CHP tenants range from people on very low incomes with rents set at a proportion of their income (generally 25 to 30 per cent) to tenants on low to moderate incomes with rents set below the relevant market rates (usually set at 75 to 80 per cent of market rents).

Many CHPs (over 300) are registered either under the National Regulatory System for Community Housing (NRSCH) or other state and territory regulatory regimes (which is the case in Victoria and Western Australia).

Although the community housing sector has grown over recent years, it remains relatively small at around 80,000 properties (less than 1 per cent of all residential dwellings) in 2016. This is compared to more than 2.8 million properties (around 10 per cent of all residential dwellings) in the United Kingdom in 2015. There are substantial barriers to the community housing sector achieving the scale and capability necessary to meet current and future demand for affordable rental accommodation. These include the fragmentation of the sector, its limited financial capability (including the degree of financial sophistication), and the funding gap — the inability of sub-market rental revenues to cover the costs of providing affordable housing — which constrains the extent of services that CHPs can offer.

Bond aggregator model

The bond aggregator aims to assist in addressing the financing challenge faced by the CHP sector. It improves efficiency and scale by aggregating the lending requirements of multiple CHPs and financing those requirements by issuing bonds to institutional investors. The bond aggregator will act as an intermediary between CHPs and wholesale bond markets, raising funds on behalf of CHPs at potentially lower cost and over a longer term than traditional bank finance (which generally offer three to five-year loan terms). This structure will provide CHPs with a more efficient source of funds, reduce the refinancing risk faced by CHPs and will reduce their borrowing costs. This should enable CHPs to invest more in providing social and affordable rental housing.

However, the bond aggregator alone will not close the funding gap experienced by CHPs. This will require ongoing support from all levels of government. In their respective reports, the AHWG15 and Ernst and Young (EY) both highlight the important role of the bond aggregator, while noting that it is only a partial solution to closing the funding gap for CHPs.

Key findings of the EY report

Analysis undertaken by EY for the Affordable Housing Implementation Taskforce in 2017 found that an affordable housing bond aggregator is a viable prospect in the Australian context and recommended a number of design features. EY found that a bond aggregator could potentially provide longer tenor and lower cost finance to CHPs. The interest savings could be in the order of 0.9 to 1.4 percentage points for 10-year debt (depending on the level of Government support).

Furthermore, EY estimated that the CHP sector will need to access around $1.4 billion of debt over the next five years, which should provide the necessary demand and scale needed to support affordable housing bond issuances.

One thought on “Government Consults on National Housing Finance and Investment Corporation”