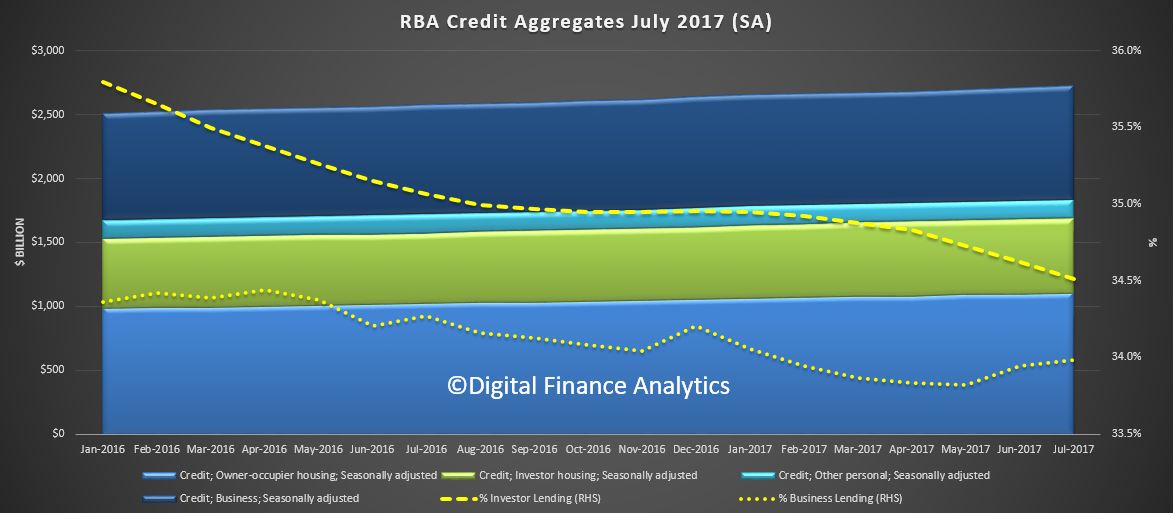

The RBA Credit Aggregates for July 2017 have been released. Overall credit rose by 0.5% in the month, or 5.3% annualised. Within that housing lending grew at 0.5% (annualised 6.6% – well above inflation), other Personal credit fell again, down 0.1% (annualised -1.4%) and business credit rose 0.5% (annualised 4.2%).

Home lending reached a new high at $1.689 trillion. Within that owner occupied lending rose $7 billion to $1.10 trillion (up 0.48%) and investor lending rose just $0.09 billion or 0.15% to $583 billion. Investor mortgages, as a proportion of all mortgages fell slightly.

Home lending reached a new high at $1.689 trillion. Within that owner occupied lending rose $7 billion to $1.10 trillion (up 0.48%) and investor lending rose just $0.09 billion or 0.15% to $583 billion. Investor mortgages, as a proportion of all mortgages fell slightly.

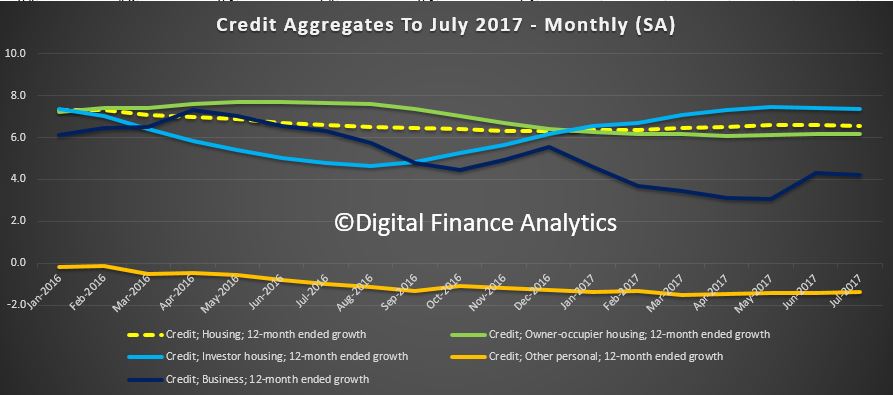

The adjusted movement data shows that investor housing is still at around 7%, higher than owner occupied loans and still way too high. Personal credit continues to languish, while business lending remains at around 4%. All growth rates for the financial aggregates are seasonally adjusted, and adjusted for the effects of breaks in the series

The adjusted movement data shows that investor housing is still at around 7%, higher than owner occupied loans and still way too high. Personal credit continues to languish, while business lending remains at around 4%. All growth rates for the financial aggregates are seasonally adjusted, and adjusted for the effects of breaks in the series

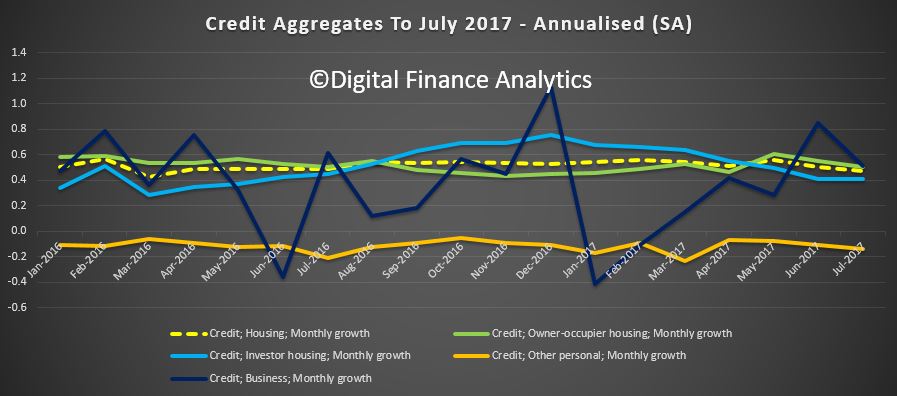

The more volatile monthly data shows a slight easing in housing credit growth this month, and a fall this month in business lending.

The more volatile monthly data shows a slight easing in housing credit growth this month, and a fall this month in business lending.

The RBA notes that:

The RBA notes that:

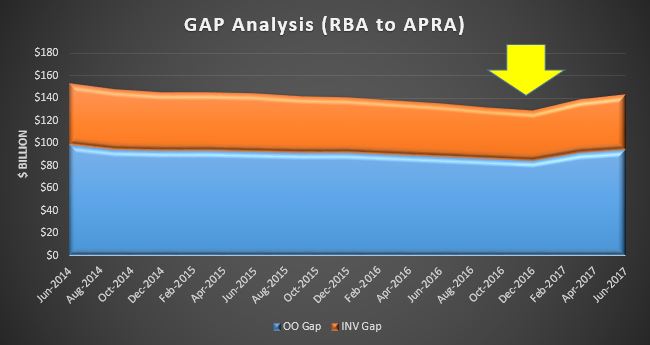

Following the introduction of an interest rate differential between housing loans to investors and owner-occupiers in mid-2015, a number of borrowers have changed the purpose of their existing loan; the net value of switching of loan purpose from investor to owner-occupier is estimated to have been $56 billion over the period of July 2015 to July 2017, of which $1.4 billion occurred in July 2017. These changes are reflected in the level of owner-occupier and investor credit outstanding. However, growth rates for these series have been adjusted to remove the effect of loan purpose changes.

So more adjustments, either from mis-classification, or borrowers proactively switching from investment loans to get better rates. This rate of switching has not slowed down, so it looks like a continuing process rather than a clerical error.

We suspect non-banks are picking up some of the investor lending slack as ADI’s conform to the regulators guidance. A quick calculation, comparing RBA and APRA data provides some validation:

2 thoughts on “Home Lending Reaches Another Record”