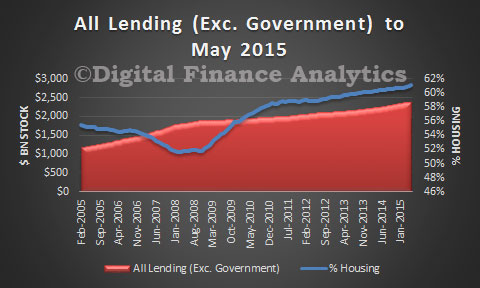

The RBA lending aggregates for May 2015 tell the ongoing story of housing lending dominated by investment loans, and housing becoming an ever larger proportion of total bank debt. Total bank lending stock grew to $2.4 trillion in May, with $1.47 trillion in housing, growing at 0.42% in the month, business lending up 0.35% to $792 million and personal lending (excluding housing) down a little to $141 million. Overall housing lending was 61.1% of all bank lending (excluding government loans) – an all time high.

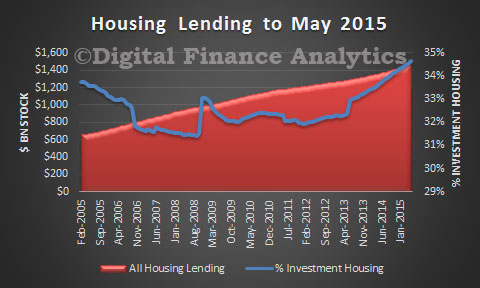

Looking more closely at housing, the $1.47 trillion was split into owner occupied lending of $958 million, up 0.42% in the month, and investment lending of $508m, up 0.81%, showing again the disproportionate focus on investment property.

Looking more closely at housing, the $1.47 trillion was split into owner occupied lending of $958 million, up 0.42% in the month, and investment lending of $508m, up 0.81%, showing again the disproportionate focus on investment property.

We can but reiterate our two key points. First, housing lending is squeezing out productive lending to business, and in so doing continues to inflate banks balance sheets, and house prices, neither productive economically speaking; whilst business finds it hard to get the support it needs to create productive growth. In the context of a mining slow down, this is a serious problem, which will not be addressed by $20k capital write-offs. Capital rules favour home lending too much.

We can but reiterate our two key points. First, housing lending is squeezing out productive lending to business, and in so doing continues to inflate banks balance sheets, and house prices, neither productive economically speaking; whilst business finds it hard to get the support it needs to create productive growth. In the context of a mining slow down, this is a serious problem, which will not be addressed by $20k capital write-offs. Capital rules favour home lending too much.

Second, the distortions created by ever larger bands of property investors, makes it harder for younger families to buy a home – indeed many are going direct to the investment sector in a bid to get a look in. However, those who analyse relative risks in an investment portfolio versus an owner occupied portfolio indicate there are higher risks in the investment pools, especially in a down turn. These risks are not recognised by the current Basel rules, and such risks are not currently priced into investment loans.

The data so far does not demonstrate any impact from the “tighter” APRA rules for investment lending, maybe next month? Even if one or two banks slow their investment lending growth rates and tighten their underwriting criteria, others will happily step in.