The latest monthly banking statistics for July 2017 from APRA are out. It reconfirms that growth in the mortgage books of the banks is still growing too fast. The value of their mortgage books rose 0.63% in the month to $1.57 trillion. Within that, owner occupied loans rose 0.73% to $1,017 billion whilst investor loans rose 0.44% to $522 billion.

Investor loans were 35.18% of the portfolio.

Investor loans were 35.18% of the portfolio.

![]() The monthly growth rates continues to accelerate, with both owner occupied and investor loans growing (despite the weak regulatory intervention). On an annual basis owner occupied loans are 6.9% higher than a year ago, and investor loans 4.8% higher. Both well above inflation and income growth, so household debt looks to rise further. The remarkable relative inaction by the regulators remains a mystery to me given these numbers. Whilst they jawbone about the risks of high household debt, they are not acting to control this growth.

The monthly growth rates continues to accelerate, with both owner occupied and investor loans growing (despite the weak regulatory intervention). On an annual basis owner occupied loans are 6.9% higher than a year ago, and investor loans 4.8% higher. Both well above inflation and income growth, so household debt looks to rise further. The remarkable relative inaction by the regulators remains a mystery to me given these numbers. Whilst they jawbone about the risks of high household debt, they are not acting to control this growth.

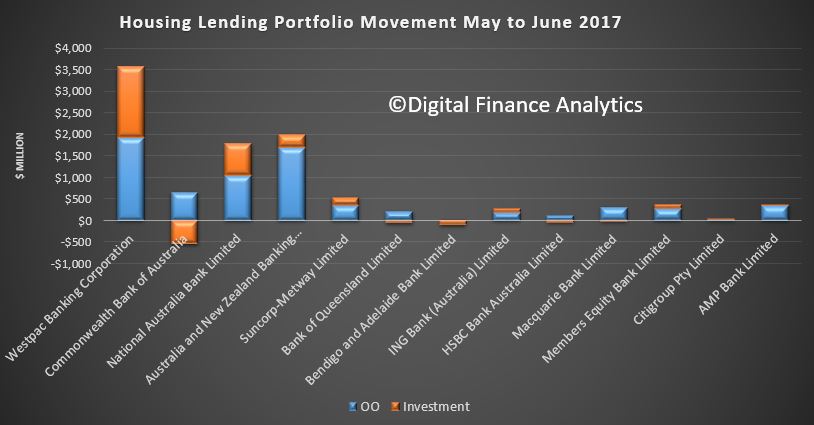

Looking at individual lenders, there was no change in the overall ranking by share.

But interestingly, we see significant variations in strategy working through to changes in the majors month on month portfolio movements.

But interestingly, we see significant variations in strategy working through to changes in the majors month on month portfolio movements.

ANZ has focussed on growing its owner occupied book, WBC is still in growth mode on both fronts, whilst CBA dropped their investor portfolio. We also saw a number of smaller lenders expand their books.

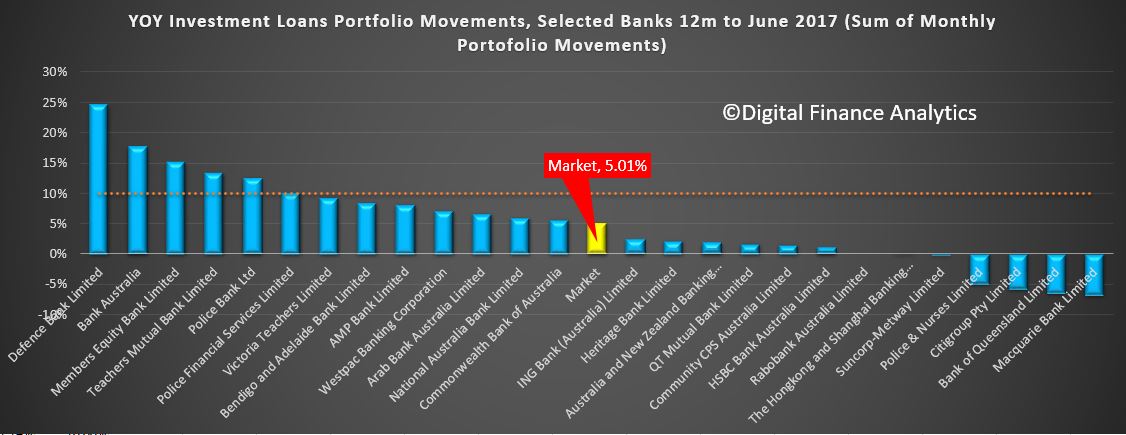

Looking at the speed limit on investor loans – 10% is too high -we see the investor market at 5% (sum of monthly movements), with all the majors well below the limit. But some smaller players are still growing faster.

Looking at the speed limit on investor loans – 10% is too high -we see the investor market at 5% (sum of monthly movements), with all the majors well below the limit. But some smaller players are still growing faster.

We have to conclude one of two things. Either the regulators are not serious about slowing household debt growth, and the recent language is simply lip service (after all the strategy has been to use households as the growth engine as the mining sector faded), or they are hoping their interventions so far will work though, given time. Well given the recent auction results (still strong) and the loan growth (still strong) we do not believe enough is being done. Time is not their friend.

We have to conclude one of two things. Either the regulators are not serious about slowing household debt growth, and the recent language is simply lip service (after all the strategy has been to use households as the growth engine as the mining sector faded), or they are hoping their interventions so far will work though, given time. Well given the recent auction results (still strong) and the loan growth (still strong) we do not believe enough is being done. Time is not their friend.

Indeed, later this week we will release our mortgage stress update. We suspect households will continue to have debt issues, and this will be exacerbated by interest rate rises in a flat income, high cost growth scenario many households are facing. The bigger the debt burden, the longer it will be to work through the system, with major economic ramifications meantime.

The RBA data will be out later, and we will see if there have been more loans switched between category, and whether non-banks are also growing their books. Both are likely.

One thought on “Home Loans Still Rising Too Fast”