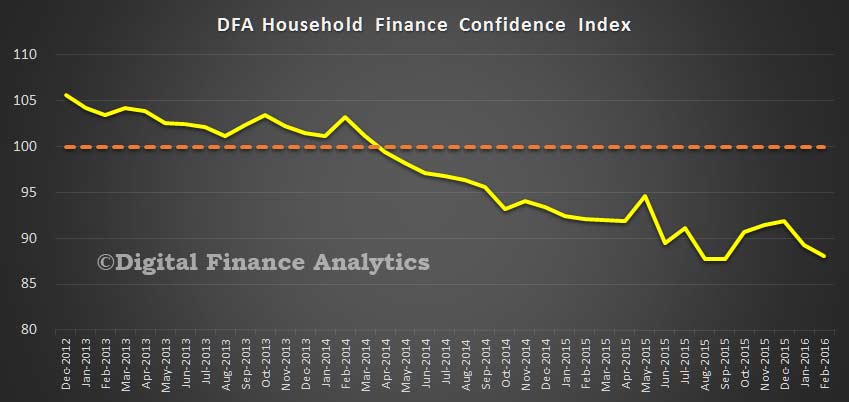

The February edition of the Digital Finance Analytics Household Finance Confidence Index, released today, fell from 89.24 to 88.11, and remains below a neutral setting.

A range of factors have led to this latest fall.

A range of factors have led to this latest fall.

Savings was one area of concern, because with stronger concerns about the property sector, and volatile stock markets, more households are wanting to hold money on deposit. 11% feel more comfortable than 12 months ago, 31% less conformable, and 52% about the same. The research shows that many households are concerned about the best investment path, and some are expecting savings rates to fall further. We also saw that about one quarter of households would have difficulty in accessing savings of $2,500 in an emergency, so savings balances are highly segment specific. Deposit rates have also improved recently for some.

On the debt front, 8% of households feel more comfortable than a year back, down 2.5%, whilst 27% are less comfortable, (up 1.8%). 62% felt about the same. Mortgages remain the major burden, whilst more are looking to pay down credit card debt. Significantly a rising number of households indicated they were considering paying down debt (rather than keeping funds in a low yielding deposit account). Perhaps the era of deleveraging is starting? Whilst new borrowing for property purchase is somewhat down, refinancing to reduce existing repayments has increased. There was a significant rise in households whose loan application was refused on serviceability grounds.

Turning to real income (after inflation), only 1.2% of households said their income had risen (down 1%), whilst 44% said their real incomes had fallen in the past year (consistent with recent RBA data showing no per capita growth since 2008). More than half said they had experienced no change in real income. Those relying on investments for incomes were most concerned. The lack of income growth constrains household spending and will reduce their ability to deleverage.

Looking at costs of living, 37% said their costs had risen in the past year, 2% said costs have fallen, and 59% said there was little net change, thanks to continued lower fuel and interest costs offsetting other rising costs. School fees and childcare costs, and health insurance costs all rose.

On a positive note, more households are confident of their employment now, with 14.14% feeling more secure than 12 months ago, up from last month, whilst 20% were feeling less secure (but down 1.73%). The majority said there has been no change (62.2%).

Summing up, household net worth is now under more pressure, with 51% said it had risen (down 4%), 15% saying net worth was lower (up 2.8%), and 26% saying there was no change. The value of some share market investments are being trimmed. We are also seeing some signs of property values falling in some places. For example, property in areas of Kalgoorlie (WA) have fallen 25% in the past year, some areas around Mackay and Fitzroy (QLD) have fallen 20%, and in SA areas around Eyre dropped 6%. Not all property markets across Australia have performed equally well. These factors feed into the falls in net worth.

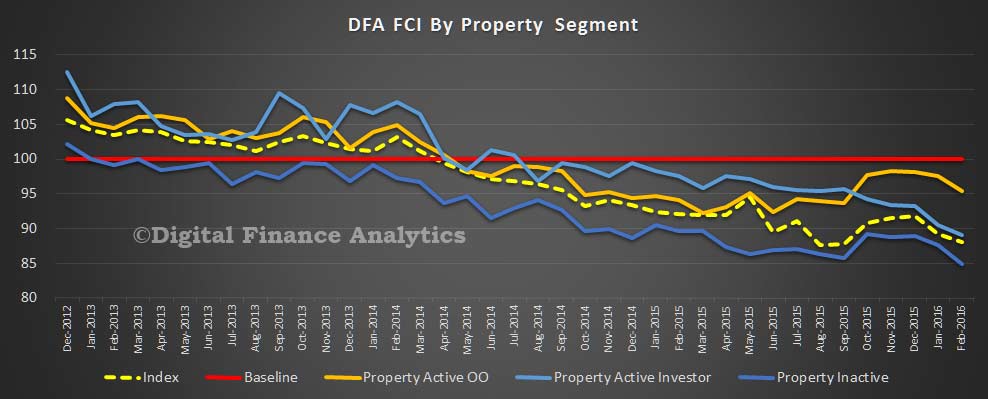

Finally, looking at a property segmented view of the index, we see that all segments recorded a fall this month, with property active owner occupied households more positive than property investors, and property inactive households (in rentals or other living arrangements) scoring the most negative results. Factors such as prospective tax changes in the budget, general political uncertainty, and the broader economic environment are all playing on households, feeding through into ongoing negativity. Significantly, the boost we saw following the change in PM has now dissipated completely.

By way of background, these results are derived from our household surveys, averaged across Australia. We have 26,000 households in our sample at any one time. We include detailed questions covering various aspects of a household’s financial footprint. The index measures how households are feeling about their financial health. To calculate the index we ask questions which cover a number of different dimensions. We start by asking households how confident they are feeling about their job security, whether their real income has risen or fallen in the past year, their view on their costs of living over the same period, whether they have increased their loans and other outstanding debts including credit cards and whether they are saving more than last year. Finally we ask about their overall change in net worth over the past 12 months – by net worth we mean net assets less outstanding debts.

By way of background, these results are derived from our household surveys, averaged across Australia. We have 26,000 households in our sample at any one time. We include detailed questions covering various aspects of a household’s financial footprint. The index measures how households are feeling about their financial health. To calculate the index we ask questions which cover a number of different dimensions. We start by asking households how confident they are feeling about their job security, whether their real income has risen or fallen in the past year, their view on their costs of living over the same period, whether they have increased their loans and other outstanding debts including credit cards and whether they are saving more than last year. Finally we ask about their overall change in net worth over the past 12 months – by net worth we mean net assets less outstanding debts.

One thought on “Household Finance Confidence Falls Again In February”