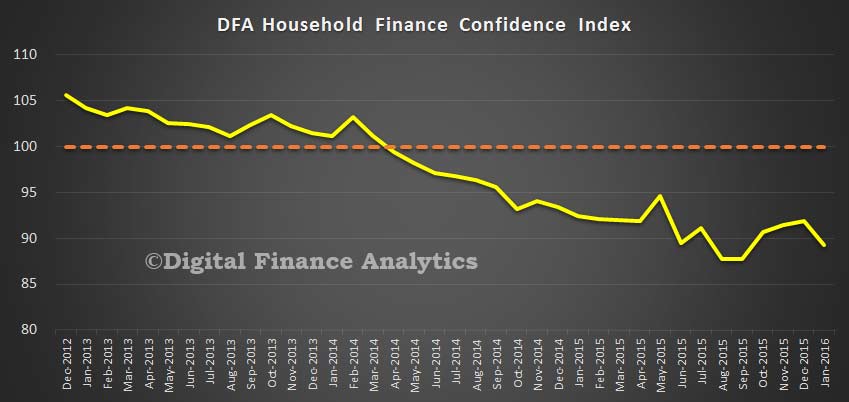

In the latest edition of the DFA Household Finance Confidence Index, to end January 2016, we see a marked fall in overall confidence, down from 91.46 to 89.24. This reverses the improvement we saw in the last quarter of 2015. Households with investment property and stock market investments registered the strongest declines. Those in WA and SA also showed greater concerns about future job prospects compared with eastern states. Confidence continues to languish below the neutral setting of 100.

The results are derived from our household surveys, averaged across Australia. We have 26,000 households in our sample at any one time. We include detailed questions covering various aspects of a household’s financial footprint. The index measures how households are feeling about their financial health. To calculate the index we ask questions which cover a number of different dimensions. We start by asking households how confident they are feeling about their job security, whether their real income has risen or fallen in the past year, their view on their costs of living over the same period, whether they have increased their loans and other outstanding debts including credit cards and whether they are saving more than last year. Finally we ask about their overall change in net worth over the past 12 months – by net worth we mean net assets less outstanding debts.

The results are derived from our household surveys, averaged across Australia. We have 26,000 households in our sample at any one time. We include detailed questions covering various aspects of a household’s financial footprint. The index measures how households are feeling about their financial health. To calculate the index we ask questions which cover a number of different dimensions. We start by asking households how confident they are feeling about their job security, whether their real income has risen or fallen in the past year, their view on their costs of living over the same period, whether they have increased their loans and other outstanding debts including credit cards and whether they are saving more than last year. Finally we ask about their overall change in net worth over the past 12 months – by net worth we mean net assets less outstanding debts.

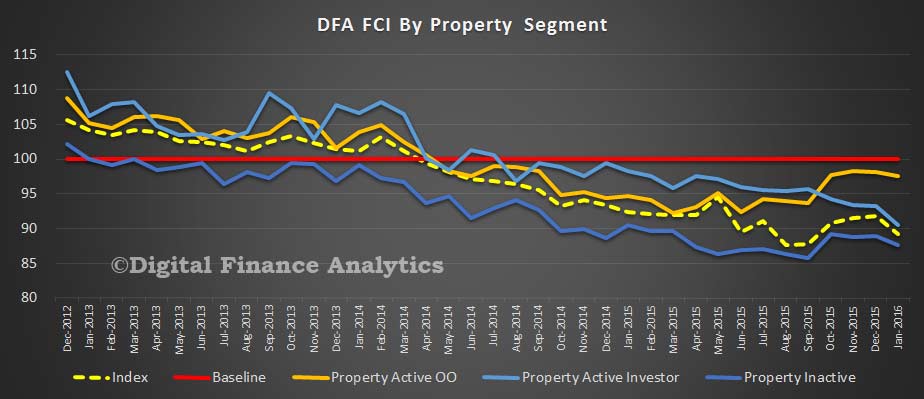

Looking specifically at our property segmentation, we see a significant decline in confidence among property investors. There are two factors driving this, first rental income is constrained, and second prospective future capital growth is uncertain. In addition, concerns about potential adverse changes to negative gearing are also having an impact. Owner occupied property holders remain relatively more positive, thanks to continued low interest rates, and with little expectation of any rise in rates anytime soon.

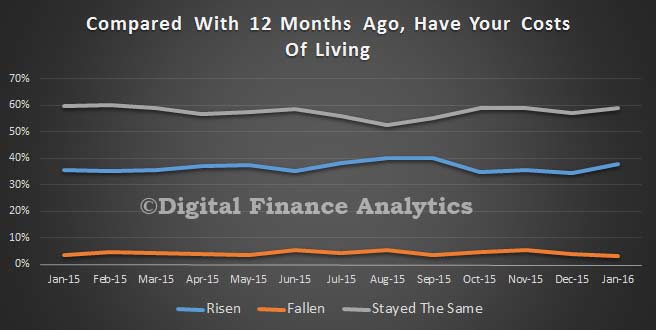

Looking at the moving parts which drive the index, costs of living continue to rise in real-terms, with 38% saying costs have risen in the past year, (up 3% from last month), whilst 58% said there had been no overall change (falls in fuel costs netting off other elements).

Looking at the moving parts which drive the index, costs of living continue to rise in real-terms, with 38% saying costs have risen in the past year, (up 3% from last month), whilst 58% said there had been no overall change (falls in fuel costs netting off other elements).

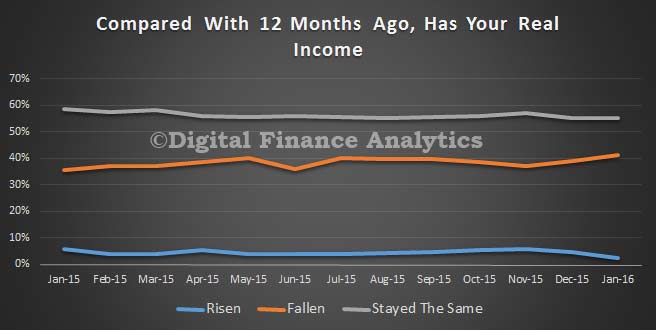

Turning to income growth, 2.3% said, in real terms (after inflation) their incomes had risen in the past year, (down 2.4% from last month), whilst 55% said there had been no net change. 41% said their income had fallen, thanks to lower investment returns, reduced overtime, and less available work. The figures varied across the states, but we won’t discuss that here.

Turning to income growth, 2.3% said, in real terms (after inflation) their incomes had risen in the past year, (down 2.4% from last month), whilst 55% said there had been no net change. 41% said their income had fallen, thanks to lower investment returns, reduced overtime, and less available work. The figures varied across the states, but we won’t discuss that here.

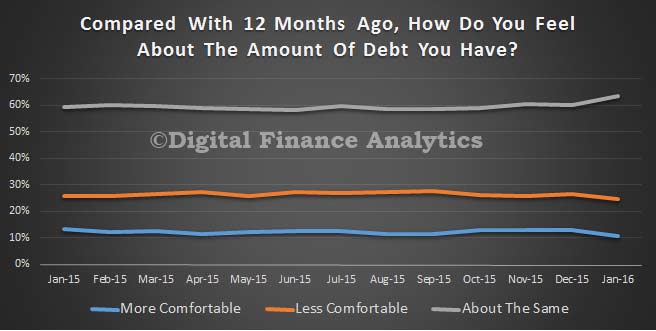

Turning to debt levels (and household debt has never been higher), 11% of household were more comfortable than a year ago (down 2% from last month), 25% were less comfortable, and 63% were about the same. Continuing low interest rates are helping to make large loans manageable.

Turning to debt levels (and household debt has never been higher), 11% of household were more comfortable than a year ago (down 2% from last month), 25% were less comfortable, and 63% were about the same. Continuing low interest rates are helping to make large loans manageable.

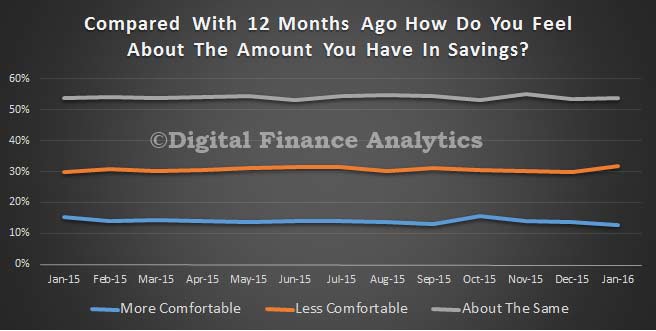

Next we look at savings. 13% of households were more comfortable with their savings than a year ago, (down 1% from last month), whilst 32% were less comfortable, mainly due to their inability to save, or for those who can, the low returns currently on offer.

Next we look at savings. 13% of households were more comfortable with their savings than a year ago, (down 1% from last month), whilst 32% were less comfortable, mainly due to their inability to save, or for those who can, the low returns currently on offer.

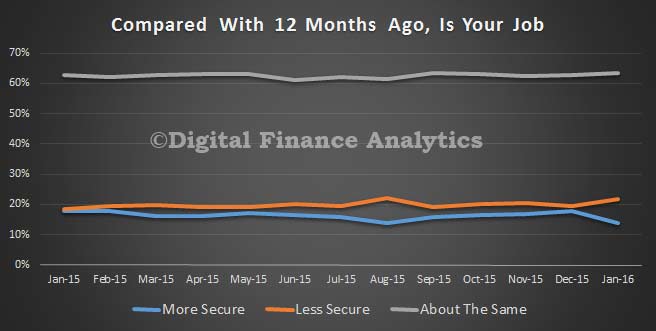

Job security varied across the states, but at an aggregated level, 14% felt more secure than a year ago, 54% felt about the same, and 32% felt less secure (up 2.5% from last month). Those in resources, and manufacturing were on average less comfortable, compared with those in the service sectors. Continued drought conditions in some areas also had an adverse impact.

Job security varied across the states, but at an aggregated level, 14% felt more secure than a year ago, 54% felt about the same, and 32% felt less secure (up 2.5% from last month). Those in resources, and manufacturing were on average less comfortable, compared with those in the service sectors. Continued drought conditions in some areas also had an adverse impact.

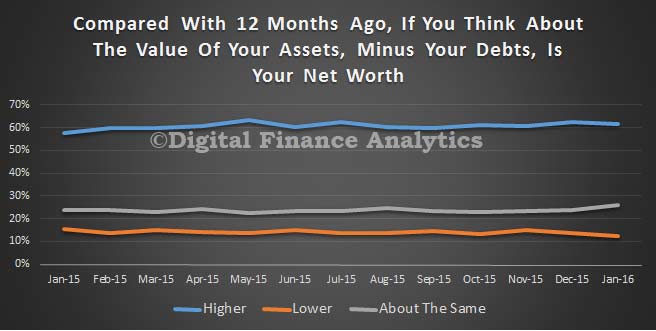

Finally, we look at net worth. Here 61% of households said their net worth was higher than a year ago (down 1% from last month), whilst 26% said there was no change, and 13% said their net worth was lower. Those with property assets are protected by the rapid rises in the past year, even if future growth is less certain. Those with stock market investments are more concerned by recent falls.

Finally, we look at net worth. Here 61% of households said their net worth was higher than a year ago (down 1% from last month), whilst 26% said there was no change, and 13% said their net worth was lower. Those with property assets are protected by the rapid rises in the past year, even if future growth is less certain. Those with stock market investments are more concerned by recent falls.

So, overall households remain concerned, and this will translate into cautious spending patterns in coming months. Given continued uncertainly on global markets, property price dynamics, and the upcoming budget in May, we do not expect much of a recovery in confidence in the short term.

So, overall households remain concerned, and this will translate into cautious spending patterns in coming months. Given continued uncertainly on global markets, property price dynamics, and the upcoming budget in May, we do not expect much of a recovery in confidence in the short term.

One thought on “Household Finance Confidence Takes A Dive”