The RBA credit aggregates for May 2017 show continued growth in housing lending, whilst business investment remains anemic.

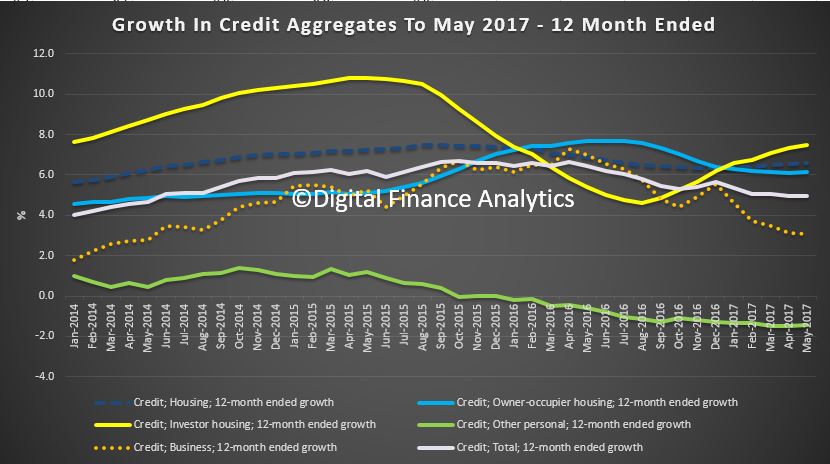

The adjusted 12 month growth trends tells it all. Investment loans still running ahead of owner occupied lending, business credit slowing and other personal lending falling. Total credit grew 5% in the year (compared with 6.4% last year), Housing credit grew at 6.6%, compared with 6.9% a year ago, and business credit grew at 3.1% compared with 7% a year ago. These are worrying trends, and makes future economic growth less certain. However, bank profits will be bolstered thanks to ongoing mortgage growth, and the benefit of the recent mortgage repricing, under the alibi of regulatory pressure. Just remember households have to repay this debt at some point, and interest rates will grind higher. Risks continue to rise.

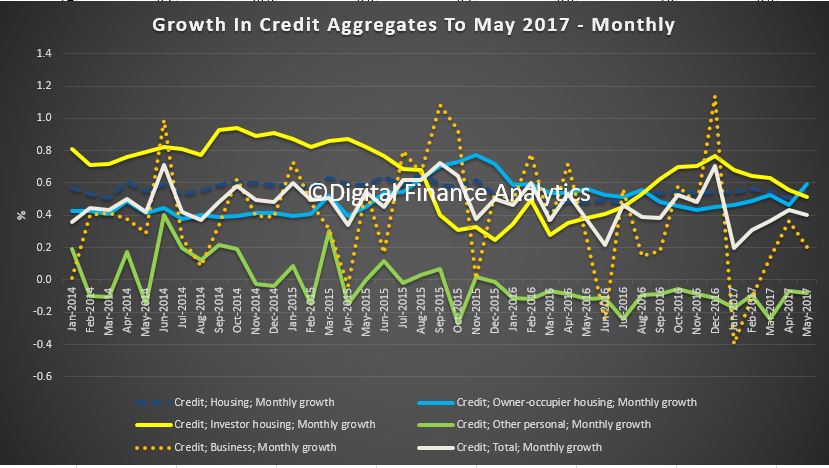

The more noisy, monthly series shows housing grew at 0.6% compared with 0.5% last month, whilst business grew 0.2% compared with 0.4% last month.

The more noisy, monthly series shows housing grew at 0.6% compared with 0.5% last month, whilst business grew 0.2% compared with 0.4% last month.

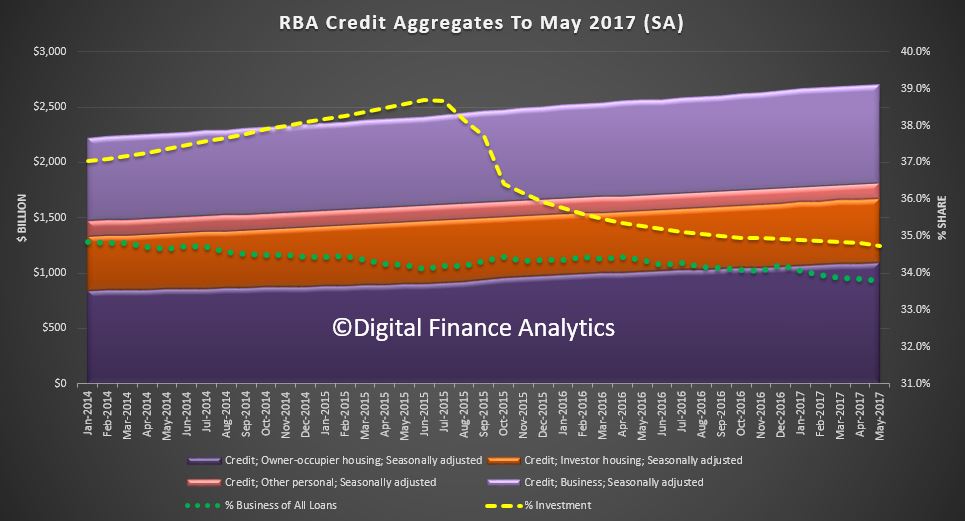

Growth in the aggregates show the proportion of investment loans fell just a little, while business lending as a proportion of all lending fell again.

Growth in the aggregates show the proportion of investment loans fell just a little, while business lending as a proportion of all lending fell again.

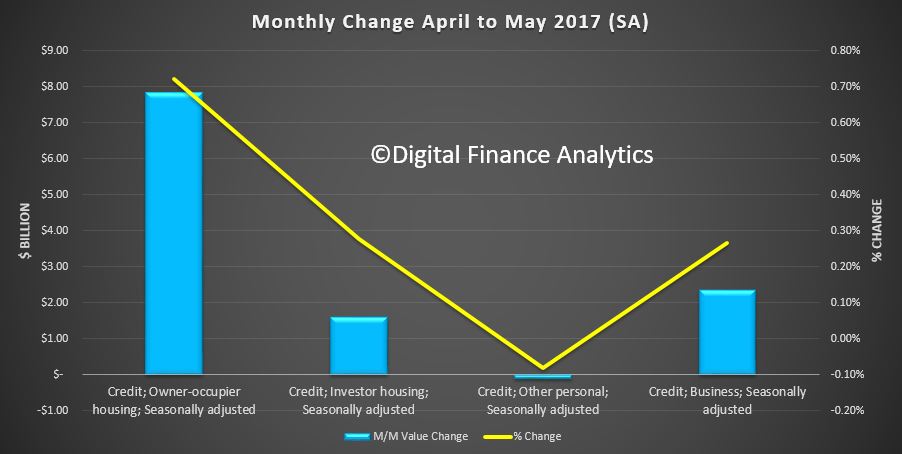

Here are the month on month moves. Owner occupied lending rose $7.8 billion (0.72%) and investment lending rose $1.6 billion (0.28%), both seasonally adjusted.

Here are the month on month moves. Owner occupied lending rose $7.8 billion (0.72%) and investment lending rose $1.6 billion (0.28%), both seasonally adjusted.

The RBA says more loans – $1.4 billion – were switched from investment to owner occupied loans, so the true state of play remains uncertain. $53 billion switched is a big number.

The RBA says more loans – $1.4 billion – were switched from investment to owner occupied loans, so the true state of play remains uncertain. $53 billion switched is a big number.

Following the introduction of an interest rate differential between housing loans to investors and owner-occupiers in mid-2015, a number of borrowers have changed the purpose of their existing loan; the net value of switching of loan purpose from investor to owner-occupier is estimated to have been $53 billion over the period of July 2015 to May 2017, of which $1.4 billion occurred in May 2017. These changes are reflected in the level of owner-occupier and investor credit outstanding. However, growth rates for these series have been adjusted to remove the effect of loan purpose changes.

It also appears the non-bank sector is growing (take the RBA aggregate from the APRA number earlier reported). $1.67 billion, less $1.56 billion = 0.11 trillion.

2 thoughts on “Housing Lending Reached A Dizzy $1.67 Trillion In May”