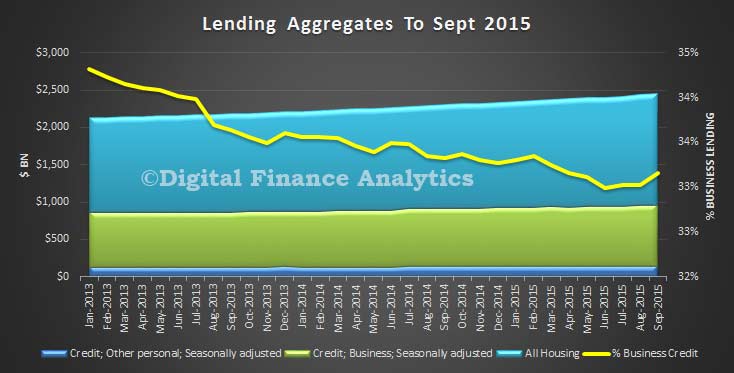

The RBA credit aggregates for September shows that overall credit (excluding to government) rose by 0.75% to $2,459 bn. Within that, lending for housing rose 0.68% in the month to $1,495 bn, yet another record, representing an annual rise of 7.5%. Lending to business rose 1.18% t0 $815 bn, representing just 33.2% of all lending – still at the lower end of the range showing business is still not that eager to borrow. Annual growth was 6.3%. Personal credit fell by 0.83% to $148 bn, an annual rate of 0.5%.

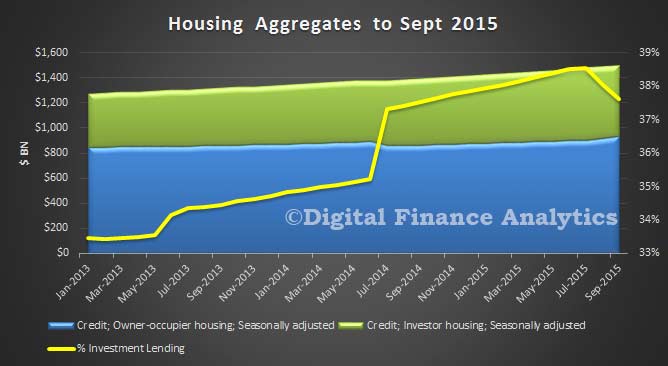

Looking in more detail at the housing data, owner occupied loans rose by 1.33% in the month to $932 bn, whilst investment loans fell by 0.38% to $563 bn. As a percentage of all loans, investment loans fell to 37.63%, from 38.55% in August.

Looking in more detail at the housing data, owner occupied loans rose by 1.33% in the month to $932 bn, whilst investment loans fell by 0.38% to $563 bn. As a percentage of all loans, investment loans fell to 37.63%, from 38.55% in August.

We see the results of the clamp down on investment loans coming through – finally – but they still make up a massive share of all loans (in the UK they are worried by an 18% share of investment loans!). We also see a massive drive to acquire and refinance owner occupied loans, as the banks now are backing this horse as the next growth lever. The share of investment loans is still higher than the rates reported by the banks before their reclassification, and it is worth remembering the regulators were worried about shares circa 35% when they imposed their speed limits. We are still higher than this.

We see the results of the clamp down on investment loans coming through – finally – but they still make up a massive share of all loans (in the UK they are worried by an 18% share of investment loans!). We also see a massive drive to acquire and refinance owner occupied loans, as the banks now are backing this horse as the next growth lever. The share of investment loans is still higher than the rates reported by the banks before their reclassification, and it is worth remembering the regulators were worried about shares circa 35% when they imposed their speed limits. We are still higher than this.

We will update APRA’s monthly banking stats (ADI’s).

One thought on “Housing Lending Still Higher At $1.5 Trillion”