The latest iteration of the BIS paper on proposed capital adequacy changes includes a fundamental change to the way the risk charge would be calculated for investment property purchases funded by a mortgage. Fundamentally, if repayments are “materially dependent on cash flows generated by the property”, then depending on the loan to value ratio, the risk weighting could be as high as 120%, significantly higher than today. We discussed this in our recent post.

BIS does not give any clear guidance on what “materially dependent” might mean, and comments are open until mid March, so finalisation will be later than this. However, this got us thinking. What would happen if, for some reason, the rental income stream stopped? Clearly in the short term, pending finding a new tenant or selling the property, the repayments would have to be made from other income streams – salary, investments and dividends.

So we have run some scenarios on our household database, to examine the potential impact. To start we estimate the average proportion of gross income which would need to go to servicing the investment mortgage. We have taken into account income from all sources (excluding rental income), and also calculated repayments based on the current interest rate, adjusted for discounts, and whether the mortgage was a principle and interest loan, or an interest only loan. We also take account of the impacts of negative gearing.

Over the next few days we will share some of our modelling, which will ultimately flow into our next Property Imperative report. Our last edition dates from September 2015 and is still available on request.

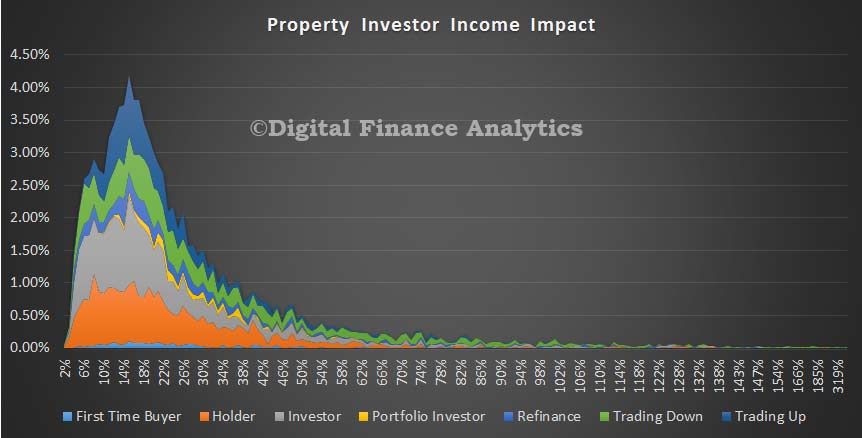

Our first analysis is grouped by our household property segments. These include households who only have investment property (Investors, and Portfolio Investors), as well as households with both an owner occupied property and an investment property (including first time buyers, holder, refinanced, trading-up and trading-down. You can read more about our segmentation here.

The chart shows the impact to their income if the repayments were to be serviced by said income, rather than rental streams. The chart shows the proportion of income which would be consumed, and the distribution of households by segment. There is considerable variation, but we see that a considerable proportion of households would need to put more than 25% of their income aside to service the mortgage. A small, but worrying proportion would require more than 50% of their income, and a small number more than 100%. This is significant, given the current low (and falling) income growth rates.

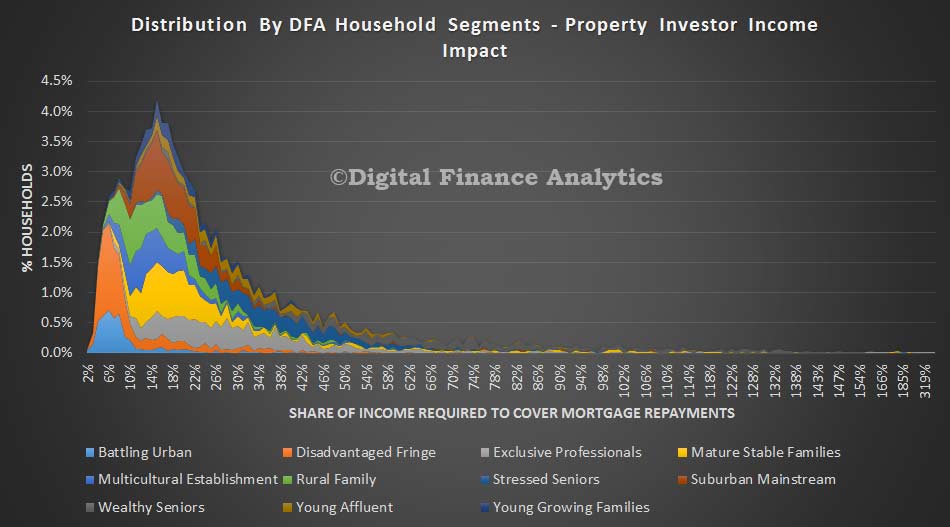

We can also look at the data through the lens of our master household segments. These are derived from a range of demographic and behaviourial elements. We see that generally more affluent households are more exposed to investment property, and as a result, require a larger proportion of their income (despite having larger incomes) to support the repayment required to replace rental income. We also see that stressed seniors, with a rental are more exposed, which is not surprising given their lower income levels.

We can also look at the data through the lens of our master household segments. These are derived from a range of demographic and behaviourial elements. We see that generally more affluent households are more exposed to investment property, and as a result, require a larger proportion of their income (despite having larger incomes) to support the repayment required to replace rental income. We also see that stressed seniors, with a rental are more exposed, which is not surprising given their lower income levels.

Standing back, this initial analysis shows that it is not easy to determine what is “material”. Different segments and property portfolios will require different settings. In addition, as the extra capital charges being discussed will translate into higher mortgage interest rates for some, it appears that these increases will hit different segments to varying extents.

Standing back, this initial analysis shows that it is not easy to determine what is “material”. Different segments and property portfolios will require different settings. In addition, as the extra capital charges being discussed will translate into higher mortgage interest rates for some, it appears that these increases will hit different segments to varying extents.

Will BIS attempt to describe conditions which are material, or leave it to the individual regulatory authorities – such as APRA?

Next time we will look at the consolidated impact of households with both owner occupied and investment loans. This is important because some households have more than half their income servicing property.

One thought on “How Material Is “Material” For Property Investors?”