The IMF published their latest assessment of Australia’s economy. It is relatively positive, though calls out risks in the housing sector and once again suggests tax changes would assist. They are also critical of attempts to segregate the property market into local and foreign buyers. There is a whole separate document on housing and risks in the system.

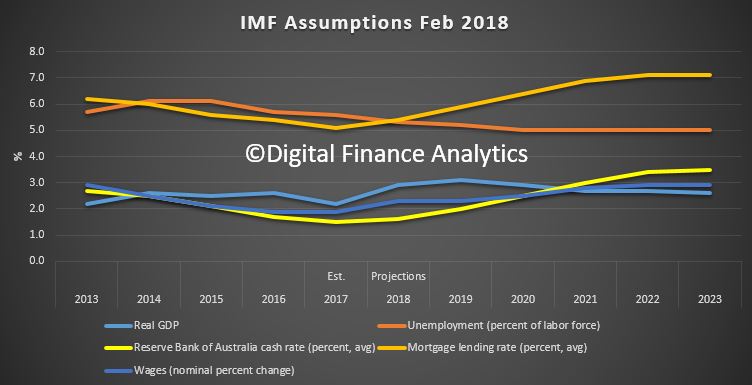

However, the underlying economic model assumptions are interesting. Most significant is the expected rise in average mortgage rates from 5.1% now, to 7.1% in 2021. That would cause some pain (and lift mortgage stress from ~920k to 1.25m households on our models).

They show unemployment drifting down to 5%, whilst there is a little improvement in GDP. The RBA cash rate rises to 3.25% in 2022/3. Overall wages growth drifts higher to 2.9% in 2023. House prices remain elevated, as does household debt, and debt to income rises, as interest rates climb.

They show unemployment drifting down to 5%, whilst there is a little improvement in GDP. The RBA cash rate rises to 3.25% in 2022/3. Overall wages growth drifts higher to 2.9% in 2023. House prices remain elevated, as does household debt, and debt to income rises, as interest rates climb.

On February 7, the Executive Board of the International Monetary Fund (IMF) concluded the 2017 Article IV consultation with Australia.

Australia has enjoyed a comparatively robust economic performance while adjusting to the end of the commodity price and mining investment booms of the 2000s. The recovery from these shocks has advanced further in 2017. Aggregate demand has been led by strong public investment growth amid a boost in infrastructure spending and private business investment has picked up, but private consumption growth has remained subdued. Employment growth has strengthened markedly over the year, although the economy is not yet back at full employment. Wage growth is weak and inflation is below its target range.

The macroeconomic policy stance has become more supportive with the infrastructure investment boost. The monetary policy stance is accommodative, with the current policy rate setting implying a real policy rate at zero relative to estimates of the real neutral long-term interest rate in the range of 1 to 2 percent. Infrastructure spending at the Commonwealth and State levels has increased by an average of 0.5 percent of GDP annually over the next 4 years relative to the last Article IV Consultation.

A housing boom has supported the Australian economy’s adjustment to the end of the boom, but has led to housing market imbalances and household vulnerabilities, which the authorities have addressed with a multipronged approach. The supply response to higher house prices has been strengthened, through increased spending on infrastructure, which helps increase the supply of accessible and developable land, and through zoning and planning reforms. The Australian Prudential Regulation Authority (APRA) used prudential policies to lower housing-related risks to household balance sheets and the banking system. Market entry for first-time home buyers has been facilitated through tax relief, grants, and support for accumulating deposits for down payments within the Superannuation framework.

Australian banks have further strengthened their resilience to negative housing and other shocks in 2017 and improved their funding profile. The capital adequacy ratio of the Australian banking system rose by another 0.8 percentage points through 2017, reaching 14.6 percent by end-September, with 10.6 percent in the form of Common Equity Tier 1 (CET-1) capital. The liquidity coverage ratio was comfortably above minimum requirements. By end-September 2017, many banks already had Net Stable Funding Ratios (NSFR) above the 100 percent required from January 1, 2018.

Recent structural policy efforts have focused on addressing infrastructure gaps, strengthening competition, and fostering research and development (R&D). Reforms to the competition law at the Commonwealth level, as proposed in the 2015 Competition Policy Review (the “Harper Review”), were enacted in November 2017, which should encourage more competitive behavior in the economy. The National Innovation and Science Agenda (NISA) seeks to strengthen R&D. In 2014, the government committed to reduce the gender gap in labor force participation by 25 percent by 2025 as part of the Brisbane Commitments in the G-20 process. The company tax rate for small companies with a turnover of up to A$50 million has been lowered from 30 to 27½ percent over the next 5 years.

Executive Board Assessment

Executive Directors commended Australia’s robust economic performance during the rebalancing of the economy in the wake of the mining investment boom of the 2000s. This has been helped by a resilient economy and strong policy frameworks. Directors noted that a more robust global outlook, employment growth, and infrastructure investment should help accelerate economic expansion. Nonetheless, while near‑term risks to growth have become more balanced, negative external risks could interact with domestic financial vulnerabilities and pose a threat to the recovery. Directors urged the authorities to maintain prudent policies, continue to address financial vulnerabilities, and raise long‑term productivity.

Directors agreed that continued macroeconomic policy support is needed to secure employment and inflation objectives. With inflation below target and the economy not yet back at full employment, the monetary policy stance should remain accommodative until stronger domestic demand growth and inflation are evident. Directors welcomed the more supportive fiscal policy stance due to infrastructure investment. They concurred that the Commonwealth budget repair strategy remains appropriately anchored by medium‑term budget balance targets. They noted that in the case of a more gradual recovery, Australia has the fiscal space to absorb this risk and protect spending for macrostructural reforms.

Directors considered appropriate the multipronged policy for addressing housing imbalances and vulnerabilities, including a tightening of prudential policies, a strengthening of housing supply, and targeted demand policies. They took note of the staff’s assessment that some policies are classified as capital flow management measures (CFMs) under the Fund’s Institutional View (IV), although their use has been consistent with the IV in most cases—in particular, that the CFMs have not substituted for warranted macroeconomic policies. In this context, many Directors raised the issue of intent and emphasized the need to consider the substance of the measures, and to assess their effectiveness in reducing financial stability risks. Some Directors, nonetheless, encouraged the authorities to consider measures that do not distinguish between residents and non‑residents where feasible (for example, on vacant properties). Directors noted that the housing policy package could be complemented by tax reform, including a gradual shift to more efficient property taxation through the introduction of a systematic land tax regime. Strong supply‑side policies will remain critical.

Directors highlighted that increased infrastructure investment should provide a welcome lift to productivity and longer‑term growth. Sustained structural policy efforts in promoting innovation and competition, upgrading labor force skills and reducing gender gaps, and advancing broad tax reform would complement these positive effects.