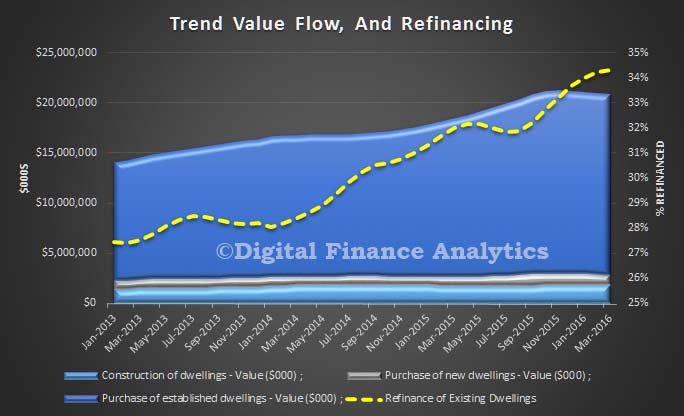

The latest housing finance data from the ABS for March 2016 showed that looking at trend data, investment lending was stronger, up 1.1% whilst owner occupied lending fell 0.7% month on month. However, we know there was more than $1.5 bn of adjustments in March, so the data should be handled with care. Significantly, the proportion of loans being refinanced continued to grow, up to 34.3% by value.

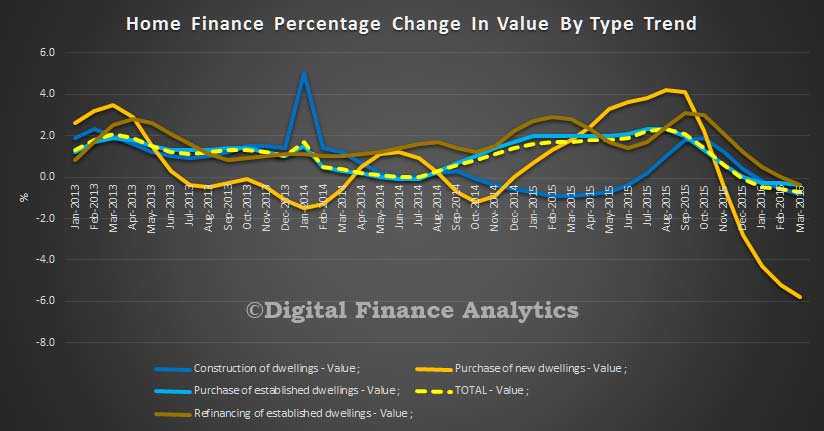

The percentage changes show significant falls in the purchase of new dwellings, down 5.8%, whilst refinance fell just 0.4% by value.

The percentage changes show significant falls in the purchase of new dwellings, down 5.8%, whilst refinance fell just 0.4% by value.

In trend terms, the number of commitments for owner occupied housing finance fell 0.2% in March 2016, whilst the number of commitments for the purchase of new dwellings fell 3.3%, the number of commitments for the construction of dwellings fell 0.9% and the number of commitments for the purchase of established dwellings rose 0.1%.

In trend terms, the number of commitments for owner occupied housing finance fell 0.2% in March 2016, whilst the number of commitments for the purchase of new dwellings fell 3.3%, the number of commitments for the construction of dwellings fell 0.9% and the number of commitments for the purchase of established dwellings rose 0.1%.

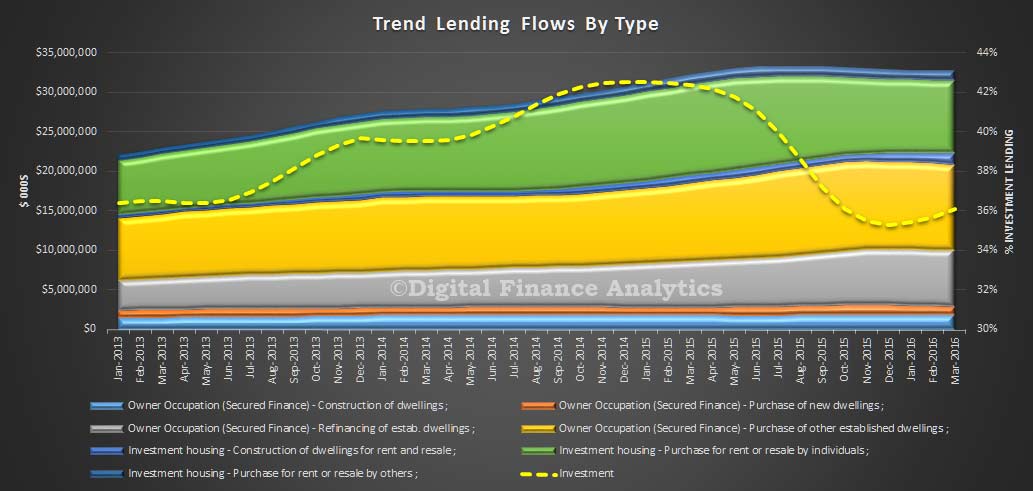

Looking at the mix of loans, the proportion of new loans for investment purposes rose from 35.7% to 36.1% in March.

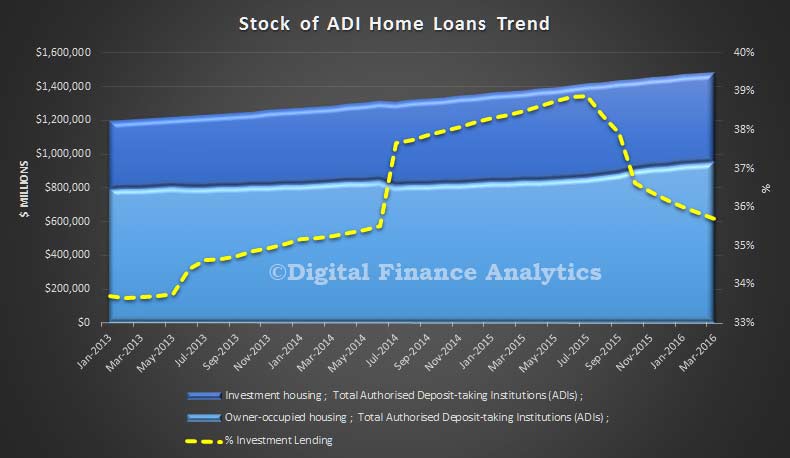

In stock terms, the proportion of investment loans fell slightly, from 35.8% to 35.7%. Owner occupied loan stock rose 0.71% to $953 billion, whilst investment loans grew 0.11% to $529 billion. Overall loan stock rose by 0.49% to $1,482 billion.

In stock terms, the proportion of investment loans fell slightly, from 35.8% to 35.7%. Owner occupied loan stock rose 0.71% to $953 billion, whilst investment loans grew 0.11% to $529 billion. Overall loan stock rose by 0.49% to $1,482 billion.

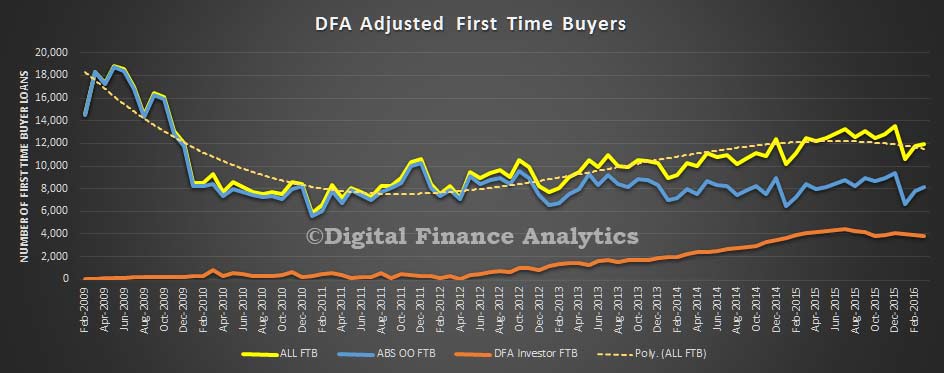

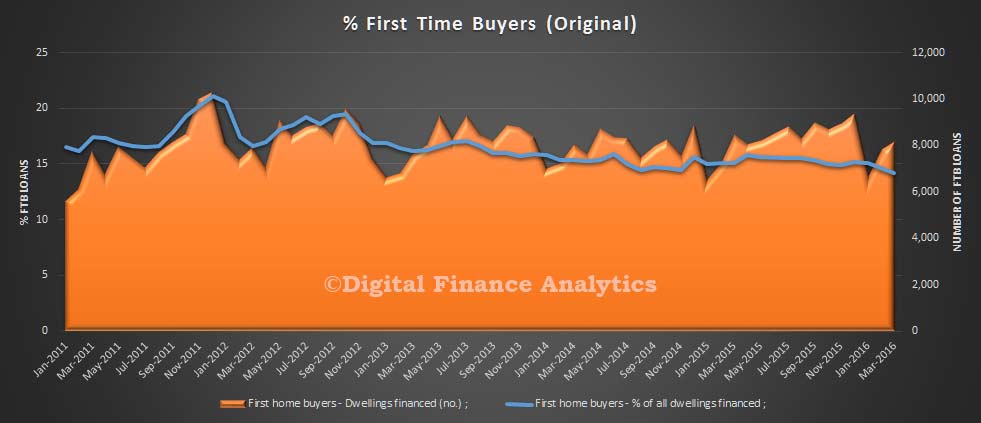

In original terms, the number of first home buyer commitments as a percentage of total owner occupied housing finance commitments fell to 14.2% in March 2016 from 14.6% in February 2016.

In original terms, the number of first home buyer commitments as a percentage of total owner occupied housing finance commitments fell to 14.2% in March 2016 from 14.6% in February 2016.

However, the number of loans rose by 4.1%, and the average loan loan size was $329k. We are still seeing a number of first time buyers going direct to the investor sector, through our household surveys, but the volumes were down by 2.8% in the month. Overall, there were 11,972 first time buyer transactions, up 1.8%; in original terms.

However, the number of loans rose by 4.1%, and the average loan loan size was $329k. We are still seeing a number of first time buyers going direct to the investor sector, through our household surveys, but the volumes were down by 2.8% in the month. Overall, there were 11,972 first time buyer transactions, up 1.8%; in original terms.