The latest lending finance data from the ABS, released today, shows the total value of dwelling finance commitments excluding alterations and additions rose 0.3%. Investment housing commitments rose 1.1%, while owner occupied housing commitments fell 0.1%. The less reliable seasonally adjusted measure showed the total falling by 1.8%. Many commentators will I am sure focus on this, and claim there is a “dramatic correction”.

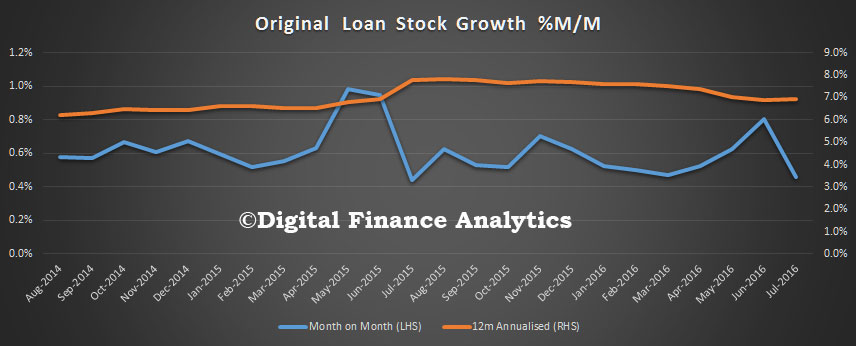

The original loan stock series shows an annual growth rate of housing lending still running close to 7%; with a slight slow down in recent months – not the significant slow down some have suggested.

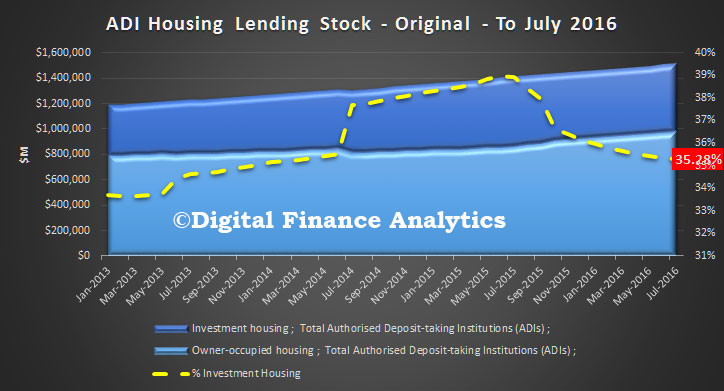

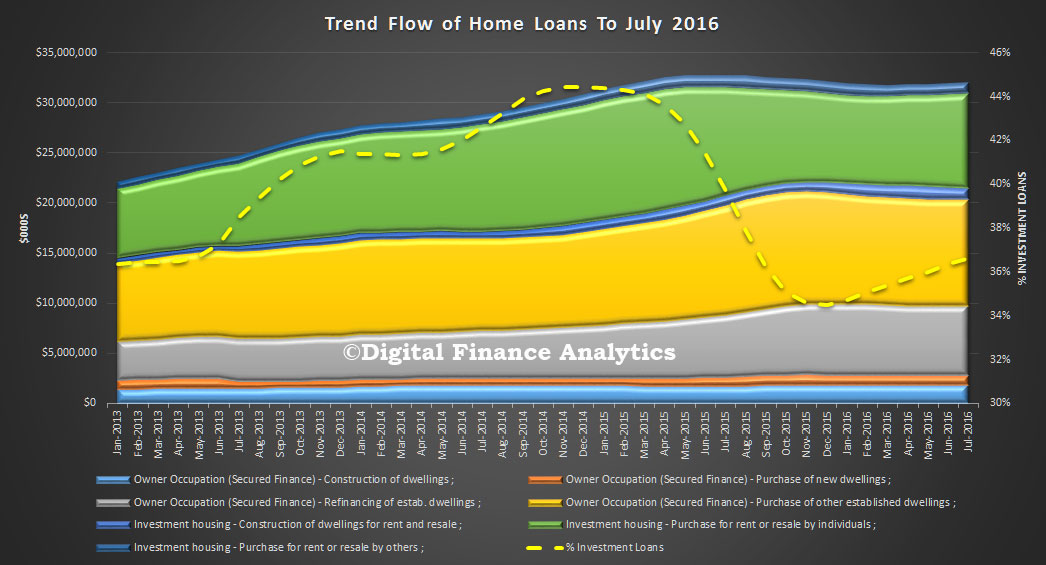

Total loans on book, in original terms, is $1.52 trillion, up 0.46%, of which 35.28% are for investment loan purposes, down from 35.36% last month. Investment lending stock rose $1.3 billion (up 0.24%) and OO lending stock rose 0.93%, up $9 billion. Remember, more than $1bn loans were reclassified in the month, so there is noise in the data.

Total loans on book, in original terms, is $1.52 trillion, up 0.46%, of which 35.28% are for investment loan purposes, down from 35.36% last month. Investment lending stock rose $1.3 billion (up 0.24%) and OO lending stock rose 0.93%, up $9 billion. Remember, more than $1bn loans were reclassified in the month, so there is noise in the data.

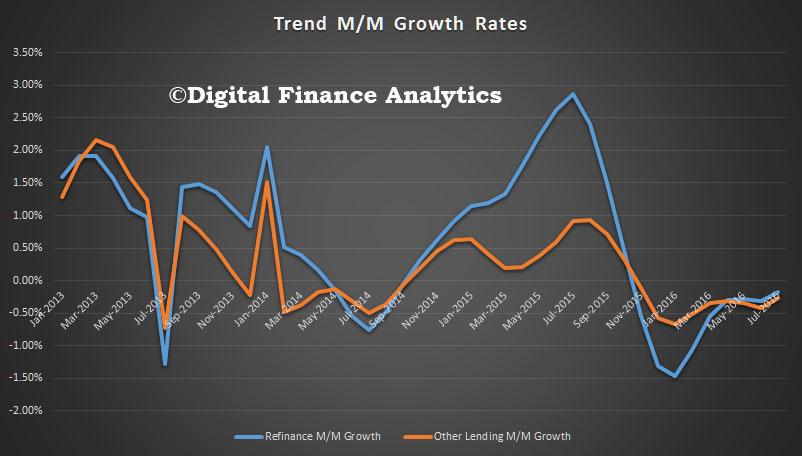

Looking at the monthly trend flows, momentum continues to ease, but more slowly.

Looking at the monthly trend flows, momentum continues to ease, but more slowly.

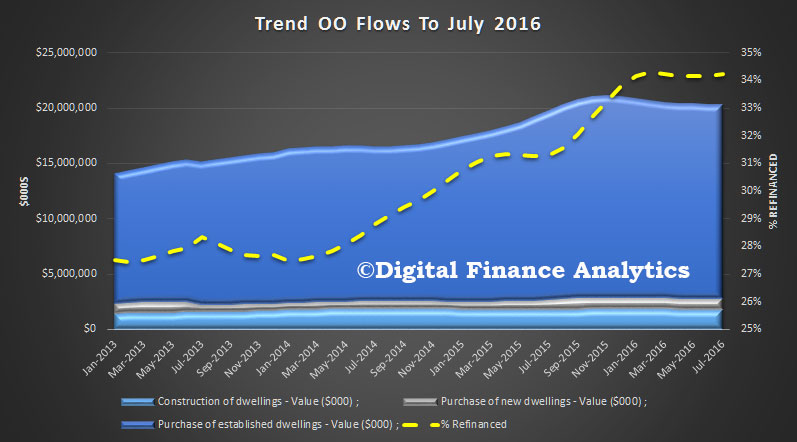

Last month, construction loans fell 0.34% in number terms, down 19,000; and fell by $0.7m in value terms. There was a rise in the number of new dwellings purchased, up 0.45% or 12,000; and in value terms up 0.66% or $6.5m. The purchase of established dwellings fell by $26m, or 0.15%. The number of refinanced transactions continued to rise, up 42,000, or 0.2%, and up 0.06% or $4.3m. The proportion of refinanced transactions fell by 0.18% compared with last month, or $24m. Refinancing remains a critical driver of ongoing growth.

Last month, construction loans fell 0.34% in number terms, down 19,000; and fell by $0.7m in value terms. There was a rise in the number of new dwellings purchased, up 0.45% or 12,000; and in value terms up 0.66% or $6.5m. The purchase of established dwellings fell by $26m, or 0.15%. The number of refinanced transactions continued to rise, up 42,000, or 0.2%, and up 0.06% or $4.3m. The proportion of refinanced transactions fell by 0.18% compared with last month, or $24m. Refinancing remains a critical driver of ongoing growth.

In trend terms, the value of investment loans rose by $127m or 1.1%, and made up 36.6% of new transactions, up compared with 36.3% last month.

In trend terms, the value of investment loans rose by $127m or 1.1%, and made up 36.6% of new transactions, up compared with 36.3% last month.

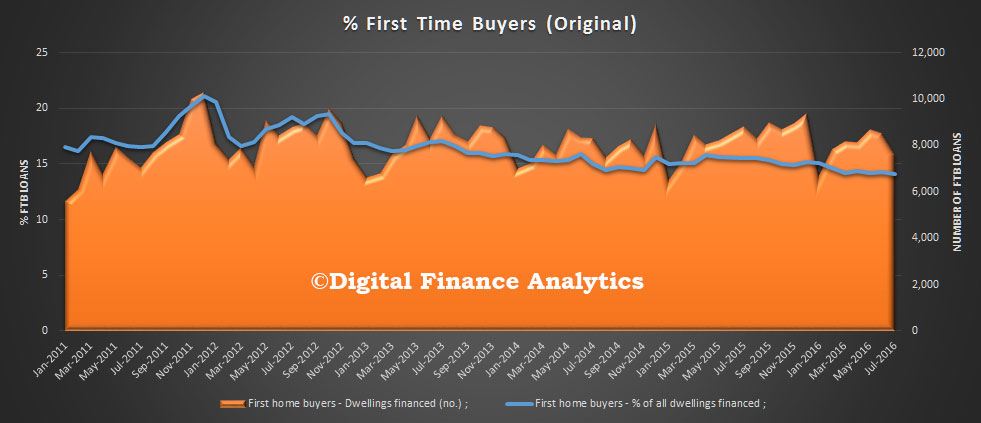

Finally, in original terms, the number of first home buyer commitments as a percentage of total owner occupied housing finance commitments fell to 14.1% in July 2016 from 14.3% in June 2016. The number fell from 8,486 to 7,586, down more than 10%. The average loan size was $335,600, 0.2% higher than last month. Signs of tightening in lending conditions?

Finally, in original terms, the number of first home buyer commitments as a percentage of total owner occupied housing finance commitments fell to 14.1% in July 2016 from 14.3% in June 2016. The number fell from 8,486 to 7,586, down more than 10%. The average loan size was $335,600, 0.2% higher than last month. Signs of tightening in lending conditions?

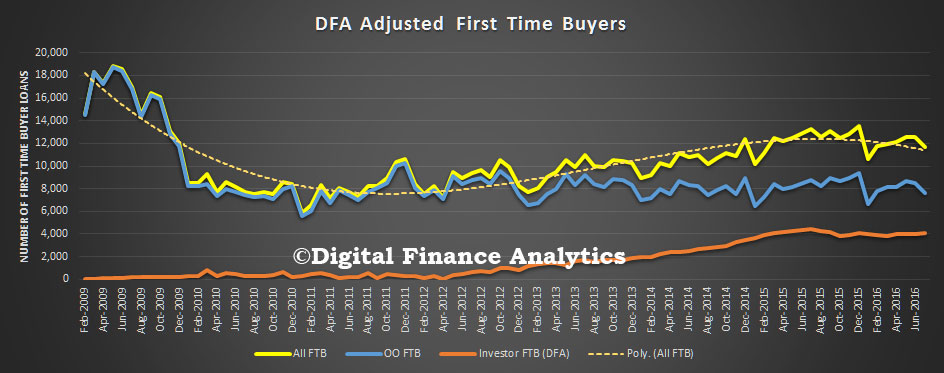

A proportion of first time buyers continue to go direct to the investment sector, as shown in the chart below which overlays our survey data on the ABS data-set.

A proportion of first time buyers continue to go direct to the investment sector, as shown in the chart below which overlays our survey data on the ABS data-set.