Investors have played an increasingly important role in the Australian housing market in recent years. Our new research shows the actual return rate for housing investors almost doubled a layman’s expectation. Experienced investors are taking advantage of the knowledge gap and might continue to price out other housing buyers.

The sharp increase in investor credit in recent years could be partly attributed to the strong growth of housing prices, particularly in Sydney and Melbourne. However, the reported capital gains might not have fully reflected investors’ actual returns as the impact of debt financing in property investment has been neglected.

Since housing investors typically use large amounts of debt to fund their investment, using the return on equity (after adjusting for debt financing) more accurately reflects their actual return.

In recent years, regulators such as the Australian Prudential Regulation Authority and lenders have implemented measures to moderate the growth of investor lending. Despite these efforts, investors have come back into the housing market since the second half of 2016.

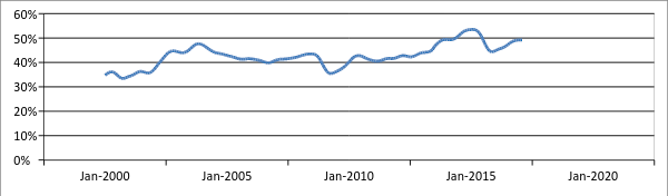

Proportion of housing investment loans

ABS, Housing Finance, Australia: February 2017

Higher returns come with greater risk

Our research sampled properties in 14 suburbs across Sydney, using the Property Investors Alliance database. The results provide some empirical evidence to demonstrate the housing return on equity with debt financing is significantly higher, at an annual return of nearly 14% per year, than the housing return on property without debt financing of about 7% per year.

This could explain the increasing proportion of investment loans in the housing market. The knowledge of investors’ advantage should also be used to inform the ongoing debate about regulating investment housing loans to enhance housing affordability for first home buyers in particular.

It is important to highlight the effect of debt financing on decisions to invest in housing. The results clearly show the enhanced returns are likely to have an acute impact.

At the same time, a higher risk level as a result of the use of debt financing has also been documented. This highlights that housing investors should closely manage their exposure to financial risk from using debt financing by using a prudential risk-management tool.

Returns and risk on housing portfolios: 2009-2015

Author provided

Explaining the increased rate of return

We used an assumption of 20% equity to demonstrate the impact of debt financing, which is in line with the current deposit requirement from major banks. Here’s an example to demonstrate the effect of debt financing.

Say an investor buys a house for A$1 million. The investor provides a 20% deposit ($200,000); therefore $800,000 was borrowed. The investor took an “interest-only” loan with an interest rate of 5% per year – so the interest cost is $40,000 per year. The investor also receives a net rental income of $30,000 in Year 1.

A year later, the investor decides to sell the property for $1.1 million (its value having increased by 10% over the year). The traditional performance analysis of property (without debt financing) would show the return on this housing investment is 13%: ($1,100,000-1,000,000+$30,000)/$1,000,000 = 13%.

Given the housing investor used debt financing, 13% is not the actual return for the investor. The investor’s actual return on equity for the investor is 45%: ($300,000-$200,000)+($30,000-$40,000)/$200,000 = 45%.

Property returns vs equity returns

Author provided

Experienced investors exploit their advantage

Overall, the results suggest the actual return rate for housing investors is significantly higher than the layman might expect from the major housing index providers.

The documented returns may not be applicable, however, to owner occupiers who are also using debt financing, via mortgages, to buy their property. There are two main reasons for this:

- owner occupiers mainly use their houses for their own residency purposes, so no rental income will be generated to offset the mortgage repayment; and

- housing investors are able to sell their properties whenever they want to realise gains in value, while owner occupiers do not have that flexibility.

Importantly, experienced housing investors, in the current low interest rate environment, have realised the benefits of debt financing and taken advantage of the knowledge gap to exploit the higher returns available to them.

These findings also highlight the need for an innovative product to assist home buyers to enter the housing market.

Author: Chyi Lin Lee , Associate Professor of Property, Western Sydney University

One thought on “Investors are exploiting returns on debt financing to muscle out home buyers”