DFA analysis of Australian mortgages highlight that we have high LTI ratios, and high LVR ratios, both indicating a build up of systemic risks in the system. We used postcode level analysis, and believe that it is essential to “get granular”.

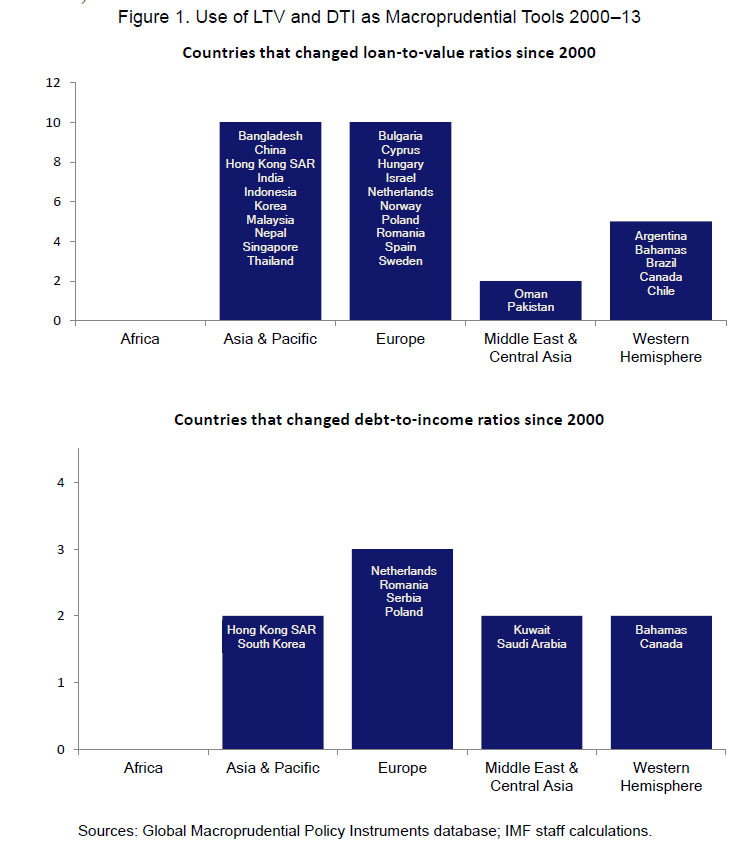

Now the IMF has released a working paper on the effectiveness of using loan-to-value (LTV) and debt-service-to-income (DTI) limits as many countries face a new round of rising house prices. Yet, very little is known on how these regulatory instruments work in practice. This paper contributes to fill this gap by looking closely at their use and effectiveness in six economies—Brazil, Hong Kong SAR, Korea, Malaysia, Poland, and Romania.

In most cases,the caps on LTV and DTI started in the range of 60–85 percent and 30–45 percent, respectively, for mortgage loans. In all countries, there were changes to the limits of LTV/DTIs typically because the authorities noted that they were not having the desired effect. In some cases, house price and mortgage growth did not fall, and in other cases, the limits did not bind. Concerned with speculative activities, authorities in some countries lowered the caps selectively either for speculative prone (geographical) areas or for individuals with multiple mortgages. In one case, the centrally set caps were removed and banks were allowed to set their own limits, validated by supervisors. However, this did not work, and stricter requirements were put back in place.

In most cases,the caps on LTV and DTI started in the range of 60–85 percent and 30–45 percent, respectively, for mortgage loans. In all countries, there were changes to the limits of LTV/DTIs typically because the authorities noted that they were not having the desired effect. In some cases, house price and mortgage growth did not fall, and in other cases, the limits did not bind. Concerned with speculative activities, authorities in some countries lowered the caps selectively either for speculative prone (geographical) areas or for individuals with multiple mortgages. In one case, the centrally set caps were removed and banks were allowed to set their own limits, validated by supervisors. However, this did not work, and stricter requirements were put back in place.

To curb leakages, the limits were extended in some of the countries to insurance companies, mutual funds and finance companies that advertised mortgage products. It was also extended to development financial institutions.

Insights include: rapid growth in high-LTV loans with long maturities or in the number of borrowers with multiple mortgages can be signs of build up in systemic risk; monitoring nonperforming loans by loan characteristics can help in calibrating changes in the LTV and DTI limits; as leakages are almost inevitable, countries strive to address them at an early stage; and, in most cases, LTVs and DTIs were effective in reducing loan-growth and improving debt-servicing performances of borrowers, but not always in curbing house price growth.

Note: The views expressed in this Working Paper are those of the author(s) and do not necessarily represent those of the IMF or IMF policy. Working Papers describe research in progress by the author(s) and are published to elicit comments and to further debate.