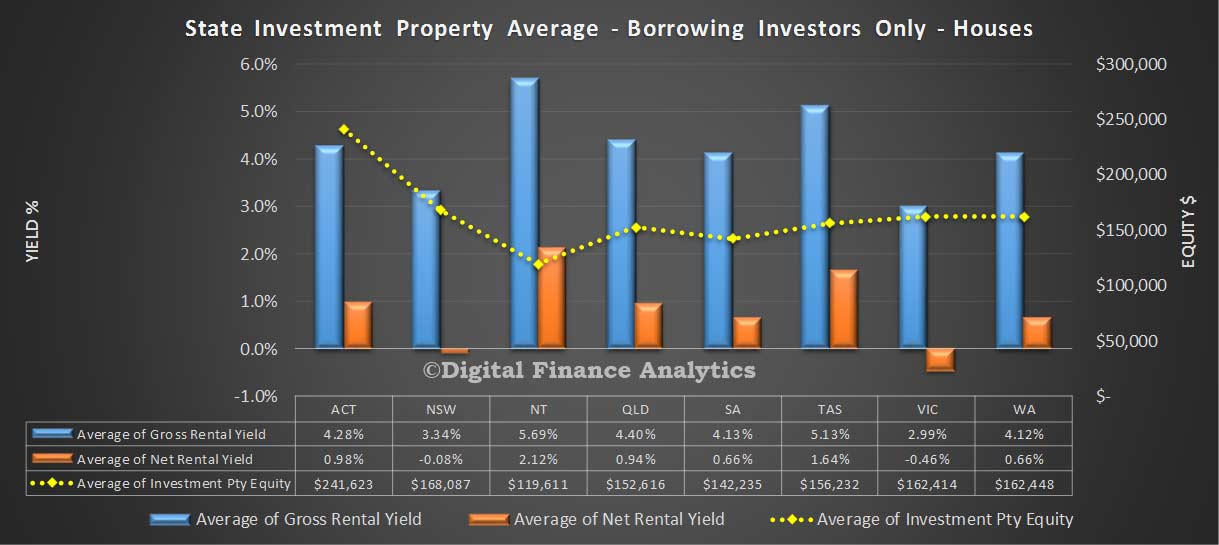

We have had the opportunity to do a deep dive on investment property loans, using data from our household surveys. We have looked at gross rental returns, net rental returns (after the costs of mortgage servicing are included) and net equity held (current property value minus mortgage outstanding). The results are in, and they make fascinating reading, especially in the context of up to 40% of all residential property loans being for investment purposes, according to the RBA. Whilst we will not be sharing the full results here, one chart tells the story quite well.

We show the average gross rental yield on houses by state, (the blue bar), net rental yields before tax (the orange bar) and the net gross average capital gain (the yellow line). Gross yield is annualised rental over current value, assuming full occupancy; net rental is annual rental less annual mortgage repayments; and capital value is the current marked to market price less current outstanding mortgage. The first two are shown as a percentage, the last as a dollar value. The chart below only covers houses, we have separate data on other property types but won’t show that here.

We found that investment property which were houses in VIC were on average losing money at the net rental level (and this is before any maintenance or other costs on the property). Those in NSW were a little better, but still in negative territory. The other states were in positive ground – some only just – and of course this is at current interest rates, before the latest uplifts were applied by the banks. We accept that the pre-tax position does not tell the full story, but as a stand-alone investment, many property investors are from a cash flow perspective underwater. Indeed, they are banking on prospective capital gains, and at the moment, they do have a cushion, but if prices were to slip, many would find this eroded quickly.

We found that investment property which were houses in VIC were on average losing money at the net rental level (and this is before any maintenance or other costs on the property). Those in NSW were a little better, but still in negative territory. The other states were in positive ground – some only just – and of course this is at current interest rates, before the latest uplifts were applied by the banks. We accept that the pre-tax position does not tell the full story, but as a stand-alone investment, many property investors are from a cash flow perspective underwater. Indeed, they are banking on prospective capital gains, and at the moment, they do have a cushion, but if prices were to slip, many would find this eroded quickly.

Our take is that the property investment sector contains considerable risks for banks, and investors, and these are not well understood at the moment. The more detailed analysis we did also showed that some specific customer segments, regions and postcodes were more at risk. Running scenarios on small interest rate rises shows that things get worse very quickly, especially for higher LVR loans.

We concur with analysis from Ireland and New Zealand, that the risks in the investment loan portfolios, despite the apparent historic low rates of default, are higher, and under Basel IV we expect investment loans to carry a higher capital rating, meaning that interest rates on investment loans are likely to rise more in the future, relative the the cash rate.

2 thoughts on “Many Eastern States Investment Properties Are Underwater”