More households are only able to purchase residential property with help from parents – the Bank of Mum and Dad. This has become a critical factor in helping first time buyers in particular break into the very expensive property market, especially as lenders tighten their underwriting standards.

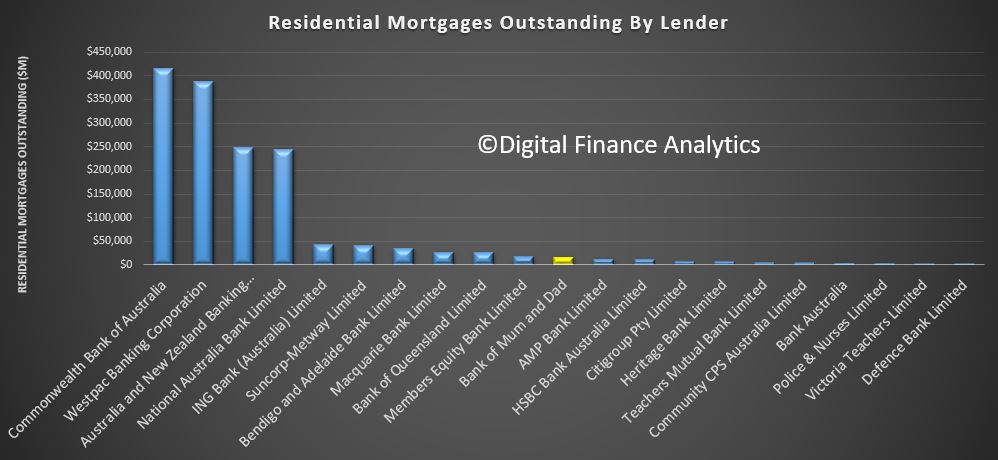

But here is an astonishing fact – the Bank of Mum and Dad, on our latest estimate, is the eleventh largest lender in Australia, ahead of AMP Bank, HSBC and most of the community banks and mutuals. We estimate at least $16 billion is outstanding with the Bank of Mum and Dad, and it is growing fast.

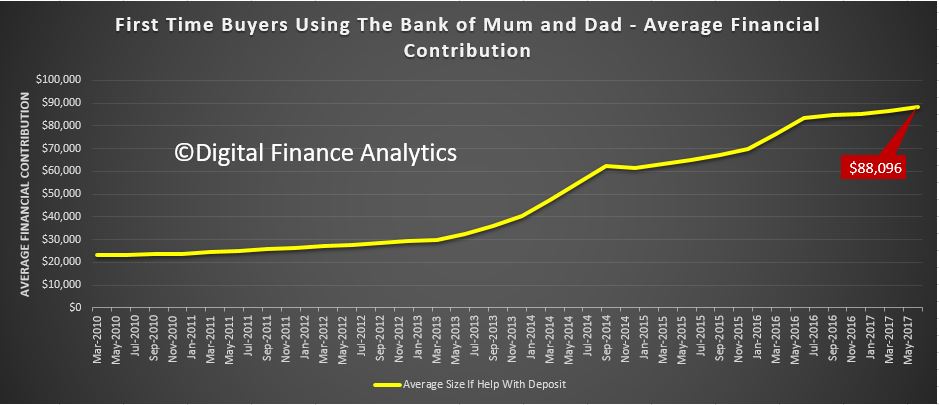

The average advance to a prospective purchaser is now $88,096, and this continues to rise.

The average advance to a prospective purchaser is now $88,096, and this continues to rise.

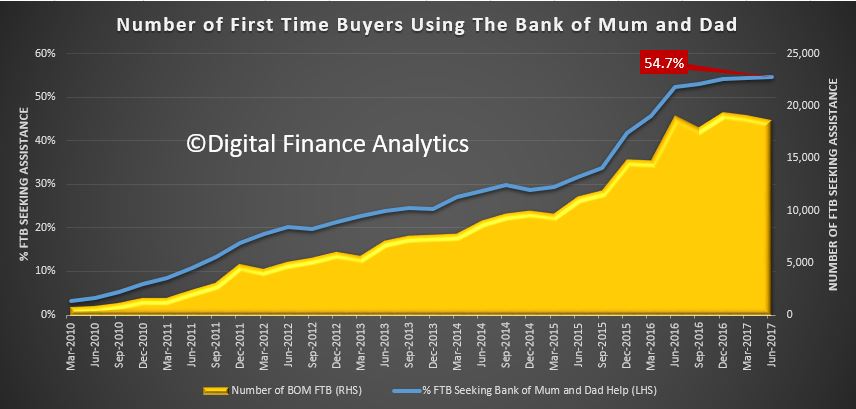

More than half of first time buyers need help from the Bank of Mum and Dad, either a cash gift or loan, or other help such as paying stamp duty, helping with mortgage repayments or child care costs. This is because of the equity held by those owning property, which is accessible when needed. But it does reinforce the inter-generational issues, and the risks in the market.

More than half of first time buyers need help from the Bank of Mum and Dad, either a cash gift or loan, or other help such as paying stamp duty, helping with mortgage repayments or child care costs. This is because of the equity held by those owning property, which is accessible when needed. But it does reinforce the inter-generational issues, and the risks in the market.

We wonder how many lenders check specifically to see if the saved deposit a prospective first time buyer has is a gift or private loan.

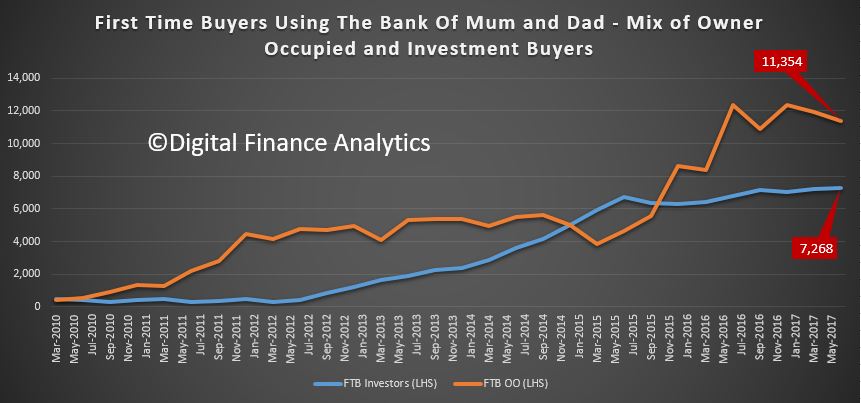

The mix of loans is interesting in that we see a relative rise in the number of owner occupied transactions where the Bank of Mum and Dad is active. In 2015, more investor loans were funded than owner occupied loans, that has reversed now.

The mix of loans is interesting in that we see a relative rise in the number of owner occupied transactions where the Bank of Mum and Dad is active. In 2015, more investor loans were funded than owner occupied loans, that has reversed now.

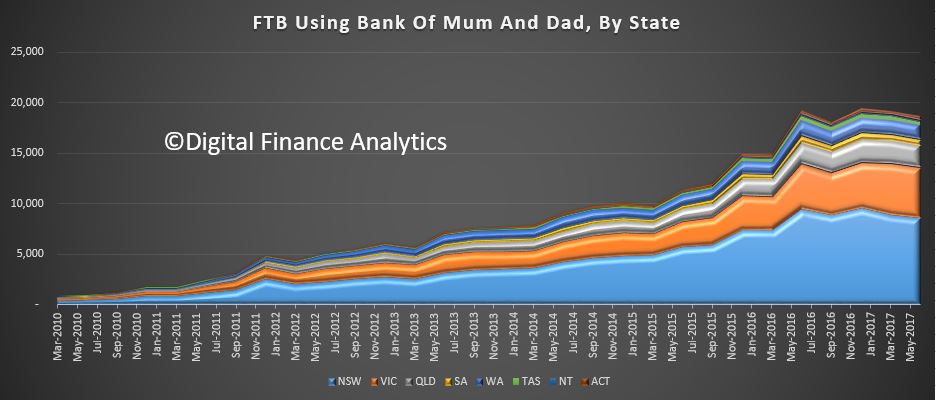

Across the states, the relative proportion in VIC is growing, although NSW still has the largest number of loans. But the Bank of Mum and Dad is active is all states and territories.

Across the states, the relative proportion in VIC is growing, although NSW still has the largest number of loans. But the Bank of Mum and Dad is active is all states and territories.

Three points worth considering.

Three points worth considering.

First, new buyers are ever more reliant on assistance from parents, but this creates inter-generation pressure with older home owners perhaps giving away value which should be part of their retirement nest egg, and younger buyers holding additional debt obligations below the water line. All caused by our silly property market, as Four Corners discussed. Those who do not have “wealthy” parents have little chance of entering the market, another factor in the inequality debate.

Second, this is of course totally (rightly) unregulated, but suggests that overall housing debt is even higher than might be thought from the official statistics. Often the arrangements are not formalised, and this can lead to issues down the track. Bank underwriting standards need to take account of this phenomenon.

Third our analysis suggests that households who receive such assistance are more likely to get into financial difficulty later, because they have not had the discipline of saving and so over-reach property wise.

Just one more element to consider when trying to understand the complex property finance sector.

6 thoughts on “Meet The Eleventh Largest and Totally Unregulated Bank In Australia”