The monthly banking stats from APRA for May 2017 were released today. The banks lifted their mortgage books by $9.2 billion to $1.56 trillion, up 0.6% in the month, still well ahead of income growth, thus household debt is still rising. The APRA controls are not strong enough.

Within this, owner occupied loans grew 0.7% to $1,010 billion and investment loans grew 0.42% to $549.9 billion (higher than the 0.39% last month). The proportion of loans for investment purposes stands at 35.4% on a portfolio basis.

Growth is accelerating, supported by stronger owner occupied lending – as expected seeing the change of emphasis we have seen from the banks.

Growth is accelerating, supported by stronger owner occupied lending – as expected seeing the change of emphasis we have seen from the banks.

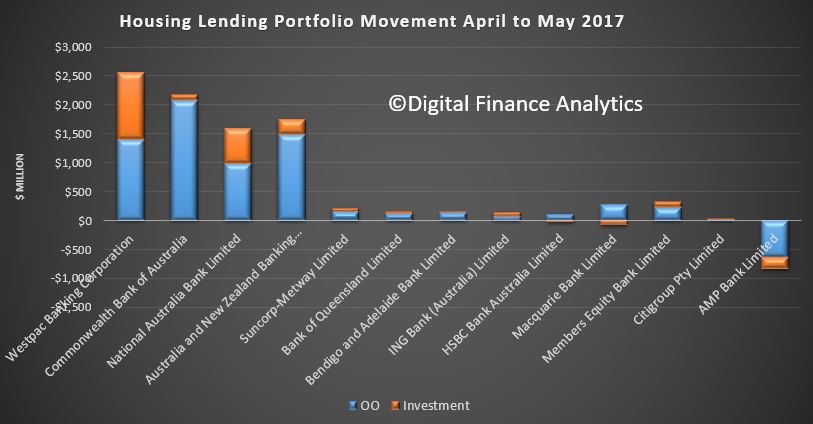

Looking at the individual lenders, Westpac wrote the most investment loans (which may explain their recent moved to tighten criteria and reduce loan types).

Looking at the individual lenders, Westpac wrote the most investment loans (which may explain their recent moved to tighten criteria and reduce loan types).

There were small changes in market share, with CBA leading the way on owner occupied lending, and Westpac on investment loans, suggesting different risk profiles.

There were small changes in market share, with CBA leading the way on owner occupied lending, and Westpac on investment loans, suggesting different risk profiles.

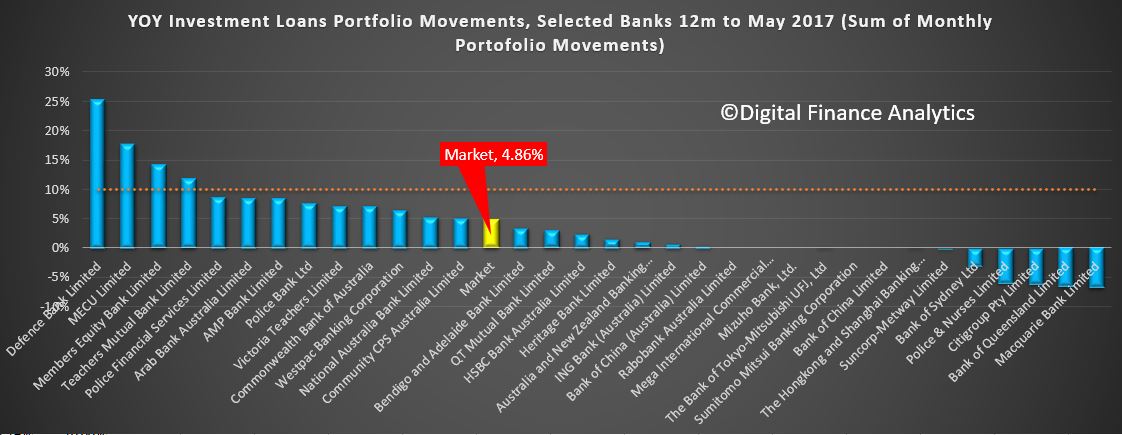

Finally, looking at the APRA speed limit, of 10%, the 12 month market growth for investment lending is sitting at 4.8% (sum of the monthly movements, as we still see a number of lenders above the limit, but not the majors.

Finally, looking at the APRA speed limit, of 10%, the 12 month market growth for investment lending is sitting at 4.8% (sum of the monthly movements, as we still see a number of lenders above the limit, but not the majors.

A caveat, of course APRA uses its internal measures to assess growth, which may not be the same as the public disclosures.

A caveat, of course APRA uses its internal measures to assess growth, which may not be the same as the public disclosures.

So, we think further steps need to be taken to cool the mortgage market – too much debt is being loaded on to households in a rising interest rate, low/no income growth environment. This also suggests home prices will continue to rise, after recent slowing trends were reported.

The RBA will release their credit aggregates shortly, and this will give a whole of market view. But debt growth just cannot continue at these levels.

2 thoughts on “Mortgage Lending Remains Too Strong”