Continuing our examination of the latest household survey results, today we look at the refinance segment. This sector of the market is poorly understood, not least because refinance of investment loans are not separately reported in the official statistics. However, yesterday we got some insights from the new RBA Governor’s handout pack.

It shows that currently more than 30% of all home loan approvals are for refinancing (and this data includes estimates of investor refinancing). This is an all time high.

Actually, the average term for a home loan is dropping, to below 4 years, and a quarter of the book is churning each year. Here is the reason.

New loans are being deeply discounted, (compared with rates being paid by loan holders). The RBA says:

The spread between the benchmark SVRs and the lowest available advertised rates has increased in recent years. The difference reflects both advertised and unadvertised discounts. It is not unusual for the discounts to be up to 1½ percentage points. Changes in discounts only affect new borrowers (and not the existing stock of mortgages).

This discounting is supported by lower funding costs.

As a result, bank net interest margins are largely unchanged.

The gap is being closed by lower deposit interest rates (other than for long-dated term deposits which the RBA says accounts for about 2% of bank funding only).

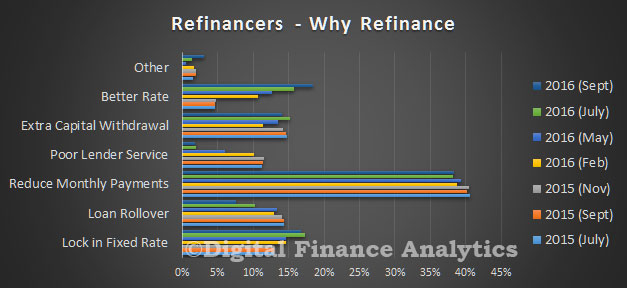

So against this backcloth, the 1.3 million households in the refinance segment are seeking to refinance, driven by the desire to reduce monthly payments (38%), better rates (18%) or to lock in an attractive fixed rate (17%). Poor service only accounts for a small proportion of the transactions.

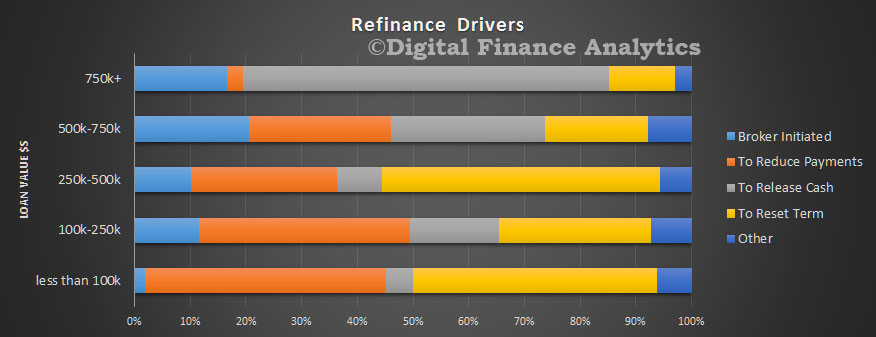

If we analyse the drivers by loan size, we see that brokers are tending to be more proactive when the loan is larger, and here refinance is more about releasing cash than just a lower rate. Indeed, much of this cash release is going back into the investment property sector, as we discussed yesterday.

If we analyse the drivers by loan size, we see that brokers are tending to be more proactive when the loan is larger, and here refinance is more about releasing cash than just a lower rate. Indeed, much of this cash release is going back into the investment property sector, as we discussed yesterday.

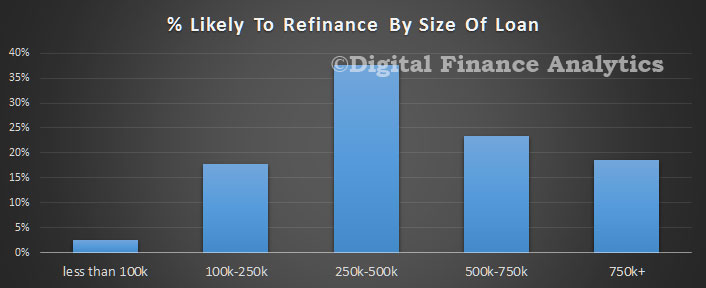

Overall, households with loans in the $250-500k band are most likely to refinance.

Overall, households with loans in the $250-500k band are most likely to refinance.

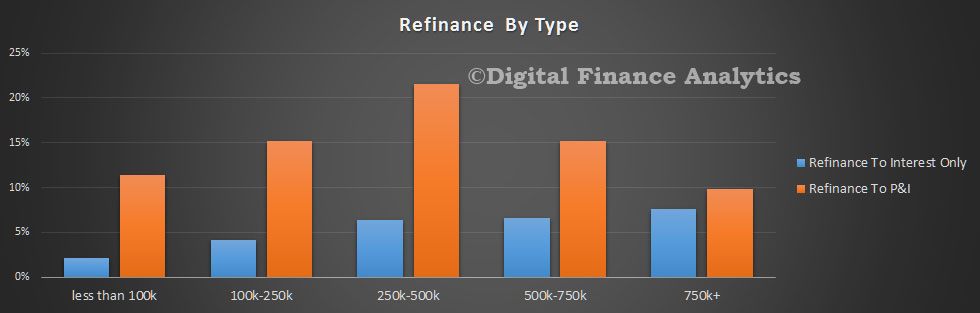

Larger loans are more likely to be refinanced to an interest only loan.

Larger loans are more likely to be refinanced to an interest only loan.

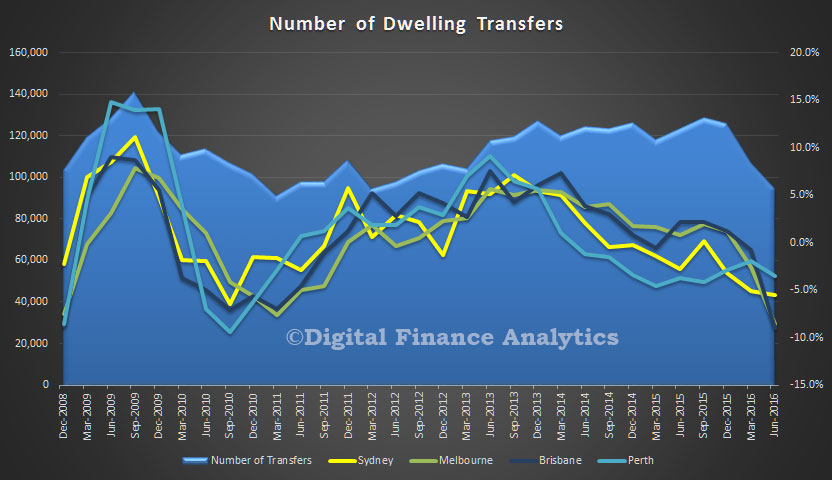

So refinancing activity is supporting market momentum. Though total dwelling transfers are down, as shown by the ABS data, released this week, remember that a refinanced transaction would not necessarily be counted.

So refinancing activity is supporting market momentum. Though total dwelling transfers are down, as shown by the ABS data, released this week, remember that a refinanced transaction would not necessarily be counted.

This chart, using ABS data, shows the total transfers of all dwellings (houses and other) and we see a fall in total transfers from Sept 2015, a peak of more than 120,000 to below 100,000 per quarter. Mapping the main centres, and smoothing the data a little, we see that Brisbane fell 10%, Melbourne 9% and Sydney 6%. So beware using this data to argue that housing momentum is easing, it is not that simple. The latest data may also be revised later by the ABS.

So, refinancing is an important element in understanding the current dynamic, and there are more households in the market now for a refinanced deal than a year ago. This explains the adverts “has your home loan got a 3 in front of it?” as shown below….

So, refinancing is an important element in understanding the current dynamic, and there are more households in the market now for a refinanced deal than a year ago. This explains the adverts “has your home loan got a 3 in front of it?” as shown below….

One thought on “Mortgage Refinance Momentum Remains Strong”