Digital Finance Analytics has released mortgage stress and default modelling for Australian mortgage borrowers, to end August 2017. Across the nation, more than 860,000 households are estimated to be now in mortgage stress (last month 820,000) with more than 20,000 of these in severe stress. This equates to 26.4% of households, up from 25.8% last month.

We also estimate that nearly 46,000 households risk default in the next 12 months, 7,000 down from last month, as we have revised down our expectations of future mortgage rate rises.

We also estimate that nearly 46,000 households risk default in the next 12 months, 7,000 down from last month, as we have revised down our expectations of future mortgage rate rises.

In this video we discuss the results and countdown the top ten suburbs across Australia.

The main drivers of stress are rising mortgage rates and living costs whilst real incomes continue to fall and underemployment is on the rise. This is a deadly combination and is touching households across the country, not just in the mortgage belts. In August higher power prices, council rates and childcare costs hit home.

This analysis uses our core market model which combines information from our 52,000 household surveys, public data from the RBA, ABS and APRA; and private data from lenders and aggregators. The data is current to end August 2017.

We analyse household cash flow based on real incomes, outgoings and mortgage repayments. Households are “stressed” when income does not cover ongoing costs, rather than identifying a set proportion of income, (such as 30%) going on the mortgage.

Those households in mild stress have little leeway in their cash flows, whereas those in severe stress are unable to meet repayments from current income. In both cases, households manage this deficit by cutting back on spending, putting more on credit cards and seeking to refinance, restructure or sell their home. Those in severe stress are more likely to be seeking hardship assistance and are often forced to sell.

Martin North, Principal of Digital Finance Analytics said “flat incomes and underemployment mean rising costs are not being managed by many, and household budgets are really under pressure. Those with larger mortgages are more impacted by rate rises if and when they occur”.

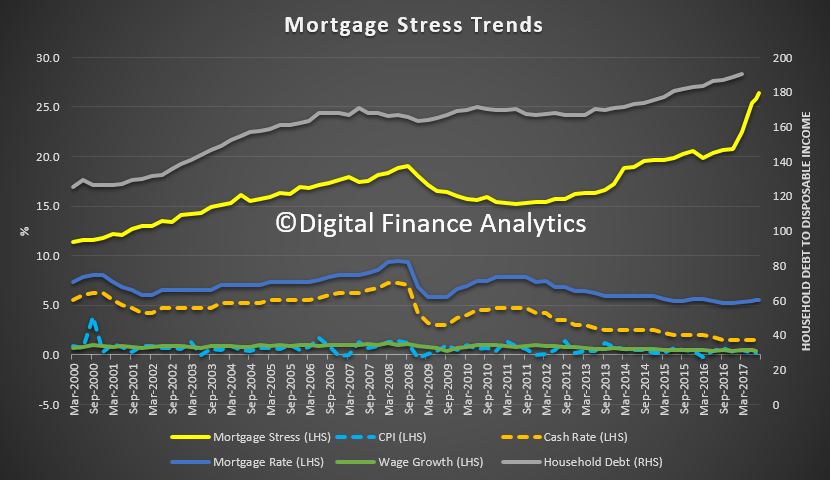

“The latest housing debt to income ratio is at a record 190.4[1] so households will remain under pressure. Stressed households are less likely to spend at the shops, which acts as a drag anchor on future growth. The number of households impacted are economically significant, especially as household debt continues to climb to new record levels.”

“We continue to see the spread of mortgage stress in areas away from the traditional mortgage belts. A rising number of more affluent households are also being impacted.”

Regional analysis shows that NSW has 238,755 households in stress (225,090 last month), VIC 236,544 (229,988 last month), QLD 146,497 (144,825 last month) and WA 118,860 (107,936 last month).

The probability of default fell a little, with around 9,000 in WA, around 8,500 in QLD, 11,500 in VIC and 12,400 in NSW. We are projecting mortgage interest rates will remain lower for longer now, and this has had a beneficial impact on our results. Probability of default extends our mortgage stress analysis by overlaying economic indicators such as employment, future wage growth and cpi changes.

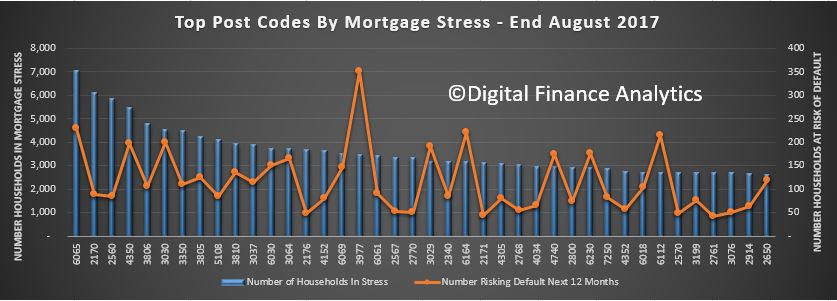

Here are the top counts of households in stress by post code.

[1] *RBA E2 Household Finances – Selected Ratios March 2016

[1] *RBA E2 Household Finances – Selected Ratios March 2016

Would be good to know what proportion in stress are in either mild stress or severe stress.

Would be extra interesting to know of those in stress, when they took out their mortgage, but obviously a lot of extra work for that.