The latest data from APRA, the monthly banking stats to December, provide data on the stock of loans and deposits held by the banks. Total housing loans on book were $1.42 trillion, up 0.7% from last month. Within the mix, owner occupied loans grew 1% ($898 bn) and investment loans by 0.17% ($518 bn). There were no declared adjustments between owner occupied and investment loans this month (first clear result for several months). Investment loans were 36.6% of book, still a big number.

The balance between $1.42 trillion and $1.52 trillion as reported today by the RBA relates to the non-bank sector.

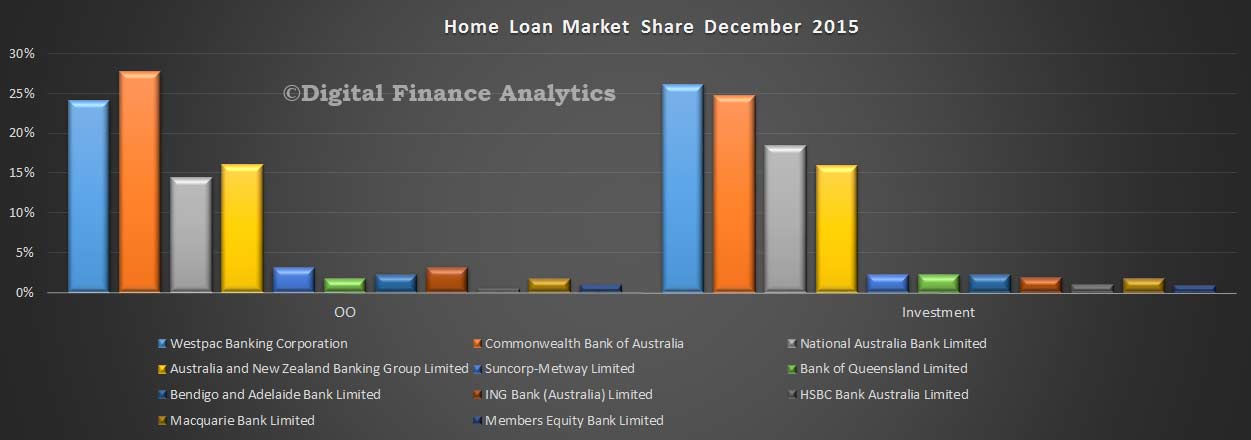

Looking at the individual lenders portfolios, CBA still has the largest owner occupied share, and Westpac the biggest share of investment loans.

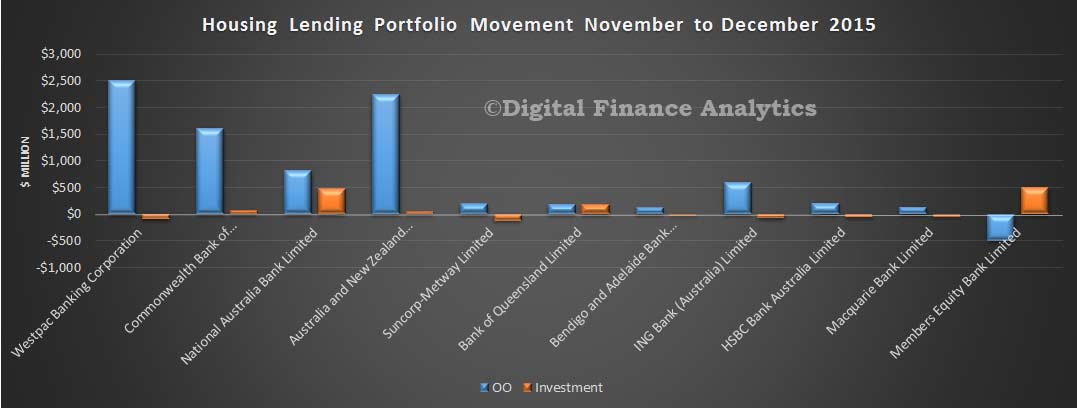

The main movements were in the owner occupied stream, with all the main lenders growing their footprint, other than Members Equity Bank who grew their investment loans. Among the majors, NAB made (net) most investment loans.

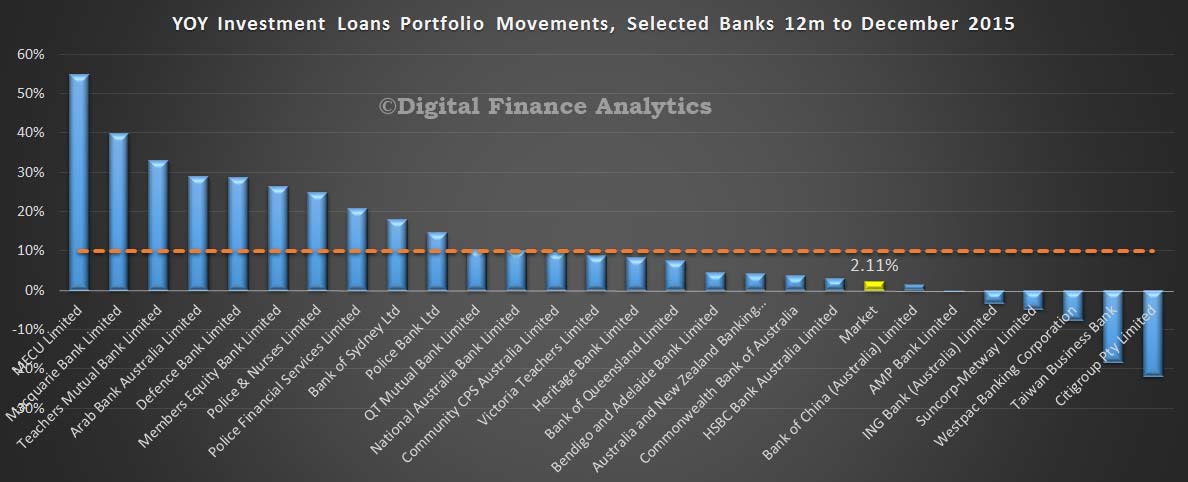

If we look at the 12 month portfolio movements by bank, we see that the investment loans market since January has now settled at 2.1% (after all the various tweaks and adjustments). This is below the APRA 10% speed limit. Now most of the major lenders are at or below the 10% hurdle, through a number of other players are still well above. Some, like Macquarie are explained by acquisitions, others by relative lending growth alone.

If we look at the 12 month portfolio movements by bank, we see that the investment loans market since January has now settled at 2.1% (after all the various tweaks and adjustments). This is below the APRA 10% speed limit. Now most of the major lenders are at or below the 10% hurdle, through a number of other players are still well above. Some, like Macquarie are explained by acquisitions, others by relative lending growth alone.

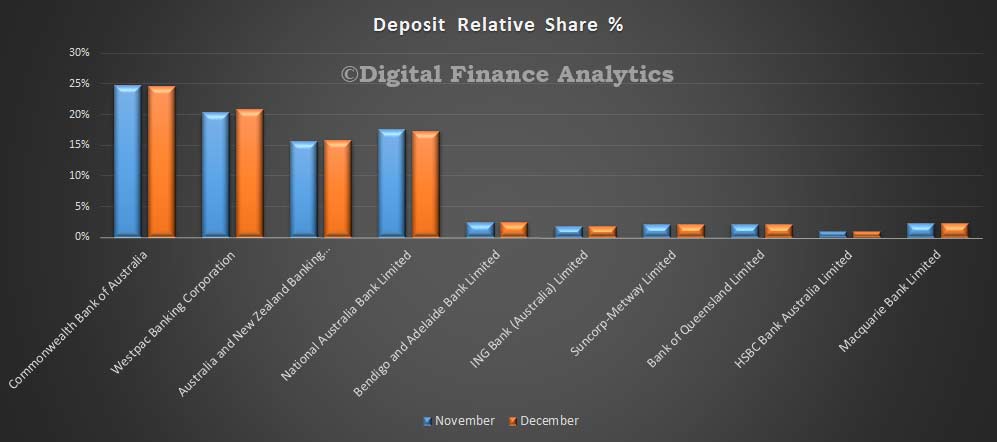

Turning to deposits, we see CBA still is the largest savings bank in Australia, though Westpac has been growing share, at the expense of NAB. Total deposits were $1.9 trillion, up $11 bn in the month – or 0.62%. This is a larger rise than the previous two months.

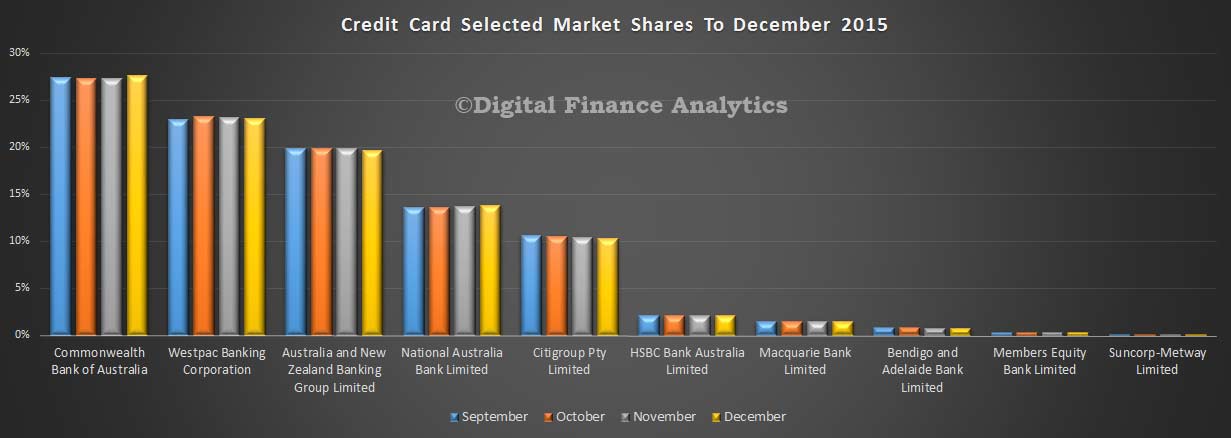

Looking at the cards portfolio, total balances were up slightly (thanks to Christmas) by $832 m to $42.2 bn. CBA lifted their share of cards balances, and they remain the largest cards player, followed by Westpac and ANZ Bank. We expect balances to fall in January as households repay their festive bloat.