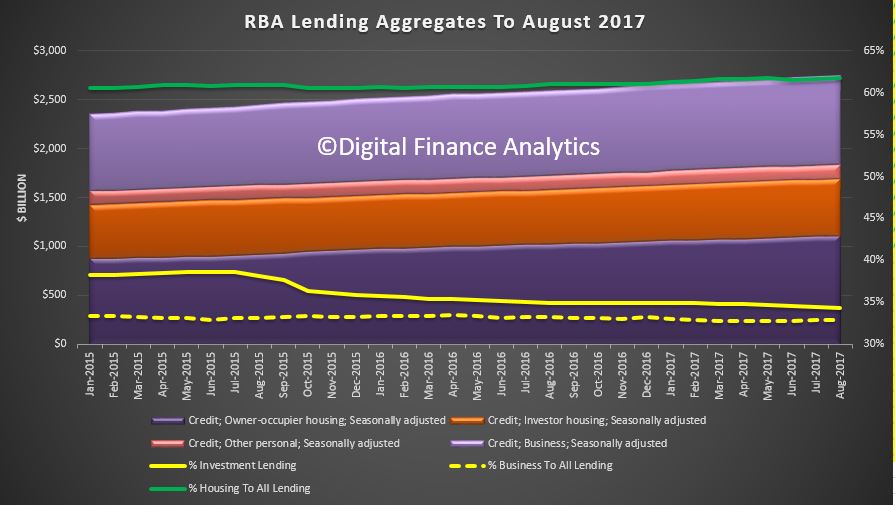

The latest RBA data on credit, to August 2017 tells a somewhat different story to the APRA data we discussed already. There were clearly adjustments in the system [CBA in particular?] and the non-bank sector is picking up some of the slack.

Overall housing credit rose 0.5% in August, and 6.6% year-ended August 2017. Personal credit fell again, down 0.2%, and 1.1% on a 12 month basis. Business credit also rose 0.5%, or 4.5% on annual basis. But overall lending for housing is still growing.

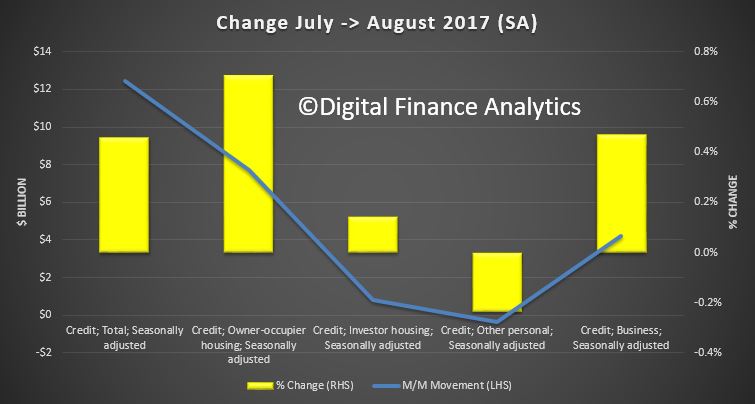

Here are the month on month (seasonally adjusted) movements. Owner occupied lending up $17.5 billion (0.68%), investment lending up $0.8 billion (0.14%), personal credit down $0.4 billion (-0.24%) and business lending up $4.2 billion or 0.47%.

Here are the month on month (seasonally adjusted) movements. Owner occupied lending up $17.5 billion (0.68%), investment lending up $0.8 billion (0.14%), personal credit down $0.4 billion (-0.24%) and business lending up $4.2 billion or 0.47%.

As a result, the proportion of credit for housing (owner occupied and investor) still grew as a proportion of all lending.

As a result, the proportion of credit for housing (owner occupied and investor) still grew as a proportion of all lending.

Another $1.7 billion of loans were reclassified in the month. This will give an impression of greater slowing investment loan growth as a result.

Another $1.7 billion of loans were reclassified in the month. This will give an impression of greater slowing investment loan growth as a result.

Following the introduction of an interest rate differential between housing loans to investors and owner-occupiers in mid-2015, a number of borrowers have changed the purpose of their existing loan; the net value of switching of loan purpose from investor to owner-occupier is estimated to have been $58 billion over the period of July 2015 to August 2017, of which $1.7 billion occurred in August 2017. These changes are reflected in the level of owner-occupier and investor credit outstanding. However, growth rates for these series have been adjusted to remove the effect of loan purpose changes.

3 thoughts on “RBA Says Housing Credit Still Growing”