There is bad news for those households with bank deposits. We have already seem a range of deposit repricing initiates by the banks, as they trim their deposit rates. But it is likely to get worst, as international sources of funding get cheaper, and changes to capital requirements are likely to translate to further rate cuts for savers down the track.

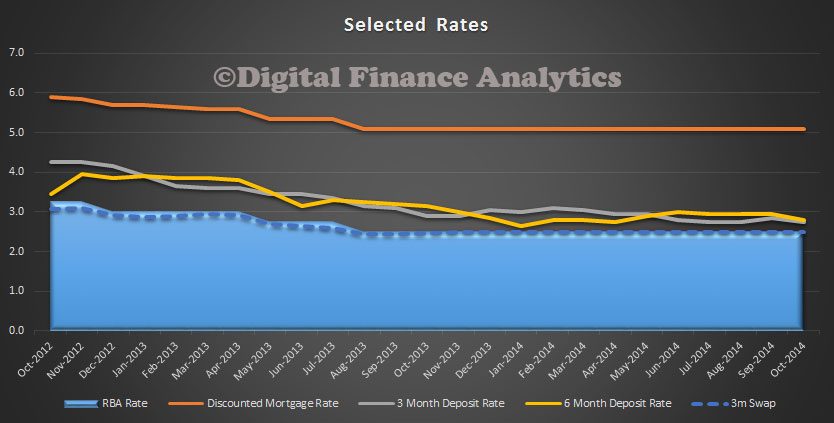

Rates have been coming down for those with bank deposits in recent months, and the rate of fall has accelerated recently. The chart below shows the movements of discounted mortgages, 3 month and 6 month deposits, and also the 3m swap rate, using RBA datsets.

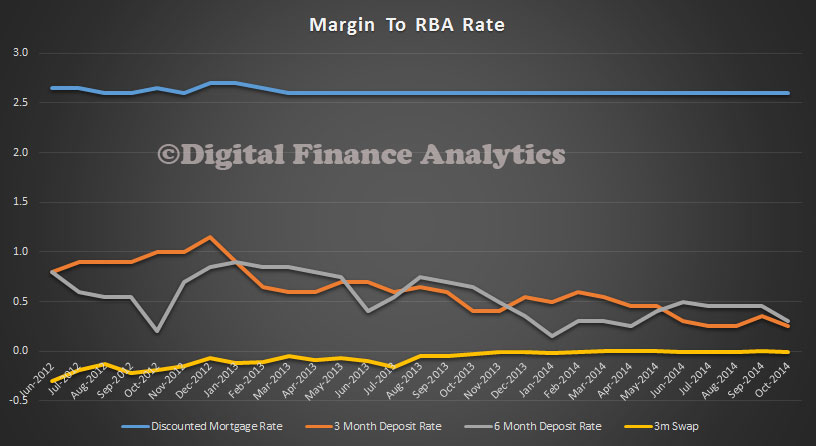

Whilst there is selective deeper discounting on the mortgage side, for some, savers are finding their returns falling. This is show most clearly by comparing the margins between the RBA rate, and loans and deposits. Despite the static RBA rate, deposit rates are falling.

Whilst there is selective deeper discounting on the mortgage side, for some, savers are finding their returns falling. This is show most clearly by comparing the margins between the RBA rate, and loans and deposits. Despite the static RBA rate, deposit rates are falling.

We know that overseas funding continues to improve, and as a result banks will be seeking to source funds through these channels. They are also discounting hard to get mortgage business. So to square the circle they are quietly trimming the rates to savers. We highlighted last week that bank deposits fell by 0.06% last month, to a value of $1.76 trillion, whereas lending grew.

We know that overseas funding continues to improve, and as a result banks will be seeking to source funds through these channels. They are also discounting hard to get mortgage business. So to square the circle they are quietly trimming the rates to savers. We highlighted last week that bank deposits fell by 0.06% last month, to a value of $1.76 trillion, whereas lending grew.

Looking ahead, with banks likely to have their wings clipped by the FSI report, due soon, and changes to capital following on which are likely to lift the costs of lending, the net result will be further pressure on saving rates, and more households looking for higher risk alternatives, as the RBA often mentions in their monthly statements. This continued fall of deposit returns hits older household segments the hardest, especially those banking on deposits to fund their retirements. Returns will be below inflation, so capital is effectively being eroded.

As a comparison, in the UK they have had 6 years of low deposits, and recently savers have found their rates being cut further. Many households are in financial stress as a result. In Australia, savers will either wear the losses, seek higher risk alternatives, or spend the money. Perhaps this latter course may assist an otherwise sluggish consumer sector. But it is not looking pretty.

3 thoughts on “Savers Are Going To Get Crunched”