In the latest RBA Bulletin there is an article on the Committed Liquidity Facility, which is a facility designed to support some of our major banks. Under the CLF, the Reserve Bank will provide an ADI with liquidity via repurchase agreements (repos), for a fee. Since the CLF was introduced in 2015, the number of ADIs that have applied to APRA to have a facility has risen from 13 to 15.

Under the Basel liquidity standard, the liquidity coverage ratio (LCR) requires authorised deposit-taking institutions (ADIs) to have enough high-quality liquid assets (HQLA) to cover their net cash outflows in a 30-day liquidity stress scenario. Jurisdictions with a clear shortage of domestic currency HQLA can use alternative approaches to enable financial institutions to satisfy the LCR – hence the CLF in Australia.

The RBA says the CLF has been in operation for five years and continues to be required given the still relatively low level of government debt in Australia. However, because the volume of HQLA securities has increased over recent years and they appear to have become more available for trading in secondary and repo markets, the Reserve Bank has assessed that the CLF ADIs should be able to raise their holdings to 30 per cent of the stock of HQLA securities. This increase will occur at a pace of 1 percentage point each year, commencing with an increase to 26 per cent in 2020. Taking into account how the CLF ADIs have responded to the framework between 2015 and 2019, the Reserve Bank has also concluded that the CLF fee should be increased from 15 basis points to 20 basis points by 2021; this is to proceed in two steps, with the fee rising to 17 basis points on 1 January 2020 and to 20 basis point on 1 January 2021.

These pricing changes will have only a minor impact on the CLF Banks in terms of their net interest margins, at a time when many other factors are in play, such as reductions in the RBA’s cash rate, competition for mortgages and the yield curve driving pricing in the 2-5 years portion of banks treasury portfolios.

But there are two bigger questions to ask and answer. First, given the size of Government debt now, and the flow of bonds available, why do we still need this facility at all?

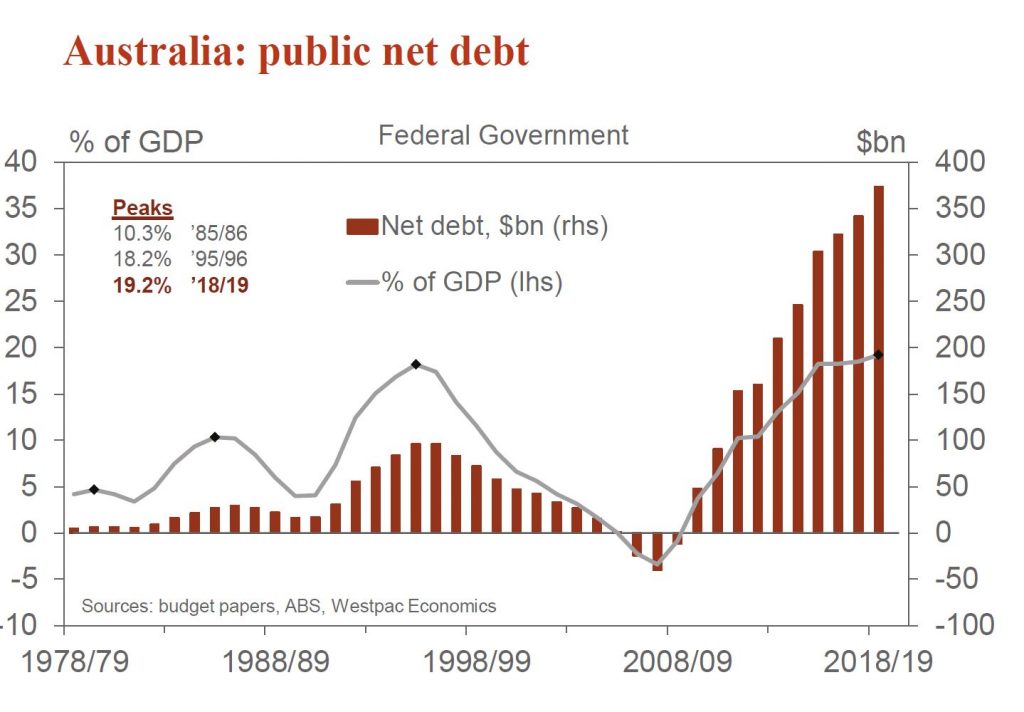

Net general government debt at June 2019 is $374bn (19.2% of GDP), some $12.5bn higher than forecast in the April 2019 Budget

The answer to that, and the second point is the CLF is essentially a back-door QE measure. If international liquidity became an issue, or if rate decreases triggered a capital flight, the CLF allows the RBA to step in and fund the banks’ funding shortfall from a loss of international investors, at rates below the banks’ international funding rates. Thus, high cost international funding by the banks can easily be replaced by cheap RBA funding through a form of QE or money printing subsidising bank profits and banker bonuses – for a short period.

This also distorts the markets because there are many lenders unable to get the CLF, creating a two-tier banking system with the “blessed” 15 supported by the CLF.

This is what the RBA says:

The Reserve Bank provides the Committed Liquidity Facility (CLF) as part of Australia’s

implementation of the Basel III liquidity standard.[1] This framework has been designed to improve the

banking system’s resilience to periods of liquidity stress. In particular, the liquidity coverage

ratio (LCR) requires authorised deposit-taking institutions (ADIs) to have enough high-quality liquid

assets (HQLA) to cover their net cash outflows in a 30-day liquidity stress scenario. Under the Basel

liquidity standard, jurisdictions with a clear shortage of domestic currency HQLA can use alternative

approaches to enable financial institutions to satisfy the LCR. These include the central bank offering a

CLF. This is a commitment by the central bank to provide funds secured by high-quality collateral through

the period of liquidity stress. This commitment can then be counted by the ADI towards meeting its LCR

requirement given the scarcity of HQLA. The Australian Prudential Regulation Authority (APRA) has

implemented the LCR in Australia, incorporating a CLF provided by the Reserve Bank.[2]

The CLF Is Required Due to the Low Level of Government Debt in Australia

The Australian dollar securities that have been assessed by APRA to be HQLA are Australian Government

Securities (AGS) and securities issued by the central borrowing authorities of the states and territories

(semis). All other forms of HQLA available in Australian dollars are liabilities of the Reserve Bank,

namely banknotes and Exchange Settlement Account (ESA) balances. For securities to be considered HQLA,

the Basel liquidity standard requires that they have a low risk profile and be traded in an active and

sizeable market. AGS and semis satisfy these requirements since they are issued by governments in

Australia and are actively traded in financial markets. In contrast, there is relatively little trading

in other key types of Australian dollar securities, such as those issued by supranationals and foreign

governments (supras), covered bonds, ADI-issued paper and asset-backed securities (Graph 1). Given

this, these securities are not classified as HQLA.

Graph 1

The supply of AGS and semis is not sufficient to meet the liquidity needs of the Australian banking

system. This reflects the relatively low levels of government debt in Australia (Graph 2). When the

CLF was first introduced in 2015, ADIs would have needed to hold around two-thirds of the stock of HQLA

securities to be able to cover their LCR requirements. Such a high share of ownership by the ADIs would

have reduced the liquidity of these securities, defeating the purpose of them being counted on as

HQLA.

Graph 2

Jurisdictions with low government debt have used a range of approaches to address the resulting shortage

of domestic currency HQLA. Australia is one of three countries that have put in place a CLF, along with

Russia and South Africa. Some other jurisdictions have allowed financial institutions to hold HQLA in

foreign currencies to cover their liquidity needs in domestic currency. The main downsides of the latter

approach is that it relies on foreign exchange markets to be functioning smoothly in a time of stress and

increases the foreign currency exposures in the banking system. Some jurisdictions have classified a

broader range of domestic currency securities as HQLA. However, this approach has not been taken in

Australia due to the low liquidity of Australian dollar securities other than AGS and semis.

The Conditions for Accessing the CLF

APRA determines which ADIs can establish a CLF with the Reserve Bank. Access is limited to those ADIs

domiciled in Australia that are subject to the LCR requirement.[3] Before establishing a CLF, these ADIs must

apply to APRA for approval. In these applications, the ADIs have to demonstrate that they are making

every reasonable effort to manage their liquidity risk independently rather than relying on the CLF. APRA

also sets the size of the CLF, both in aggregate and for each ADI.

The Reserve Bank makes a commitment under the CLF to provide a set amount of liquidity against eligible

securities as collateral, subject to the ADI having satisfied several conditions.[4] The ADI is

required to pay a CLF fee to the Reserve Bank that is charged on the entire committed amount (not just

the amount drawn). To access liquidity through the CLF, an ADI must make a formal request to the Reserve

Bank that includes an attestation from its CEO that the institution has positive net worth. The ADI must

also have positive net worth in the opinion of the Reserve Bank.

Under the CLF, the Reserve Bank will provide an ADI with liquidity via repurchase agreements (repos). In

a repo, funds are exchanged for high-quality securities as collateral until the funds are repaid. These

securities must meet criteria set by the Reserve Bank. The types of securities that the ADIs can hold for

the CLF include self-securitised residential mortgage backed securities (RMBS), ADI-issued securities,

supras, and other asset-backed securities. To protect against a decline in the value of these securities

should an ADI not meet its obligation to repay, the Reserve Bank requires the value of the securities to

exceed the amount of liquidity provided by a certain margin. These margins are set by the Reserve Bank to

manage the risks associated with holding these securities.[5] If the CLF is drawn upon, the ADI must also pay

interest to the Reserve Bank for the term of the repo at a rate set 25 basis points above the cash

rate.

The First Five Years of the CLF

Since the CLF was introduced in 2015, the number of ADIs that have applied to APRA to have a facility

has risen from 13 to 15.[6] Each year, APRA sets the total size of the CLF by taking the difference between the

Australian dollar liquidity requirements of the ADIs and the amount of HQLA securities that the Reserve

Bank assesses can be reasonably held by these ADIs (the CLF ADIs) without unduly affecting market

functioning.

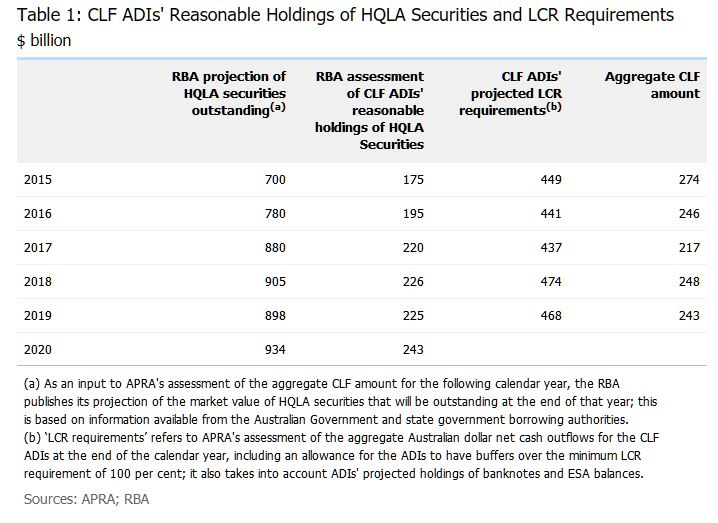

For 2015-19, the Reserve Bank assessed that the CLF ADIs could reasonably hold 25 per cent of

the stock of HQLA securities. In determining this, the Reserve Bank took into account the impact of the

CLF ADIs’ holdings on the liquidity of HQLA securities in secondary markets, along with the

holdings of other market participants. The volume of HQLA securities that the CLF ADIs could reasonably

hold increased from $175 billion in 2015 to $225 billion in 2019, reflecting growth in the stock of HQLA

securities (Table 1). Over the period, the CLF ADIs held a significantly higher share of the stock

of HQLA securities than in the years leading up to the introduction of the LCR (Graph 3). The CLF

ADIs have been holding a larger share of the stock of semis compared to AGS.

Graph 3

The CLF ADIs’ projected LCR requirements, which were used in calculating the CLF, increased

modestly in aggregate from $449 billion in 2015 to $468 billion in 2019. This increase can be entirely

explained by the CLF ADIs seeking to raise their liquidity buffers over time to be well above the minimum

LCR requirement of 100. Reflecting this, the aggregate LCR for these ADIs increased from around

120 per cent in 2015 to around 130 per cent in 2019; this was the case for their

Australian dollar liquidity requirements as well as for their requirements across all currencies

(Graph 4).[7]

Graph 4

The aggregate CLF amount is the CLF ADIs’ projected LCR requirements less the RBA’s

assessment of their reasonable holdings of HQLA securities. APRA reduced the aggregate size of the CLF

from $274 billion in 2015 to $243 billion in 2019. This reflected that the volume of HQLA securities that

the CLF ADIs could reasonably hold increased by more than their projected liquidity requirements over

this period.

From 2015 to 2019, the Reserve Bank charged a CLF fee of 15 basis points per annum on the

commitment to each ADI. The fee is set so that ADIs face similar financial incentives to meet their

liquidity requirements through the CLF or by holding HQLA. The amount of CLF fee paid by the CLF ADIs to

the Reserve Bank declined from $413 million in 2015 to $365 million in 2019, which is in line with the

reduction in the size of the CLF. Since the CLF was established, no ADI has drawn on the facility in

response to a period of financial stress.[8]

Assessing ADIs’ Reasonable Holdings of HQLA Securities

When assessing the volume of HQLA securities that the CLF ADIs can reasonably hold, the Reserve Bank

seeks to ensure that these holdings are not so large that they impair market functioning or liquidity.

For the period from 2015 to 2019, the Reserve Bank assessed that the CLF ADIs could reasonably hold

25 per cent of HQLA securities without materially reducing their liquidity. This was informed

by the fact that a large proportion of HQLA securities were owned by ‘buy and hold’

investors. These investors were price inelastic and generally did not lend these securities back to the

market, reducing the free float of HQLA securities. Many of these investors were non-residents (such as

sovereign wealth funds), which were holding nearly 60 per cent of the stock of HQLA securities

earlier in the decade (Graph 5). So overall, the Reserve Bank concluded that these bond holdings

were not contributing significantly to liquidity in the market.

Graph 5

Over recent years, the volume of HQLA securities has risen and they have become more readily available

in bond and repo markets (Table 1). The Australian repo market has grown considerably, driven by

more HQLA securities being sold under repo. Since 2015, non-residents have emerged as significant lenders

of AGS and semis (and borrowers of cash) in the domestic market (Graph 6). Over the same period,

repo rates at the Reserve Bank’s open market operations have risen relative to unsecured funding

rates (Graph 7). This is consistent with market participants financing a larger volume of HQLA

securities on a short-term basis through the repo market. For this assessment, the increased availability

of HQLA securities in the market suggests that the CLF ADIs should be able to hold a higher share of

these securities without impairing market functioning.

Graph 6

Graph 7

Analysis of transactions in the bond and repo markets using data from 2015–17 suggests that most

HQLA securities were being actively traded.[9] Monthly turnover ratios for AGS bond lines were well above

zero, and much higher than turnover ratios for other Australian dollar securities such as asset-backed

securities, covered bonds, ADI-issued paper and supras (Graph 1). Although semis bond lines were

traded less frequently than AGS, relatively few semis had low turnover ratios (Graph 8). As such,

some increase in ADIs’ holdings of AGS and semis would appear unlikely to jeopardise liquidity in

these markets.

Graph 8

Earlier in the decade, a ‘scarcity premium’ had emerged in the pricing of HQLA securities.

Australia’s relatively strong economic performance and AAA sovereign rating have been of

considerable appeal to investors with a preference for highly rated securities. Higher yields compared to

other AAA-rated sovereigns also contributed to strong demand from foreign investors, particularly for

AGS. The scarcity premium was most prominent before 2015, when the yield on 3-year AGS was well below the

expected cash rate over the equivalent horizon (as measured by overnight indexed swaps (OIS);

Graph 9). However, the scarcity premium has dissipated alongside an increase in the stock of AGS on

issue. This suggests that there is scope for the CLF ADIs to hold more HQLA securities without impairing

market functioning.

Graph 9

Given these developments, the Reserve Bank has assessed that the CLF ADIs should be able to increase

their holdings to 30 per cent of the stock of HQLA securities.[10] To

ensure a smooth transition and thereby minimise the effect on market functioning, the increase in the CLF

ADIs’ reasonable holdings of HQLA securities will occur at a pace of 1 percentage point per

year until 2024, commencing with an increase to 26 per cent in 2020.

The CLF Fee

The Reserve Bank sets the level of the CLF fee such that ADIs face similar financial incentives when

holding additional HQLA securities or applying for a higher CLF in order to satisfy their liquidity

requirements. A useful starting point to assess the appropriate CLF fee is to compare the yields on the

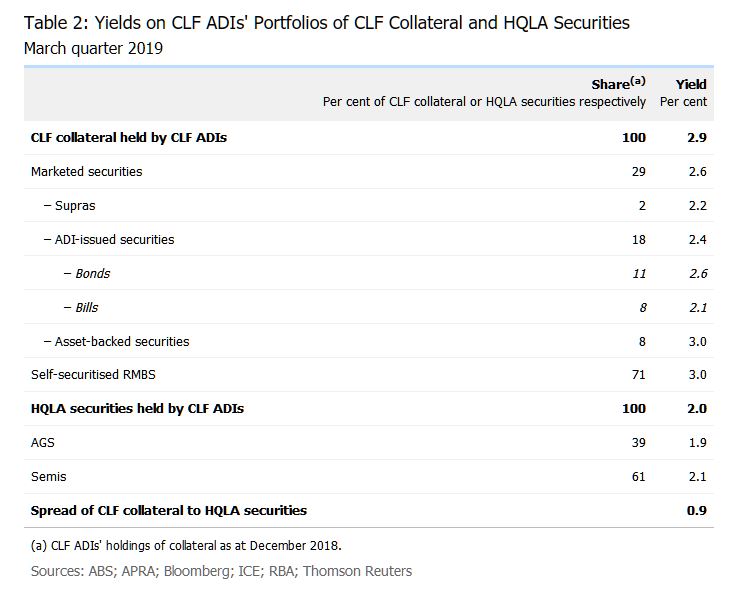

CLF collateral and the HQLA securities held by the relevant ADIs.[11] The Reserve Bank estimated that the

weighted average yield differential between the CLF collateral and the HQLA securities was around

90 basis points in the March quarter 2019 (Table 2). This includes the compensation required by

ADIs to account for the higher credit risk associated with holding CLF collateral rather than HQLA

securities, which would be a sizeable share of the spread. However, it is only the additional liquidity

risk associated with holding CLF collateral that should be reflected in the CLF fee. In practice,

adjusting the spread between CLF collateral and HQLA securities to remove the credit risk component is

not straightforward.

When the Reserve Bank set the CLF fee earlier this decade, it looked at repo rates on some CLF-eligible

securities to gauge how much a one-month liquidity premium might be worth. Before late 2013, it was

possible to separately identify repo rates on government securities (AGS and semis) and private

securities (such as ADI-issued securities) in the Reserve Bank’s market operations. Based on these

data, it was estimated that the one-month liquidity premium for private securities was less than

10 basis points in normal circumstances. However, given that part of the purpose of the liquidity

reforms was to recognise that the market had under-priced liquidity in the past, it was judged to have

been appropriate to set the fee at 15 basis points.

It has since become more difficult to gauge a liquidity premium by using repo rates. In particular, in

late 2013 the Reserve Bank ceased to charge different repo rates for government and private securities.

Instead, the Bank revised its margin schedule to manage the credit risk on different types of collateral

accepted under repo. Moreover, most of the collateral now being purchased by the Reserve Bank under repo

is HQLA securities. This suggests that repo rates mostly reflect the price for converting HQLA securities

into ESA balances, rather than CLF collateral into HQLA.

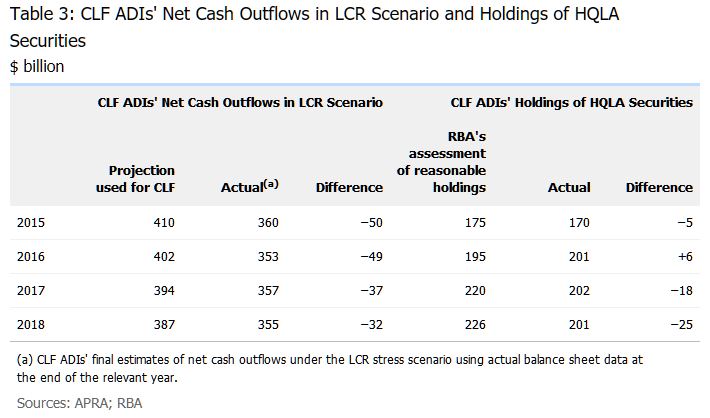

At the same time, it is now possible to take into account how the CLF ADIs have responded to the

existing framework when setting the future CLF fee. Since the CLF was introduced, the CLF ADIs (in

aggregate) have consistently overestimated their liquidity requirements (Table 3). This has resulted

in the CLF ADIs being granted larger CLF amounts, which they have mainly used to hold larger buffers

above the minimum required LCR of 100 (Graph 4).[12] In recent years, the CLF ADIs have also been

holding fewer HQLA securities than the Reserve Bank had judged could be reasonably held without impairing

the market for HQLA securities. Taken together, these two observations suggest that the CLF fee should be

set at a higher level in future.

However, there is uncertainty about the exact level of the fee that would make ADIs indifferent between

holding more HQLA or applying for a larger CLF. If the CLF fee is set too high, this could trigger a

disruptive shift away from using the facility and distort the markets that use HQLA. This has potential

implications for the implementation of monetary policy, since the market that underpins the cash rate

involves the trading of ESA balances, which are also HQLA.[13] The remuneration on ESA balances is purposefully

set at a rate of 25 basis points below the cash rate target in order to encourage ADIs to recycle

their surplus ESA balances rather than holding them. There are scenarios where holding ESA balances could

be a cheaper way to satisfy the LCR than holding HQLA securities. For instance, earlier in the decade,

the yield on AGS was at or below the expected return from holding ESA balances (Graph 9). In this

context, the CLF fee should be set such that ADIs would not have an incentive to meet their LCR

requirements by holding excessive ESA balances.

As a result of these considerations, the RBA has concluded that the CLF fee should be increased

moderately. This should ensure that ADIs have strong incentives to manage their liquidity risk

appropriately, without generating unwarranted distortions in the markets that use HQLA. To ensure a

smooth transition by minimising the effect on market functioning, the increase will occur in two steps,

with the CLF fee rising to 17 basis points on 1 January 2020 and to 20 basis points on 1

January 2021.[14]

The RBA’s Christopher Kent, Assistant Governor (Financial Markets) spoke about the CLF today. Look carefully, as banks effectively can cross collateralise via each others mortgage backed securities – what could possibly go wrong?

I’d like to thank Bloomberg for the opportunity to speak to you about the committed liquidity

facility (CLF). The CLF has been in place now for almost five years.

As we announced in June, after a careful review, the RBA will be adjusting the settings of the CLF

starting from next year.[1] Today, I thought it would be helpful to discuss the developments that have led us to

make these adjustments. We have also published a detailed article on this on the RBA’s

website.[2] But first, let’s review why we needed the CLF in the first place.

Why Do We Need a CLF?

The global financial crisis highlighted how important it is for banks to manage their liquidity risk.

During the crisis, many banks overseas faced significant liquidity problems having not paid enough

attention to their liquidity management in the lead up to the crisis.

Following this experience, the Basel Committee on Banking Supervision proposed tougher liquidity

requirements as part of its broader package of reforms, known as the Basel III regulations. These

changes have made the banking system more resilient to periods of financial market stress.

One of the key planks of the requirement to increase liquidity of the banks was the introduction of the

liquidity coverage ratio (LCR). The LCR requires banks to have enough high-quality liquid assets (HQLA)

to cover their estimated net cash outflows during a scenario that entails a 30-day period of stress. The

idea is that a bank experiencing stress will have enough liquid assets that they can use to meet their

short-term liquidity needs. In this way, each bank holds a sufficient amount of HQLA as self-insurance

against liquidity risk. Like all insurance, this comes at a cost. In this case, the cost to each bank is

incurred because the HQLA earn a lower yield than alternative, less liquid assets that the bank could

otherwise hold, such as mortgages or business loans.

For HQLA securities to be of sufficient quality and liquidity, they should be both low risk and

actively traded in markets. In Australia’s case, Australian Government Securities (AGS) and

securities issued by the state and territory borrowing authorities (semis) meet this test. In contrast,

there is relatively little trading in other Australian dollar securities, such as those issued by

foreign agencies (supras), banks and securitisation trusts (Graph 1).

Graph 1

However, there is less government debt in Australia relative to the size of the banking system, and the

economy more generally, than is the case in many other countries (Graph 2). This means that there

are fewer HQLA in Australia. Indeed, back in 2015, if there had been no other way for Australian banks

to meet their LCR, collectively they would have had to have held around two-thirds of the total stock of

AGS and semis. And if the banks had held such a high share of those government securities, the liquidity

of those markets would have been substantially impaired, thereby defeating the purpose of them being

counted on as HQLA.

Graph 2

In recognition of this issue, the Basel liquidity standards allow jurisdictions with limited HQLA to

use alternative approaches. One of those approaches is for the central bank to offer a facility to

provide banks with a guaranteed source of liquidity.[3] And so the CLF was born. This entails the central

bank committing to stand ready to provide a bank with liquidity against high-quality collateral that

would otherwise be illiquid in the market. This commitment can be counted by banks towards meeting their

LCR. In return for the CLF, banks are charged a fee on the entire committed amount, whether or not it is

actually drawn upon. This fee is akin to the insurance premium that banks would implicitly pay if

instead of the CLF, they had to hold additional HQLA.

Starting from 2015, the RBA has provided the CLF as part of Australia’s implementation of the

Basel III liquidity reforms.[4]

The First Five Years of the CLF

Under the CLF, the RBA commits to provide liquidity under repo against securities eligible in its

operations. To access the CLF, a bank must meet several conditions: it must have paid its CLF fee; the

bank’s CEO has to have attested that the bank has positive net worth; and the RBA has to have

judged that this is indeed the case.[5]

In the five years since the CLF was introduced, 15 banks have applied to APRA for access to the

CLF. None of these banks have needed to draw on the facility in response to a period of financial

stress.

Each year, APRA determines the total size of the CLF. It’s the difference between the banking

system’s liquidity needs and the amount of AGS and semis that the RBA assesses that the banks can

hold without impairing the functioning of the market. The size of the CLF was set at $274 billion in

2015. As an input to this, the RBA assessed that the banks could reasonably hold 25 per cent

of the stock of AGS and semis. This was a sizeable step up from their holdings earlier in the decade

(Graph 3).

Graph 3

However, since then, the stock of AGS and semis has increased by almost a third. In comparison, the LCR

requirements of the banks have been little changed. So the banks can hold more HQLA securities compared

to their liquidity needs. As a result, the size of the CLF has declined to just below $250 billion. The

increase in AGS and semis also means that the shortage of HQLA securities is not as large as it once

was, although there is still a shortage.

Reassessing the Banks’ Reasonable Holdings of HQLA Securities

To assess the amount of HQLA securities that the banks can reasonably hold, the RBA takes into account

the behaviour of other holders of these securities, along with conditions in bond and repo markets.

In 2015, a large share of Australian government debt was held by what can be described as ‘buy

and hold’ investors. That is, these investors were not particularly sensitive to the prices of

these securities, and typically they did not contribute to liquidity in the market. Many of these

investors were non-residents, which were holding nearly 60 per cent of the total stock of HQLA

securities earlier in the decade (Graph 4).

Graph 4

However, over recent years more HQLA securities have become available for use as collateral. In

particular, the Australian repo market has grown substantially, driven by more HQLA securities being

sold under repo. Of note, non-residents have been lending more of their holdings of AGS and semis back

into the domestic market (Graph 5).

Graph 5

Also, our analysis of transactions in bond and repo markets demonstrates that most HQLA securities were

being actively traded. Turnover ratios for individual AGS bond lines were well above zero and much

higher than for other Australian dollar securities. Although semis were traded less frequently than AGS,

only a small share of the bond lines of semis had low turnover ratios (Graph 6). Given this, it

appears unlikely that a moderate increase in banks’ holdings of AGS and semis would present a

problem for liquidity in these markets.

Graph 6

Another issue we considered in 2015 was the ‘scarcity premium’ that was present for AGS.

Australia’s relatively strong economic performance and AAA credit rating have been very appealing

for investors globally. The scarcity premium was prominent in the years leading up to 2015, when the

yield on AGS was well below the expected cash rate over the period to maturity (Graph 7). Since

then, however, the scarcity premium has gradually dissipated. This has occurred alongside an increase in

the stock of AGS. It is also consistent with these securities being less tightly held. The combination

of these changes suggests that the banks can now hold a higher share of the AGS on issue without

impairing the functioning of the market.

Graph 7

This brings us to the first of two changes that we have made to the settings of the CLF. We have

assessed that banks can increase their holdings of HQLA securities from 25 to 30 per cent of

the outstanding stock. This will result in the CLF being smaller than it otherwise would have been. To

minimise the effect of this change on the market, the increase will occur at the gradual pace of

1 percentage point each year, beginning with an increase to 26 per cent in 2020.

Setting the CLF Fee

The second change we are implementing relates to the CLF fee.

The CLF fee should be set at a level at which banks will face similar financial incentives to meet

their LCR through the CLF or by holding HQLA (if there were enough available). However, determining this

level of the fee is easier to do in theory than in practice.

The starting point for determining the fee is to make use of the spread between the yields on HQLA

securities and the collateral that the banks hold for the CLF. This collateral is all eligible for the

RBA’s market operations, and is mainly the banks’ self-securitised residential mortgage

backed securities. We have estimated that this spread was around 90 basis points earlier this year.

But the higher yield on CLF collateral reflects compensation for a variety of risks. In particular, a

sizeable share of the spread owes to the higher credit risk on these securities. However, the CLF fee

should only reflect the liquidity risk component of the spread, and that is very difficult to identify

separately.[6]

When the Reserve Bank set the CLF fee earlier this decade, it looked at repo rates on some CLF-eligible

securities to gauge how much a one-month liquidity premium might be worth. The answer was not very much

in normal circumstances. Based on data from the RBA’s open market operations, it was estimated to

be around 10 basis points. However, given that part of the point of the liquidity reforms was to

recognise that the market had underpriced liquidity in the past, it was judged to have been appropriate

to set the fee at 15 basis points.

Now that we have several years of experience with the CLF, we can look back and see how the banks have

responded to the existing framework. Since the CLF was introduced, the banks, in total, have

consistently overestimated their ‘net cash outflow’ projections in their CLF applications

for the following year.[7] These projections were used by APRA to determine the size of the CLF. As a result, the

banks have been granted a larger CLF than would have been the case had the net cash outflow projections

been more accurate ex ante (Graph 8). In recent years, the banks have also been

holding fewer HQLA securities than the RBA judged that they could reasonably hold. Taken together, these

observations suggest that the CLF fee should be set at a higher rate in the future.

Graph 8

A higher CLF fee will help to make the banks indifferent between holding more HQLA securities and asking

for a larger CLF. However, if the fee is too high, this could trigger a disruptive shift away from using

the CLF facility and create distortions in the markets that use HQLA. Accordingly, we have concluded

that the fee should be increased moderately and occur in two steps. The fee will rise from 15 to

17 basis points in January 2020 and to 20 basis points in January 2021.

When taken together, these two changes to the settings for the CLF will result in a small increase in

the cost of the CLF for the banks. To show this, we can fully apply the new settings to the current CLF

amounts, assuming everything else is held constant. If the banks were holding the higher level of AGS

and semis that the RBA has assessed would be reasonable, this would reduce the size of the CLF from just

below $250 billion to around $200 billion. If we then apply the 5 basis points total increase

in the CLF fee, collectively the banks would pay around $30 million more than they do currently for the

liquidity commitment they receive from the RBA.[8]

Conclusion

In conclusion, the CLF is important for Australia’s implementation of the Basel III liquidity

reforms. The facility has been working well, but after five years it is time to make some modest and

gradual adjustments to the settings, in a way that reduces the need of the banks to make use of the CLF

while also increasing their cost of doing so a little. In combination, these changes will help to ensure

that the banks continue to have strong incentives to manage their liquidity risk appropriately.

Following a review, the Reserve Bank has assessed that Authorised Deposit-taking Institutions (ADIs) using the Committed Liquidity Facility (CLF) can increase their holdings of high quality liquid assets (HQLA) from 25 to 30 per cent of the stock of HQLA securities. This change is possible because the volume of HQLA securities has risen over recent years. To minimise the effect on market functioning, the increase will occur at a pace of 1 percentage point per year until 2024, commencing with an increase to 26 per cent in 2020.

The Reserve Bank has also assessed that the CLF fee should be increased from 15 to 20 basis points

per annum on the size of the commitment to each ADI. The fee is set so ADIs face similar financial

incentives to meet their liquidity requirements through the CLF or by holding HQLA. To minimise the

effect on market functioning, the increase will occur in two steps, with the CLF fee rising to

17 basis points on 1 January 2020 and to 20 basis points on 1 January 2021.

The Reserve Bank will provide further information about these adjustments in a speech to be scheduled

in July.

Background

Since January 2015, the Reserve Bank has provided the CLF as part of Australia’s implementation

of the Basel III liquidity reforms. Under APRA’s liquidity standard, ADIs that are required to

meet the liquidity coverage ratio (LCR) need to hold enough HQLA to be able to respond to an acute

stress scenario. The Australian dollar securities that have been assessed by APRA to meet the

requirements to be HQLA are Australian Government Securities (AGS) and securities issued by the central

borrowing authorities of the states and territories (semis). The CLF is required because of the limited

supply of AGS and semis, reflecting relatively low levels of government debt in Australia.

As an alternative to holding HQLA to meet the LCR, ADIs can apply to APRA to establish a CLF with the

Reserve Bank. This enables them to access a set amount of liquidity from the Reserve Bank under repo

against eligible securities as collateral. These ADIs are required to meet several conditions, including

paying the CLF fee. Each year, APRA sets the total size of the CLF by taking the difference between the

liquidity requirements of the CLF ADIs and the amount of HQLA securities that the Reserve Bank assesses

can be reasonably held by the CLF ADIs without unduly affecting market functioning. For more

information, see Domestic Market Operations.

APRA today published a letter relating to the Committed Liquidity Facility which is available to just 15 of the banks in Australia (The LCR banks). These have the back-stop option of calling on funds from the RBA to buttress their liquidity in case of need – so they can meet their obligations under the Basel III regime.

For a fee, if used, these banks essentially have a safety net in times of distress. Now APRA has outlined the arrangements for next year. Of course the other lenders have to operate without these supports.

More evidence of a lack of a level playing field in the system, and how the regulators are supporting the big end of town. No surprise then that big players are regarded by the markets as too big to fail.

But as Australian Government debt is hurtling beyond $500 billion, I have to say their so called justification – lack of liquidity in the local securities (mainly Australian Government Securities and securities issued by the borrowing authorities of the states and territories) is wearing a bit thin.

Why is this facility needed at all?

This is what APRA said today:

The Australian Prudential Regulation Authority (APRA) is today releasing aggregate results on the Committed Liquidity Facility (CLF) established between the Reserve Bank of Australia (RBA) and certain locally incorporated ADIs that are subject to the Liquidity Coverage Ratio (LCR).

APRA implemented the LCR on 1 January 2015. The LCR is a minimum requirement that aims to ensure that ADIs maintain sufficient unencumbered high-quality liquid assets (HQLA) to survive a severe liquidity stress scenario lasting for 30 calendar days. The LCR is part of the Basel III package of measures to strengthen the global banking system.

In December 2010, APRA and the RBA announced that ADIs subject to the LCR will be able to establish a CLF with the RBA. The CLF is intended to be sufficient in size to compensate for the lack of sufficient HQLA (mainly Australian Government Securities and securities issued by the borrowing authorities of the states and territories) in Australia for ADIs to meet their LCR requirements. ADIs are required to make every reasonable effort to manage their liquidity risk through their own balance sheet management before applying for a CLF for LCR purposes.

Committed Liquidity Facility for 2019

All locally incorporated LCR ADIs were invited to apply for a CLF amount to take effect on 1 January 2019. All fifteen ADIs chose to apply. Following APRA’s assessment of applications, the aggregate Australian dollar net cash outflow (NCO) of the fifteen ADIs was estimated at approximately $381 billion. The total CLF amount allocated for 2019 (including an allowance for buffers over the minimum 100 per cent requirement) is approximately $243 billion.

The CLF will enable participating ADIs to access a pre-specified amount of liquidity by entering into repurchase agreements of eligible securities outside the Reserve Bank’s normal market operations. To secure the Reserve Bank’s commitment, ADIs will be required to pay ongoing fees. The Reserve Bank’s commitment is contingent on the ADI having positive net worth in the opinion of the Bank, having consulted with APRA.

The facility will be at the discretion of the Reserve Bank. To be eligible for the facility, an ADI must first have received approval from APRA to meet part of its liquidity requirements through this facility. The facility can only be used to meet that part of the liquidity requirement agreed with APRA. APRA may also ask ADIs to confirm as much as 12 months in advance the extent to which they will be relying on a commitment from the Bank to meet their LCR requirement.

The Fee

In return for providing commitments under the CLF, the Bank will charge a fee of 15 basis points per annum, based on the size of the commitment. The fee will apply to both drawn and undrawn commitments and must be paid monthly in advance. The fee may be varied by the Bank at its sole discretion, provided it gives three months notice of any change.

Eligible Securities

Securities that ADIs can use under the CLF will include all securities eligible for the Reserve Bank’s normal market operations. In addition, for the purposes of the CLF, the Reserve Bank will allow ADIs to present certain related-party assets issued by bankruptcy remote vehicles, such as self-securitised residential mortgage-backed securities (RMBS). This reflects a desire from a systemic risk perspective to avoid promoting excessive cross-holdings of bank-issued instruments. Should the ADI lack a sufficient quantity of residential mortgages, other ‘self-securitised’ assets may be considered, with eligibility assessed on a case-by-case basis.

The Reserve Bank has discretion to broaden the eligibility criteria and conditions for the various asset classes at any time. The Bank will provide one years notice of any decision to narrow the criteria for the facility.

Interest Rate

For the CLF, the Bank will purchase securities under repo at an interest rate set 25 basis points above the Board’s target for the cash rate, in line with the current arrangements for the overnight repo facility.

Margining

The initial margins that the Reserve Bank will apply to eligible collateral will be the same as those used in the Bank’s normal market operations. Consistent with current practice, each day the Bank will re-value all securities held under repurchase agreements at prevailing market prices.

Termination

Subject to the ADI having positive net worth, the Reserve Bank will give at least 12 months notice of any intention to terminate the CLF. The Bank’s commitment to any individual ADI will lapse if the fee is not paid.

An important post from Macrobusiness (MB) by the excellent Leith van Onselen which opens the can of worms which is the RBA’s Committed Liquidity Facility (a.k.a. Bank Safety Net or Unofficial Government Guarantee). Its all about the RBA’s version of QE!

He says:

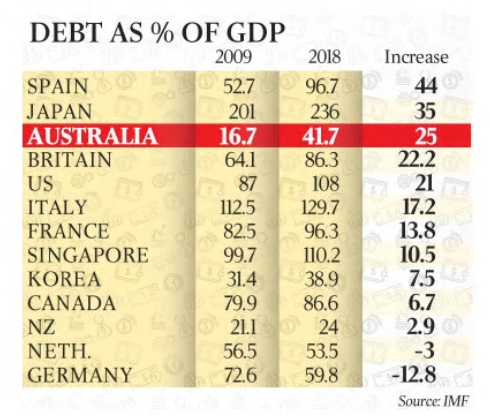

Figures from the International Monetary Fund (IMF) show that Australian government debt has risen faster than most other developed nations, increasing from 16.7% of GDP to an expected 41.7% this year – a jump of 25 percentage points. From The Australian:

The IMF report comes as Scott Morrison prepares to unveil next month’s budget, which will recycle improved company tax flows into personal income tax cuts while taking on more debt to finance infrastructure development. The Treasurer argues that the government is no longer borrowing to finance daily running costs but just to cover infrastructure and defence investments.

The mid-year budget update in December showed gross debt peaking at $591 billion in 2019-20, having hit $500bn in 2016-17. Gross debt stood at $319bn when the Coalition took office in 2013.

The IMF predicts this year will be the peak for Australian gross debt at 41.7 per cent of GDP, before a decline to 32.2 per cent over the next five years…

Although the IMF projects that Australia’s federal and state budgets will be back in surplus by 2020, it says there will be a continuing need to raise funds to roll over debts as they mature.

We think the projected return to surplus by 2020 is wishful thinking, given:

Commodity prices will likely fall, draining company profits, national income, and company tax revenue;

The housing downturn will dampen consumer spending, jobs and growth, draining company and personal income tax revenue; and

We are likely to see tax cuts offered from both sides in the upcoming federal election campaign.

Regardless, there is another important question that is rarely asked outside of MB: why is the Reserve Bank of Australia (RBA) persisting with the Committed Liquidity Facility (CLF) when there is now so much government debt on issue?

The CLF was established in late-2011 in order to meet the Basel III liquidity reforms. Below is the RBA’s explanation of the CLF [my emphasis]:

The facility, which is required because of the limited amount of government debt in Australia, is designed to ensure that participating authorised deposit-taking institutions (ADIs) have enough access to liquidity to respond to an acute stress scenario, as specified under the liquidity standard…

The CLF will enable participating ADIs to access a pre-specified amount of liquidity by entering into repurchase agreements of eligible securities outside the Reserve Bank’s normal market operations. To secure the Reserve Bank’s commitment, ADIs will be required to pay ongoing fees. The Reserve Bank’s commitment is contingent on the ADI having positive net worth in the opinion of the Bank, having consulted with APRA.

The facility will be at the discretion of the Reserve Bank. To be eligible for the facility, an ADI must first have received approval from APRA to meet part of its liquidity requirements through this facility. The facility can only be used to meet that part of the liquidity requirement agreed with APRA. APRA may also ask ADIs to confirm as much as 12 months in advance the extent to which they will be relying on a commitment from the Bank to meet their LCR requirement.

The Fee

In return for providing commitments under the CLF, the Bank will charge a fee of 15 basis points per annum, based on the size of the commitment. The fee will apply to both drawn and undrawn commitments and must be paid monthly in advance. The fee may be varied by the Bank at its sole discretion, provided it gives three months notice of any change…

Interest Rate

For the CLF, the Bank will purchase securities under repo at an interest rate set 25 basis points above the Board’s target for the cash rate, in line with the current arrangements for the overnight repo facility.

In light of the federal budget deficit projected to balloon out to nearly $600 billion, the question for the RBA is: shouldn’t the CLF be unwound and the banks instead be required to hold government bonds, as initially required under Basel III?

Bonds on issue are roughly triple that of when the CLF was first announced, so surely the RBA should amend the liquidity rules so that Australia’s ADIs are forced to purchase government bonds, so that the size of the CLF requirement decreases?

The most likely reason is because the RBA wants to keep open the option of bailing-out the banks. As noted by Deep T:

When there is capital flight due to official interest rate decreases, the RBA could and would step in and fund the banks’ funding shortfall from a loss of international investors using the Committed Liquidity Facility at rates below the banks’ international funding rates. The CLF used in these circumstances would be a form of quantitive easing and would have a dampening effect on mortgage rates by subsidising bank borrowing rates but could never be a lasting solution and only have limited effect in the long term. So yes, high cost international funding by the banks can easily be replaced by cheap RBA funding through a form of QE or money printing subsidising bank profits and banker bonuses.

The fact of the matter is the CLF represents another subsidy to the banks. The cost of the CLF is very low – i.e. 15bps pa – compared to the alternative. The CLF allows ADIs to originate mortgage assets and create RMBS rather than buying government bonds. The net spread on mortgage assets or RMBS compared to government bonds is much greater than 15bps pa, thus representing a significant direct subsidy to the banks.

MB reader, Jim, nicely dissected the lunacy of the CLF in a comment in 2016:

You’ve missed the real beauty of the CLF, and APS210

So the banks are forced to hold ‘as much as possible’ qualifying Tier 1 securities to meet their APS210 requirements. But… even with the large commonwealth government deficit, there still isn’t enough CGS to go round (CGS and TCorp bonds only qualify for Tier 1 securities under APS210).

Which is why the RBA invented the CLF. The CLF allows, no, it requires the banks to:

– hold their own securitised bonds on their balance sheet to qualify as ‘liquid assets’

– buy each other’s bonds to qualify as ‘liquid assets’

So, ANZ, CBA, NAB and WBC each have around $50bn of their own off balance sheet mortgages sitting back on their balance sheet to protect them against a ‘liquidity event’. Then they each have around $10bn each of each other’s bonds, so NAB holds around $50bn of WBC/ANZ/CBA bonds etc.

And if / when the liquidity shit hits the fan (e.g. foreigners stop buying the bank’s bonds), the banks can swap them into the RBA for a 15bps fee.

So the RBA will be forced to sit on about half a trillion dollars of Aussie bank paper ($100bn each plus a little more for CBA and WBC, plus Suncorp, Bendigo etc). Just think what THAT would do to your graph of yellow lines – more than double it in an instance.

So the CLF is not about government debt, its about bank debt, and how the RBA has bent over forward for the banks. Having worked in treasury at a Big 4, the CLF is the biggest joke under the sun – a guaranteed way to print money for the banks. This is why the fixed income desks at banks are always the best paying – those guys are paid to buy and hold bank bonds under APS210 requirements.

Do an investigation on how much REAL systemic debt is sitting in the banking system – the RBA has made itself lender of last resort to over $500bn worth of debt.

The bottom line is that with the stock of outstanding Commonwealth debt now so large (and still growing), the rationale for maintaining the CLF has evaporated. But don’t expect any action from the RBA, which wants to maintain the capability of bailing-out the banks via its own form of quantitative easing.

Blog")

For a fee, if used, these banks essentially have a safety net in times of distress. Now APRA has outlined the arrangements for next year. Of course the other lenders have to operate without these supports.

For a fee, if used, these banks essentially have a safety net in times of distress. Now APRA has outlined the arrangements for next year. Of course the other lenders have to operate without these supports. He says:

He says: