Chairman Rod Sims has today announced the ACCC’s compliance and enforcement priorities for 2018 at a CEDA event in Sydney.

He signalled that the ACCC will shortly release its interim report into residential mortgage pricing and a key focus will be on transparency, particularly how the major banks balance the interests of consumers and shareholders in making their interest rate decisions.

This year, the regulator will focus on consumer issues in broadband services and energy, competition in the financial services and commercial construction sectors, systemic consumer guarantee issues, and conduct that may contravene the new misuse of market power and concerted practices provisions.

“As I have repeatedly said, Australia faces an energy affordability crisis. This has upended one of Australia’s core sources of competitive advantages, and caused significant consumer harm. The ACCC’s retail electricity pricing inquiry report and the ACCC’s wholesale gas inquiry have given us, and the wider community, a far stronger understanding of the issues and pressures around rising energy prices,” said Mr Sims.

“Armed with the clear findings on the causes of the problem, the ACCC will now focus on making recommendations that will improve electricity affordability across the National Electricity Market and provide recommendations for reform in our final report at the end of June 2018.”

“Consumer issues in the provision of broadband services, including addressing misleading speed claims and statements made during the transition to the NBN, have become one of the ACCC’s most prominent issues in the past two years and highlights the importance of both our consumer and competition focus.”

“The first report of the ACCC’s Measuring Broadband Australia program will be released shortly, and our commitment to truth in advertising related to broadband speeds is making it easier for Australians to choose a service provider. You have seen a number of ACCC enforcement actions in 2017 and can expect further interventions this year.”

The ACCC is also well placed to play a role in consumer and competition issues relating to access to data, as recognised by the government.

“This is a hugely important pro-competition and pro-consumer innovation. At the heart of the proposals is giving consumers access to data that is held about them by business, including the ability to direct that such data be copied and provided to a third party.”

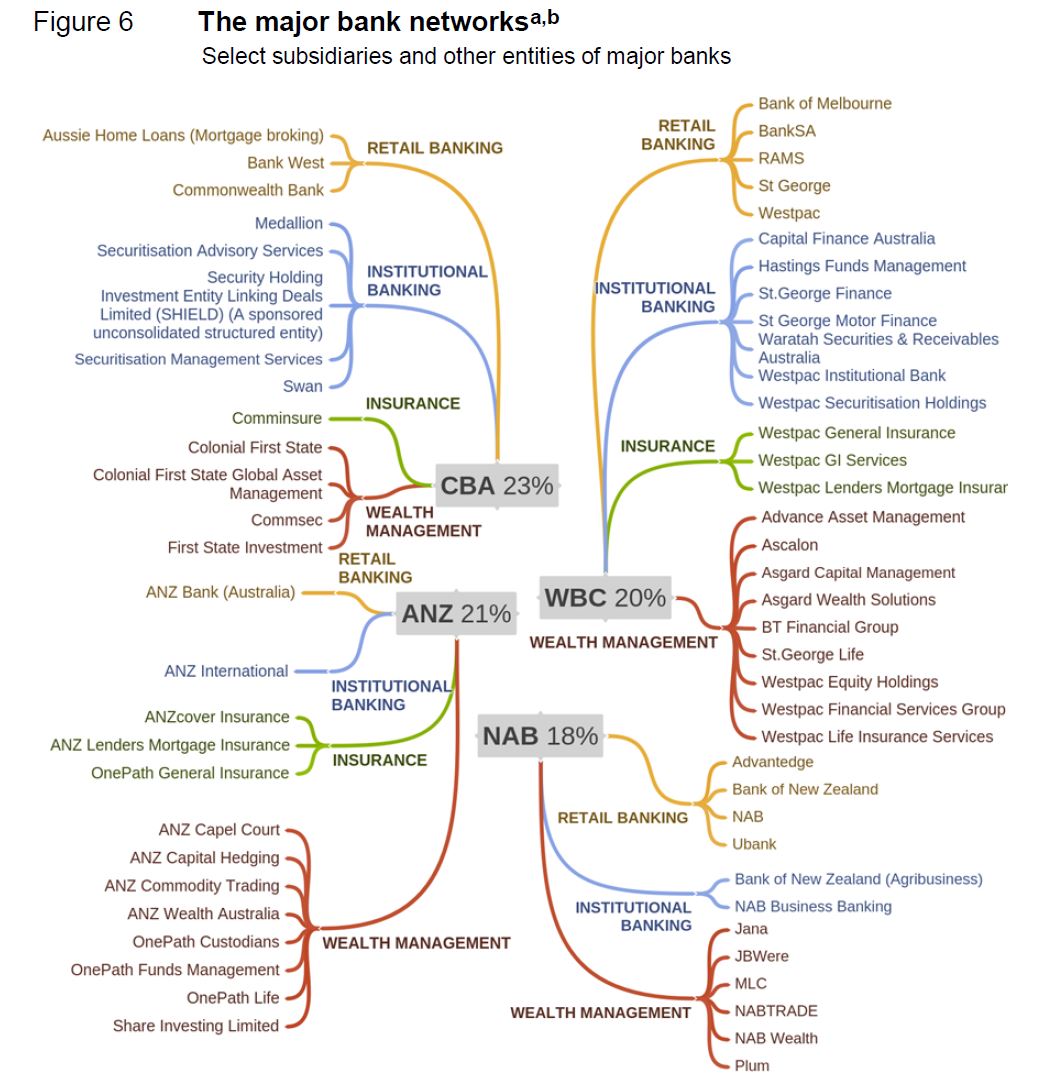

The ACCC’s Financial Services Unit is now well established and will, post 1 July, proactively identify and investigate competition issues in the sector.

“Importantly, the ACCC is due to release its interim report into residential mortgage pricing shortly. As directed by the Treasurer, a key focus will be on transparency, particularly how the major banks balance the interests of consumers and shareholders in making their interest rate decisions.”

Mr Sims highlighted 2018 as the first full year the ACCC will have powers covering misuse of market power and concerted practices.

“In response to the Harper Reform legislation, the ACCC has established the Substantial Lessening of Competition (SLC) Unit to focus on investigations that could give rise to cases under the new laws. The SLC Unit also has a broader mandate to enhance our investigation of competition cases and look afresh at the way we handle such investigations. The ACCC fought hard for these provisions and we will be using them,” Mr Sims said.

Mr Sims also stressed the importance of higher penalties under both consumer and competition law. In relation to the Australian Consumer Law (ACL), legislation was introduced last week to raise penalties from $1.1 million for companies to the greater of $10 million, three times the value of the benefit received, or where the benefit cannot be calculated, 10 per cent of annual turnover in the preceding 12 months.

“Currently, the maximum penalties for breaches of the ACL are, for corporations, approximately one-tenth of the lowest maximum penalty for breaches of the Competition Law. There is no good reason for this difference as we have seen cases where consumer law breaches have led to very substantial harm to many consumers.”

In relation to competition penalties, the ACCC is also anticipating the launch of an OECD report at the end of March will shine a light on Australia’s approach to antitrust sanctions in comparison with other developed competition law jurisdictions.

“Put simply, we believe large businesses should bear penalties which are commensurate to their size, in order to achieve specific and general deterrence. Making this happen is a huge priority and challenge for the ACCC in 2018.”

Most keenly anticipated, perhaps, is the ACCC’s inquiry into digital platforms.

“Concerns about the influence of digital platforms have become prominent in recent years, on many fronts, and this inquiry will be the first of its kind to explore broadly the competition and consumer implications,” Mr Sims said.

“A key question will be how much consumers know about the amount and use of the data about them that is collected and sold by the digital platforms in the form of advertising.”