I discuss a Nucleus Wealth article authored by Tim Fuller, Head of Advice at Nucleus.

The allure of having complete control over your financial future is very compelling, and becomes even more so in turbulent market periods, like the one we have seen in 2020. So it is understandable that 2020’s volatile markets combined with the opaqueness of many large super funds could have left you wondering if you should be opening your own self managed super fund (SMSF).

CBA has decided to remove SMSF lending from its services. Commonwealth Bank of Australia (CBA) has said it is “streamlining” its product offering and as such will no longer offer the ability for self-managed super fund (SMSF) trusts purchase investment property with their fund. Via Australian Broker.

In July, Westpac announced it would be removing its SMSF product. CBA also announced it would be removing low-doc loan products.

CBA’s SuperGear product currently available will cease at close of business on 12 October. New applications and refinancing applications will not be accepted after this date.

Any approvals before 12 October have the condition they must be settled and approved by 28 December 2018.

A CBA spokesperson said in a statement, “As part of our strategy to become a simpler, better bank, we are streamlining our product portfolio and have made the decision to discontinue our ‘SuperGear’ lending product which enabled investment in residential and commercial property through self-managed super funds.

“This change will be effective from close of business on 12 October 2018. We will continue to support our existing customers who have these loans with us.”

For brokers, commission payments will continue as per existing agreements.

Over the past week, four separate lenders have announced their exit from the SMSF lending space, with a further two banks saying loans will no longer be offered to SMSFs.

Westpac announced that effective 31 July 2018 it would no longer offer property loans to SMSFs for both residential and commercial properties.

This followed an earlier announcement from its subsidiary St.George that it will withdraw its SMSF loan products from sale effective 31 July 2018.

Westpac Group confirmed to InvestorDaily sister title Mortgage Business that the removal of SMSF loans for both residential and business properties will be applied across all of the brands in the Westpac Group, including Bank of Melbourne and BankSA.

Commenting on the decision to withdraw all its brands from the SMSF lending space, Westpac stated that the bank “continually reviews its products to ensure we meet the expectations and requirements of customers”.

“To streamline our product offering, effective Tuesday, 31 July 2018 applications for new consumer or business lending will no longer be accepted for SMSFs,” Westpac stated in a public release.

The borrowing market has been getting tougher for SMSF trustees for several months, especially with loan to value expectations, as foreshadowed by specialist brokers like Thrive Investment Finance’s owner Samantha Bright last year.

Most recently, Ms Bright said off-the-plan purchases are becoming increasingly difficult to finance, with lenders either refusing applications for properties that are less than six months old or requiring stronger assets than normal to back their loans.

Many Self Managed Super Funds (SMSF) trustees may not have received “best interest” advice with regards to their fund. This despite the considerable growth in the SMSF sector, which is driven, according to our research, by holders wanting to avoid retail fund fees, and greater control of their finances.

ASIC has released Report 575 SMSFs: Improving the quality of advice and member experiences and Report 576 Member experiences with self-managed superannuation funds.

ASIC reviewed 250 client files randomly selected based on Australian Taxation Office (ATO) data and assessed compliance with the Corporations Act’s ‘best interests’ duty and related obligations.

In 91% of files reviewed the adviser did not comply with Corporations Act’s ‘best interests’ duty and related obligations. The non-compliant advice ranged from record-keeping and process failures to failures likely to result in significant financial detriment. This included:

In 10% of files reviewed, the client was likely to be significantly worse off in retirement due to the advice;

In 19% of cases, clients were at an increased risk of financial detriment due to a lack of diversification.

ASIC Deputy Chair Peter Kell said the standard of advice on SMSFs must improve. ‘A healthy and robust SMSF sector is an important part of our super system. However, it is clear lots of people are setting up self-managed super funds without knowing whether this is the best option. The financial advice sector has significant work to do to lift their performance on this issue.’

ASIC will be taking follow up regulatory action, in particular where consumers have suffered detriment.

ASIC also conducted market research which included interviews with 28 consumers who had set up an SMSF and an online survey of 457 consumers who had set up an SMSF. Through this work we found a lot of people do not understand fully the risks of SMSFs, or their legal obligations as trustees.

In the online survey:

38% of respondents found running an SMSF more time consuming than expected;

32% found it to more expensive than expected;

33% did not know the law required an SMSF to have an investment strategy; and

29% mistakenly believed that SMSFs had the same level of protection as prudentially regulated superannuation funds in the event of fraud.

Mr Kell said, ‘Decisions about super are some of the most important a person can make. However, ASIC found there is a lack of basic knowledge of the legal obligations in setting up or running an SMSF. It is also concerning many people with an SMSF have not understood the importance of diversification, which puts their financial future at risk.’

ASIC also found some people had moved to SMSFs as a way to get into the property market, and were using it solely for this purpose without a wider investment strategy.

The interviews also identified a growing use of ‘one-stop-shops’ where the adviser has a relationship with a developer or a real estate agent whose products the person is encouraged to invest in. This put people at increased risk of getting poor advice that did not take account of their personal circumstances or is not given in their best interests.

ASIC’s findings are supported by the recent Productivity Commission super report which found smaller SMSFs (with balances under $1 million) delivered on average returns below larger funds, and that the costs for low-balance SMSFs are higher than for funds regulated by the Australian Prudential Regulation Authority (APRA).

ASIC’s SMSF report will inform its surveillance and regulatory work into the SMSF sector. ASIC will take enforcement action as appropriate, including ensuring licensees with non-compliant advisers undertake client review and remediation.

More broadly, ASIC and the ATO will have an increased focus on property one-stop-shops. This will include sharing data and intelligence, and ASIC taking enforcement action where it sees unscrupulous behaviour.

NAB says that appetite for equity investing among Australian Self-Managed Super Fund (SMSF) investors surged in 2017, with international shares, domestic exchange traded funds, mFunds and partially paid shares the top new investment picks for investors.

The nabtrade data, which looked at the equity trading patterns of SMSFs in the 12 months to 15 December, showed this group of investors had almost tripled their investment in mFunds, and raised their holdings in ETFs and partially paid shares by 55 per cent and 51 per cent respectively.

Preference shares were equally popular with SMSF investors, with holdings up 34 per cent. Traditional equity holdings were also solid, up 13.5 per cent, while SMSFs retreated from investing in floating rate notes and options over the same period.

NAB Director of SMSF and Customer Behaviour, Gemma Dale, said SMSF investors were overall very active in equity markets in 2017, with total portfolios up more than 15 per cent on the previous year.

“The analysis shows that investors are getting comfortable with the more exotic equity instruments in the market and are prepared to spread risk. Low levels of volatility and the strong performance of domestic and international markets gave investors’ confidence to look for new opportunities,’’ Ms Dale said.

“As with previous years, financials and materials were the most heavily traded sectors, accounting for 36 per cent and 17 per cent of the turnover in 2017. NAB, Commonwealth Bank and Telstra were the most traded stocks in 2017.

“Telecommunication services, healthcare and consumer discretionary stocks were also popular among investors.”

The data also showed SMSF investors are also getting more confident in international equity investing and prepared to take bets on new and innovative sectors such as robotics and aerospace using ETFs.

“International trading surged nearly 100 per cent over the previous year, with US equities and US ETF’s the most traded equity instruments on international markets throughout the year,’’ Ms Dale said.

‘’Like retail investors, SMSF investors are turning to offshore markets to diversify their portfolios and to access high growth sectors in the US.’’

Most popular equity investments by SMSF Investors in 2017 Top Ten Domestic Equity instruments in 2017

NATIONAL AUSTRALIA BANK. Ordinary Fully Paid

COMMONWEALTH BANK OF AUSTRALIA. Ordinary Fully Paid

WESTPAC BANKING CORPORATION. Ordinary Fully Paid

AUSTRALIA AND NEW ZEALAND BANKING GROUP. Ordinary Fully Paid

TELSTRA CORPORATION. Ordinary Fully Paid

BHP BILLITON. Ordinary Fully Paid

WESFARMERS. Ordinary Fully Paid

CSL. Ordinary Fully Paid

WOOLWORTHS GROUP. Ordinary Fully Paid

WOODSIDE PETROLEUM. Ordinary Fully Paid

Source: nabtrade

Top Ten International Equity instruments in 2017

AMAZON COM ORD Common Stock

APPLE ORD Common Stock

FACEBOOK CL A ORD Common Stock

ALIBABA GROUP HOLDING ADR REP 1 ORD Depositary Receipt

ENPHASE ENERGY ORD Common Stock

TENCENT ORD Common Stock

TESLA ORD Common Stock

NVIDIA ORD Common Stock

MICROSOFT ORD Common Stock

BANK OF AMERICA ORD Common Stock

Source: nabtrade

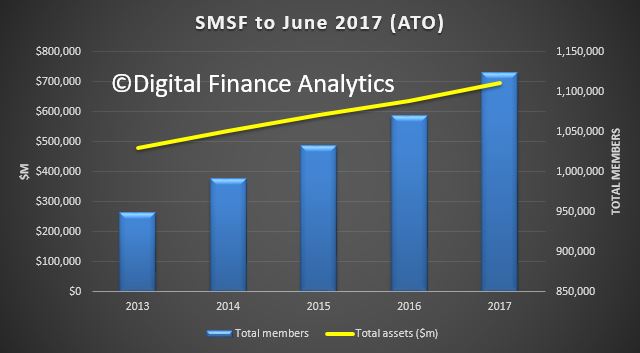

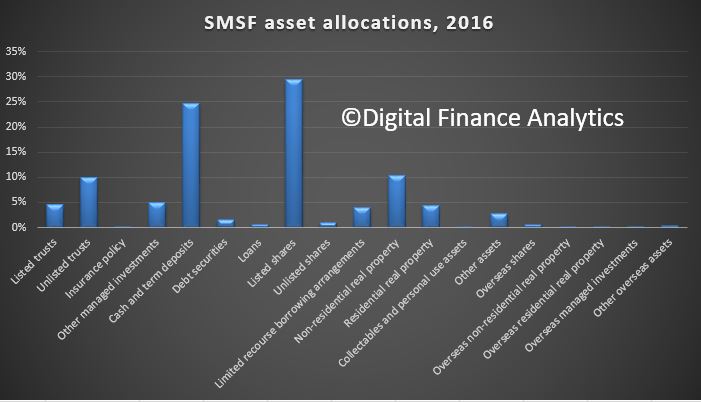

The ATO published the latest data on Self-managed superannuation funds to 2016. The number and balance of funds continues to grow and contributions are growing faster than to retail or industry funds. More property is held and under limited recourse borrowing arrangement.

In 2015–16, estimated average return on assets for SMSFs was positive (2.9%), a decrease from the estimated returns in 2014–15 (6.0%). This was the same as the investment performance for APRA funds of more than four members (2.9%) and remains consistent with the trend for APRA funds over the five years to 2016.

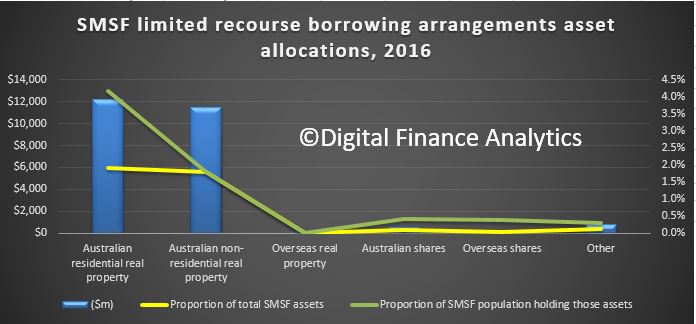

We also see a rise in property investment within SMSFs, with 7% of SMSFs reported $25.4 billion assets held under limited recourse borrowing arrangement (LRBAs), which is slightly higher than in 2015 (6%). The majority of these funds held LRBA investments in residential real property and non-residential real property.

The estimated average total expense ratio of SMSFs in 2016 was 1.21% and the average total expenses value was $13,700. This would be lower than the typical costs in a retail fund.

SMSF’s make up 30% of all superannuation assets which in total are worth $2.3 billion. There were 597,000 SMSFs holding $697 billion in assets, with more than 1.1 million SMSF members as at 30 June 2017. Over the five years to 30 June 2017, growth in the number of SMSFs averaged almost 5% annually.

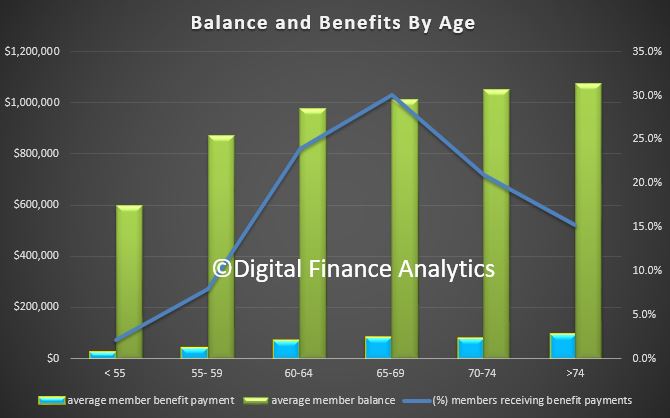

At 30 June 2016 the average SMSF member balance was $599,000 and the median balance was $362,000, an increase of 26% and 32% respectively over the five years to 2016.

The average member balances for female and male members were $511,000 and $641,000 respectively. The female average member balance increased by 30% over the five-year period, while the male average member balance increased by 22% over the same period.

Over the five years to 2016, the proportion of members with balances of $200,000 or less decreased from 42% to 32% of all members.

In 2016, the majority of members had balances of between $200,001 and $1 million.

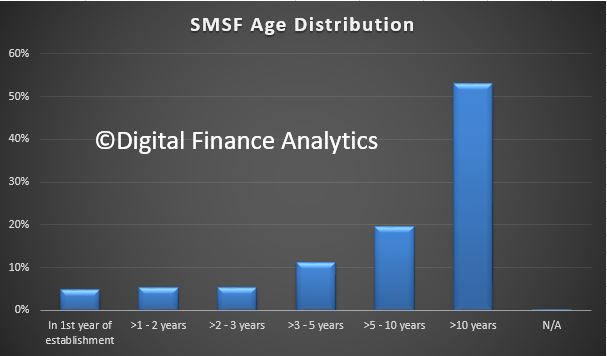

53% of SMSFs have been established for more than 10 years, and 16% have been established for three years or less.

For the 2015–16 income year, the average assets of SMSFs were just over $1.1 million, a growth of 25% over five years and 3% from 2015. Total contributions to SMSFs increased by 21% over the five years to 2016. This is significantly higher than the growth of total contributions to all superannuation funds (16%) over the same period. The majority of SMSFs continued to be solely in the accumulation phase (53%) with the remaining 47% making pension payments to some of or all members.

At 30 June 2017, 57% of all SMSFs had a corporate trustee rather than individual trustees.

Of newly registered SMSFs in 2015 to 2017, on average 81% were established with a corporate trustee.

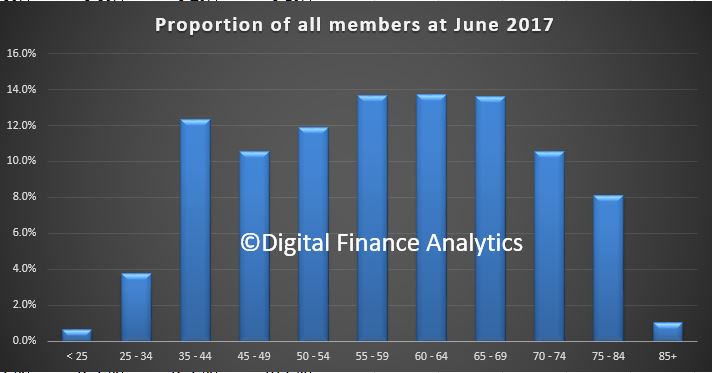

At 30 June 2017 there were 1.1 million SMSF members, of whom 53% were male and 47% female.

The trend continued for members of new SMSFs to be from younger age groups. The median age of SMSF members of newly established funds in 2016 was 47 years, compared to 59 years for all SMSF members as at 30 June 2017.

SMSFs directly invested 80% of their assets, mainly in cash and term deposits and Australian-listed shares (a total of 54%).

In the five years to 2016, cash and term deposits decreased (by 7%) to 25% of total SMSF assets.

In 2016, 7% of SMSFs reported $25.4 billion assets held under Limited recourse borrowing arrangement (LRBAs), which is slightly higher than in 2015 (6%). The majority of these funds held LRBA investments in residential real property and non-residential real property. In terms of value, real property assets held under LRBAs collectively made up 93% or $23.7 billion of all SMSF LRBA asset holdings in 2016.

The estimated average total expense ratio of SMSFs in 2016 was 1.21% and the average total expenses value was $13,700.

The average ‘investment expense’ and ‘administration and operating expense’ ratios were consistent at 0.65% and 0.56% respectively.

SMSF and accounting professionals alike are increasingly finding that clients are willing to take risky moves with their property portfolios, in an effort to reduce their mortgage stress. From SMSF Adviser.

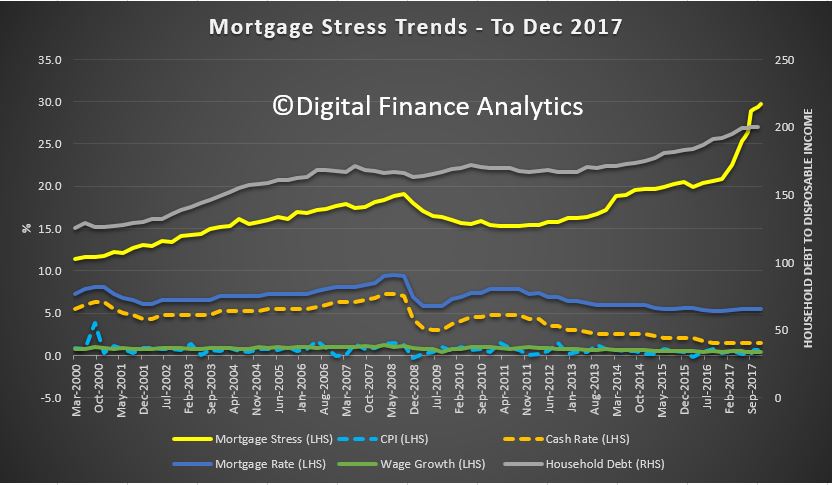

These patterns are surfacing as instances of mortgage stress continue to climb significantly in Australian households. Research house Digital Finance Analytics (DFA) has released its mortgage stress and default analysis for December 2017, showing about 29.7 per cent of households — 921,000 — are under “mortgage stress.”

About 24,000 households are under “severe mortgage stress”, up by 3,000 from November 2017.

DFA principal Martin North believes the risk of default for Australians has increased for 2018, with an estimated 54,000 households currently at risk of 30-day debt defaults in the next 12 months.

Several accountants and financial advisers have told Accountants Daily that their clients, including high-net-worth property investors, are increasingly looking to take on more risk to sustain their levels of debt.

Director at Verante Financial Planning, and chair of the SMSF Association’s NSW state chapter, Liam Shorte, said he’s seen evidence of investors asking accountants to increase their reportable income to increase their borrowing capacity, usually where they need to refinance. Historically, clients have sought advice on how to minimise their reportable income for tax purposes.

He also told sister publication Accountants Daily that more clients are asking their parents to do a “family pledge,” or guarantee about 20 per cent of a loan to help reduce debt while refinancing.

For Lielette Calleja, director at bookkeeping firm All That Counts, mortgage stress is most pronounced with small business owners, and doesn’t necessarily only affect those at the lower end of the earning scale.

“I would have to say that small business owners are heavily affected. Your income is not always consistent, as opposed to being a PAYG. Mortgage stress is across the board I don’t believe it discriminates as it’s relative to each type of borrower. Property investors and high-net-worth individuals tend to be asset rich but lack cash flow until their development is complete and/or sold/leased out,” Ms Calleja told Accountants Daily.

Further, Ms Calleja is finding clients are modifying their behaviours and expenses to adjust to a new normal in household debt levels.

“Families that are not in a position to refinance are resorting to taking their kids out of private schools and foregoing luxury holidays, even simple things like making your own lunch instead of buying is becoming the Aussie way,” she said.

“Small business owners are coming to the conclusion that having good financials consistently all year round is critical in keeping their mortgage stress levels at bay,” she added.

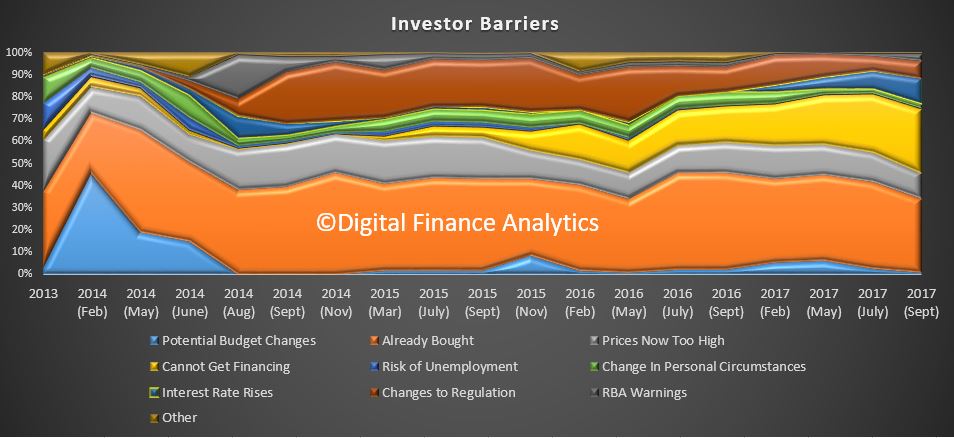

Continuing our series on our latest household survey results, we look more deeply at the attitude of property investors, who over the past few years have been driving the market. We already showed they are now less likely to transact, but now we can look at why this is the case.

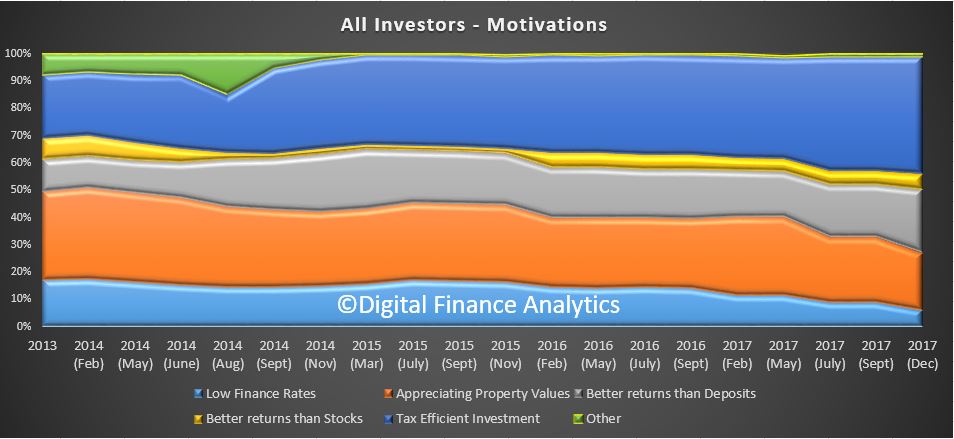

Looking at investors (and portfolio investors) as a group, we see the prime attraction is the tax effectiveness of the investment (negative gearing and capital gains tax) at 43% (which has been rising in recent times). But availability of low finance rates and appreciating capital values have both fallen this time around. They are still driven by better returns than deposits (23%) but returns from stocks currently look better, so only 6% say returns from investment property are better than stocks! Only tax breaks are keeping the sector afloat.

We can also look at the barriers to investing. One third of property investors now report that they are unable to obtain funding for further property transactions, nearly double this time last year.

Then 32% say they have already bought, and are not in the market at the moment. Whilst concerns about more rate rises have dissipated a little, factors such as prices being too high, potential changes to regulation and RBA warnings all registered.

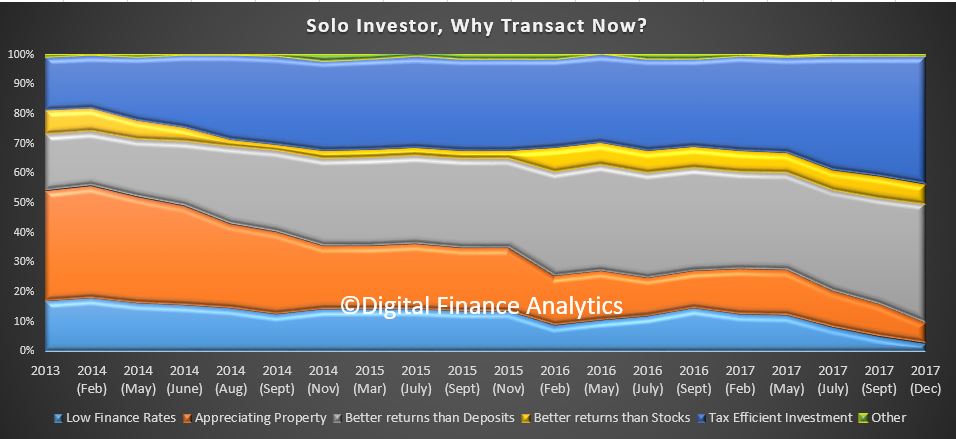

Turning to solo property investors (who own just one or two investment properties), 43% report the prime motivation is tax efficiency, 40% better returns than bank deposits and better returns than stocks (7%). But the accessibility of low finance rates and appreciating property prices have fallen away.

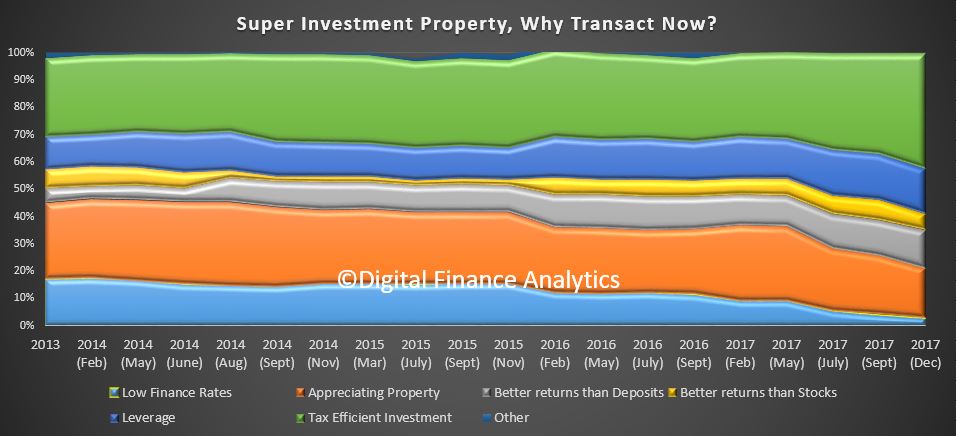

Those investing via SMSF also exhibit similar trends with tax efficiency at 43%, leverage at 16%, and better returns than deposits 14%. Once again, cheap finance and appreciating property values have diminished in significance.

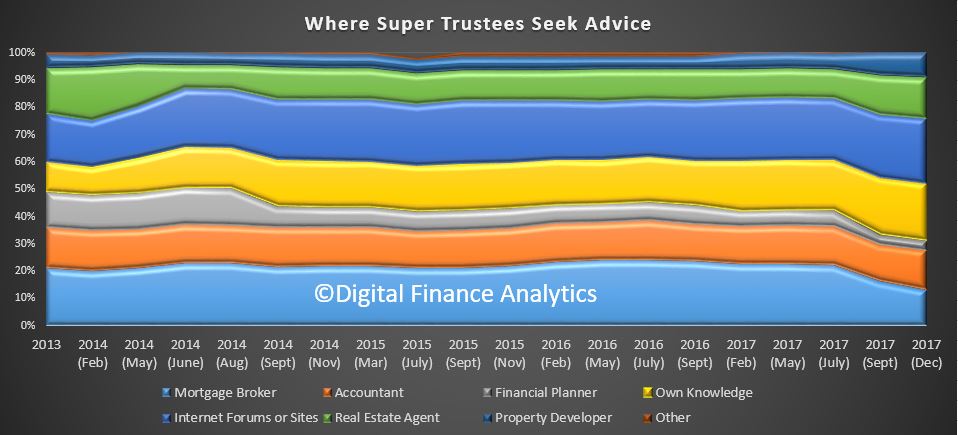

We also see 23% of SMSF trustees get their investment advice from internet or social media sites, 21% use their own knowledge, while 13% look to a mortgage broker, 14% an accountant and 4% a financial planner. 15% will consult with a real estate agent and 9% with a property developer.

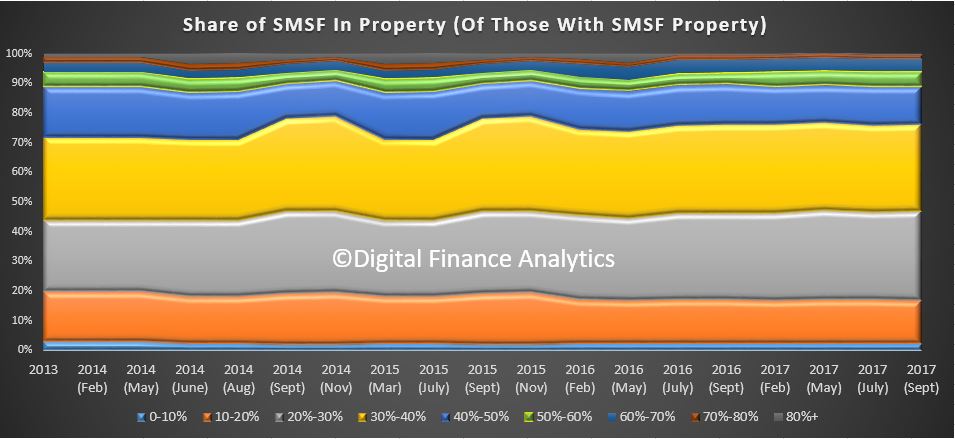

There is a fair spread of portfolio distribution into property. 13% have between 40-50% of SMSF investments in property, 29% 30-40% and 30% 20-30% of their portfolios.

Next time we will look at first time buyers and other owner occupied purchasers. Some are taking up the slack from investors, but is that sufficient to keep the market afloat?

American wealth management giant Charles Schwab Corporation has re-opened an office in Sydney after exiting the Australian market in 2000.

The San Francisco-headquartered financial advice firm, custodian and brokerage has “re-established” its presence in Australia following the acquisition of Chicago-based “broker-dealer” optionsXpress.

Charles Schwab Australia managing director JP Drysdale told InvestorDaily the decision to re-enter the Australian market was due to growth of SMSFs in Australia that exhibited the “clear demand for self-directed investment opportunities”.

“The acquisition and integration of the optionsXpress business presented opportunities in both the Australian and Singapore markets,” Mr Drysdale said.

“The time was right to enter both, to give investors in both markets the ability to trade in US markets through a platform that’s cost effective, secure and time-tested.”

Prior to 2000, Charles Schwab had an Australian presence but decided to physically exit the market due to a “range of market circumstances at that time”.

Where optionsXpress only offered an online trading platform, Charles Schwab had the capacity to cater to the needs of Australian investors more broadly, Mr Drysdale said.

“Globally, Charles Schwab is a wealth management and advisory firm that focuses on helping clients invest for their future,” Mr Drysdale told InvestorDaily.

“This is a far broader approach to customers investing needs than optionsXpress.

“Charles Schwab Australia is now in a position to assist many more Australians who need to manage they investments and diversify in the US, but don’t see themselves as short-term traders.”

Through its electronic trading platform, the broker firm will offer Australian investors access to US-listed equities, offshore mutual funds, ETFs, fixed income, options and futures at US$4.95 per online equity trade.

He added that local investors, through a variety of channels, were now able to have cost effective access to the US market.

“Typically, access to US markets for self-directed investors, including SMSFs, is expensive compared to the costs of transacting in the Australian market,” he said.

“However, we believe there need not be trade-offs between price and customer service.

“From the high-quality research content mentioned above to the ability for clients to pick up the phone and talk to a financial consultant, Charles Schwab provides many ways for clients to access investment experts.

“We see our role as working with clients to help them develop a strategy for increasing the diversity of their investments and therefore managing the risk in their portfolios.”

The Turnbull government has taken planned restrictions to borrowing by self-managed superannuation funds off the agenda in the short-term in a move that may presage a weakening of the proposals.

Under a plan announced in April, debt on the books of SMSFs would be added to fund values when calculating the new $1.6 million limits for tax-free super pensions.

The move was designed to stop people effectively getting around the cap by using borrowings to reduce asset values and paying the debts off over time.

The initial consultation period for the move expired on May 3 but the government has opened discussions again with the superannuation industry.

A spokesperson for acting Financial Services and Revenue Minister Mathias Cormann said: “Following stakeholder feedback, the government will consult further with stakeholders on the proposal to add the outstanding balance of a limited recourse borrowing arrangement (LRBA) to a member’s total superannuation balance measure in conjunction with consultation on the non-arm’s length income integrity measure announced in the 2017-18 budget.”

The SMSF industry has kicked back on the moves, saying they may force some investors to sell properties because they won’t be able to make extra non-concessional contributions to their fund needed for debt repayments once it has hit the $1.6 million limit.

“Some self-managed funds may not be able to use limited recourse borrowing arrangements if they will be relying on non-concessional contributions to repay some or all of the loan interest and capital because the gross value of the asset(s) will take them over the $1.6 million total superannuation balance and they will be unable to make further non-concessional contributions to service the debt,” the SMSF owners alliance said in a submission on the issue to Treasury.

The opposition has not expressed a view on the legislation, saying instead it would like to ban SMSF’s borrowing altogether.

“Labor has previously stated that we will restore the general ban on direct borrowing by superannuation funds, as recommended by the 2014 Financial Systems Inquiry, to help cool an overheated housing market partly driven by wealthy Self-Managed Super Funds,” a spokesman for Labor’s shadow Financial Services Minister Katy Gallagher said in response to questions from The New Daily.

“This has seen an explosion in borrowing from $2.5 billion in 2012 to more than $24 billion today.”

Stephen Anthony, chief economist for Industry Super Australia, said there was an argument for leaving out existing arrangements from the changes.

“I’d be happy to see transition arrangements put in place and allowing the restrictions to apply to arrangements from here on in,” he said.

“But if the outcome of the consultation is just to water down what I see as a useful structural reform, I’d be very disappointed.”

The industry fears that introducing the new restrictions to existing arrangements would mean some SMSF owners would be forced to sell properties held in their funds because they would not be able to make loan repayments.

The explosion of SMSF property debt has been a concern for regulators, with the Murray inquiry into the financial system in 2014 recommending SMSF borrowing be banned, warning “further growth in superannuation funds’ direct borrowing would, over time, increase risk in the financial system”.

Blog")