Last October we wrote a series of posts on the risks related to interest only loans. Given recent developments, and the belated focus from APRA and ASIC, we revisit the topic today.

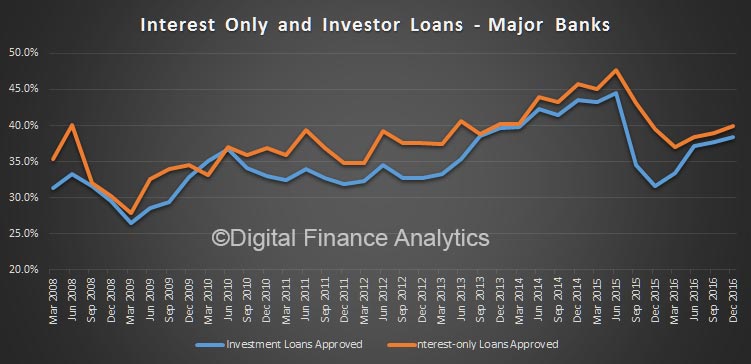

Here is a plot from the APRA data showing the relative movement of investor loans and interest only loans. Yes, there is a correlation! The ABC’s Phil Lasker used this chart in the TV News on Friday.

Lenders will need to throttle back new interest only loans. But this raises an important question. What happens when existing IO loans are refinanced?

Lenders will need to throttle back new interest only loans. But this raises an important question. What happens when existing IO loans are refinanced?

Less than half of current borrowers have complete plans as to how to repay the principle amount.

Interest-only loans may seem like a convenient way to reduce monthly repayments, (and keep the interest charges as high as possible as a tax hedge), but at some time the chickens have to come home to roost, and the capital amount will need to be repaid.

Many loans are set on an interest-only basis for a set 5 year term, at which point the lender is required to reassess the loan and to determine whether it should be rolled on the same basis. Indeed the recent APRA guidelines contained some explicit guidance:

For interest-only loans, APRA expects ADIs to assess the ability of the borrower to meet future repayments on a principal and interest basis for the specific term over which the principal and interest repayments apply, excluding the interest-only period

This is important because the number of interest-only loans is rising again. Here is APRA data showing that about one quarter of all loans on the books of the banks are interest-only, and that recently, after a fall, the number of new interest-only loans is on the rise – around 35% – from a peak of 40% in mid 2015. There is a strong correlation between interest-only and investment mortgages, so they tend to grow together. Worth reading the recent ASIC commentary on broker originated interest-only loans.

But what is happening at the coal face? To find out we included some specific questions in our household survey, and today we present the results.

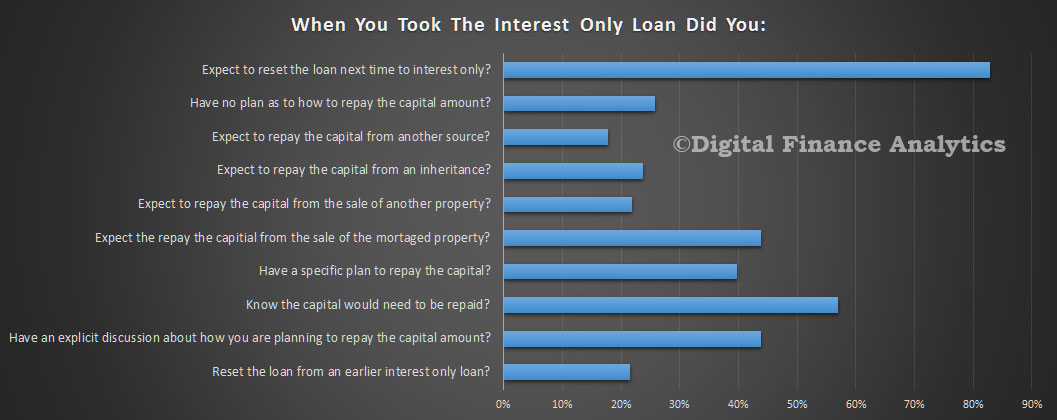

We were surprised to find that around 83% of existing interest-only loan holders expect to roll their loan to another interest-only loan, and to keep doing so. More concerning, only around 44% of borrowing households had an explicit discussion with the lender (or broker) at their last loan draw down or reset about how they plan to repay the capital amount outstanding. Some of these loans are a few years old.

Around 57% said they knew the capital would have to be repaid (we assume the rest were just expecting to roll the loan again) and 26% had no firm plans as to how to repay whereas 39% had an explicit plan to repay.

Around 57% said they knew the capital would have to be repaid (we assume the rest were just expecting to roll the loan again) and 26% had no firm plans as to how to repay whereas 39% had an explicit plan to repay.

Many were expecting to close the loan out from the sale of the property (thanks to capital appreciation) at some point, from the sale of another property, or from another source, including an inheritance.

Thus we conclude there is a potential trap waiting for those with interest-only loans. They need a clear plan to repay, at some point. It also highlights that the quality of the conversation between borrower and lender is not up to scratch.

We think some borrowers on an interest-only loan may get a rude shock, when next they try to roll their interest-only loan. If they do not have a clear repayment plan, they may not get a new loan. There is a debt trap laid for the unwary and the APRA guidelines have made this more likely.

Back in 2014, we wrote about the interest only situation in the UK.

So, now lets look at the UK experience. There are 11.3 million mortgages in the UK, with loans worth over £1.2 trillion. At the end of 2013 there were an estimated 2.2 million pure interest-only loans outstanding, and a further 620,000 part interest-only, part repayment mortgages outstanding on lenders’ books. Compared to 2012 this represents a fall of around 300,000 pure interest-only mortgages (down 12%), and around 90,000 part-and-part mortgages (down 13%).

According to the Council for Mortgage Lenders, at the peak of their popularity in the late 1980s, interest-only mortgages accounted for more than 80% of all loans taken out. This year, however, lenders are likely to advance only around 40,000 new interest-only loans for residential house purchase, less than 10% of the total.

Among first-time buyers, the decline in interest-only borrowing has been particularly pronounced. CML data shows that only 2% are taking out interest-only mortgages, with 98% opting for repayment loans. Interest-only accounts for a higher proportion of new borrowing by existing owner-occupiers who are moving (10%) and those remortgaging (13%).

Most new interest-only borrowing is in the buy-to-let market (aka investment mortgage), where this option remains the norm for very good reasons. Fixed-rate interest-only mortgages minimise costs for landlords and are more likely to produce a profitable margin. Interest-only mortgages also enable landlords to meet lenders’ requirements that their rental income produces an average minimum cover of 125% of their borrowing costs.

A couple of years back, there were concerns in the UK that interest only loans may be a problem, and alongside regulatory commentary, CML produced an “interest-only toolkit” designed to help mortgage lenders to work with their interest only mortgage customers, especially those loans due for repayment before 2020.

The regulators reached the conclusion that 90% of interest-only mortgage holders have a repayment strategy in place. Lenders made a commitment with the regulator (the Financial Conduct Authority) to contact interest-only loan holders and ask about their repayment plans. The CML via it lender members found that Lenders have been using a variety of contact strategies. In addition to reminders and mailings requesting the customer’s written response (including questionnaire responses), telephone calls, face-to-face meetings and even home visits are also used by some lenders. Overall, around 30% of customers contacted have so far responded.

Among those borrowers who have responded, around four out of five already had a clear plan. Among those who did not, the survey found that the solutions and approaches lenders are offering typically include term extensions, permanent conversions to capital and interest, and overpayments.

There has also been a positive set of changes in the loan-to-value profile of outstanding interest-only mortgages. Two-thirds of outstanding interest-only mortgages have loan-to-value (LTV) ratios of less than 75% – and the vast majority of these are not due to mature until after 2020.

The chart shows that a large number of loans would have moved into a lower LTV band as a result of house price inflation alone. However, it also shows that borrowers are taking additional action to reduce their mortgage balances, as the effect of house price inflation alone would not have resulted in the improvements in outstanding LTVs that have been seen over the past year. Indeed, the number of loans in every LTV band below 75% would have seen an increase on the basis of house price inflation alone (as loans moved down from higher LTV bands) – but, in fact, every band saw a decrease.

Changes in interest-only loans outstanding, September 2012-December 2013, by LTV

Under the new mortgage regulations now in force in the UK, lenders may offer interest only loans, but only if a borrower has a credible repayment plan, at the time of application.

So some points to ponder.

1. How many interest only loans in Australia have a credible repayment strategy? To what extent is this considered by borrowers and lenders at the time of application?

2. Will rising house prices be the solution to interest-only loan repayment?

3. Are the review processes (on average each 5 years in Australia, even if the loan term is 25/30 years) sufficiently robust to identify potential issues?

4. Does Negative Gearing lead to a greater dependence on interest-only loans?

One thought on “The Interest-Only Loan Debt Trap II”