The CPI data released by the ABS yesterday showed that over inflation remains low.

But within the series there is a striking contrast. The Housing Group category of data rose 0.3 per cent for the quarter, and 2.4 per cent for the year to June 2017 but rent rose only 0.2 per cent for the quarter, and 0.6 per cent for the year.

It is worth reflecting on this in the light of the out of cycle rate hikes which property investors are experiencing, as the banks improve their margins using the alibi of regulatory tightening. In fact recent hikes being applied not to new mortgages but to the entire book have meant a significant “bonus” to the banks.

First, lets be clear rental rates have more to do with income that property prices, and the fact that rental rates have hardly grown reflects the stagnation in wages. Vacancy rates are also rising.

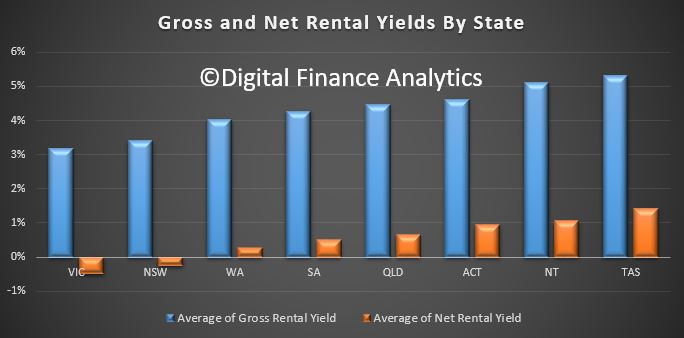

Second, the fact is a greater proportion of property investors are now underwater on a net rental cash flow basis. But the situation varies by state. This chart shows both gross yield (rental income) and net yield, (costs of mortgage repayments and other rental costs) on a cash flow basis and before tax. VIC and NSW have on average negative net returns.

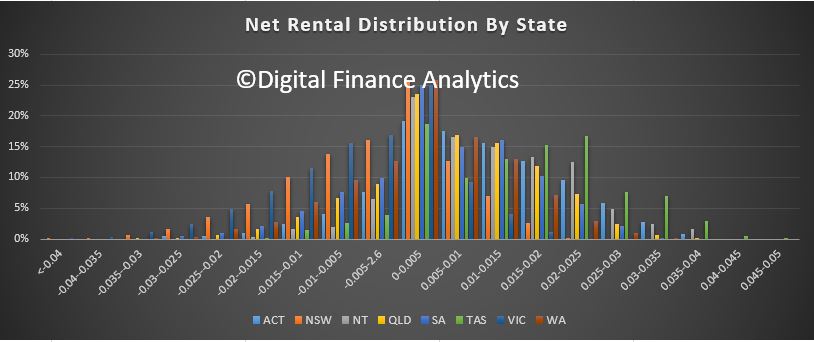

The net rental calculation is before any tax offsets. The distribution by state is even more interesting.

The net rental calculation is before any tax offsets. The distribution by state is even more interesting.

Investors seem ok with negative cash-flow returns because in many cases they just offset the losses against tax, and comfort themselves with the thought that the capital value of the property is still rising (in most eastern states at least).

Investors seem ok with negative cash-flow returns because in many cases they just offset the losses against tax, and comfort themselves with the thought that the capital value of the property is still rising (in most eastern states at least).

However, the divergent movement of mortgage rates and net rental returns are a leading indicator of trouble ahead, especially if capital growth reverses.

Given flat incomes, we think rentals will not grow much at all for some time, and remember more new properties are coming on stream, so vacancy rates are likely to continue to rise!