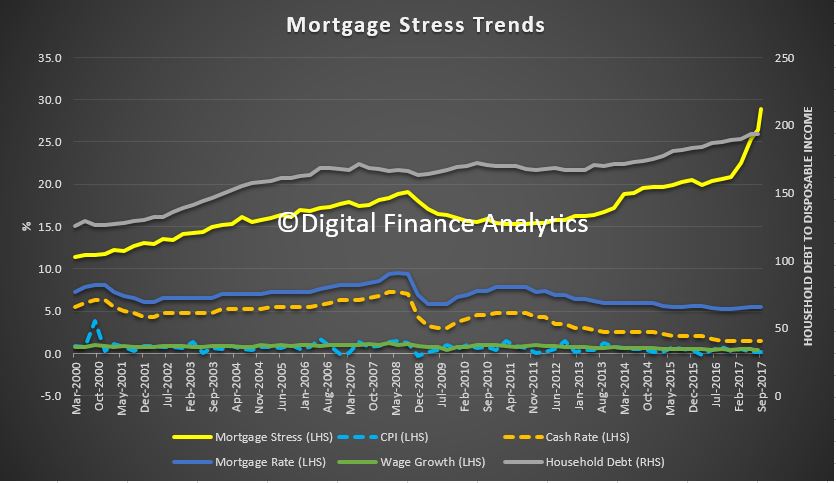

Mortgage stress rose again in September according to Digital Finance Analytics analysis, crossing the 900,000 household rubicon for the first time. The latest RBA data shows household debt to income rose again in June, to 193.7, further confirmation of Australia’s debt problem.

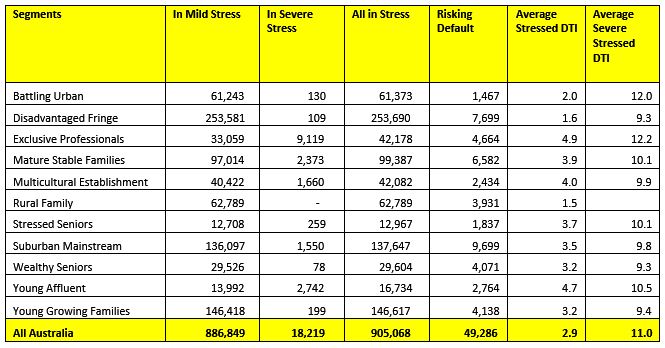

Across the nation, more than 905,000 households are estimated to be now in mortgage stress (last month 860,000) and more than 18,000 of these in severe stress. This equates to 28.9% of households. A rising number of more affluent households are being impacted as the contagion of mortgage stress continues to spread beyond the traditional mortgage belts. We estimate that more than 49,000 households risk default in the next 12 months, up 3,000 from last month.

Across the nation, more than 905,000 households are estimated to be now in mortgage stress (last month 860,000) and more than 18,000 of these in severe stress. This equates to 28.9% of households. A rising number of more affluent households are being impacted as the contagion of mortgage stress continues to spread beyond the traditional mortgage belts. We estimate that more than 49,000 households risk default in the next 12 months, up 3,000 from last month.

Watch the video to learn more, and count down the latest top 10 post codes. We had some new regions “promoted” into the list this time.

The main drivers of stress are rising mortgage rates and living costs whilst real incomes continue to fall and underemployment remains high. Some households are now making larger mortgage repayments following out of cycle interest rate rises, and are simultaneously facing higher power prices, council rates and childcare costs. This remains a deadly combination and is touching households across the country, not just in the mortgage belts.

Our analysis uses the DFA core market model which combines information from our 52,000 household surveys, public data from the RBA, ABS and APRA; and private data from lenders and aggregators. The data is current to end September 2017. We analyse household cash flow based on real incomes, outgoings and mortgage repayments, rather than using an arbitrary 30% of income.

Households are defined as “stressed” when net income (or cashflow) does not cover ongoing costs. Households in mild stress have little leeway in their cash flows, whereas those in severe stress are unable to meet repayments from current income. In both cases, households manage this deficit by cutting back on spending, putting more on credit cards and seeking to refinance, restructure or sell their home. Those in severe stress are more likely to be seeking hardship assistance and are often forced to sell. The debt-to-income (DTI) ratios in severely stressed households are on average eleven times their current annual incomes and this is high on any measure. The combined statistics suggest there are continuing concerns about underwriting standards.

We revised our expectation of potential interest rate rises, given the stronger data on the global economy. Probability of default extends our mortgage stress analysis by overlaying economic indicators such as employment, future wage growth and cpi changes.

Martin North, Principal of Digital Finance Analytics said that “continued pressure from low wage and rising costs means those with bigger mortgages are especially under the gun. These stressed households are less likely to spend at the shops, which will act as a further drag anchor on future growth. The number of households impacted are economically significant, especially as household debt continues to climb to new record levels”. The latest household debt to income ratio is now at a record 193.7.[1]

Gill North, joint Principal of Digital Finance Analytics and a Professorial Research Fellow in the law school at Deakin University, citing her recent research, suggests the Australian house party has been glorious – but the hangover may be severe and more should be done to mitigate future risks and harm to highly indebted households and the nation.[2]

She notes that at the beginning of 2016 the RBA and APRA stood largely aloof from concerns around levels of household debt and the major risk was complacency. While the RBA and APRA have been more vocal since and have taken steps to tighten lending standards, she calls for additional measures and highlights the continuing vulnerability of many households without financial buffers for adverse contingencies.[3]

Regional analysis shows that NSW has 238,703 households in stress (238,755 last month), VIC 243,752 (236,544 last month), QLD 168,051 (146,497 last month) and WA 124,754 (118,860 last month). The probability of default rose, with around 9,300 in WA, around 9,100 QLD, 12,800 in VIC and 13,100 in NSW.

Regional analysis shows that NSW has 238,703 households in stress (238,755 last month), VIC 243,752 (236,544 last month), QLD 168,051 (146,497 last month) and WA 124,754 (118,860 last month). The probability of default rose, with around 9,300 in WA, around 9,100 QLD, 12,800 in VIC and 13,100 in NSW.

You can request our media release. Note this will NOT automatically send you our research updates, for that register here.

[contact-form to=’mnorth@digitalfinanceanalytics.com’ subject=’Request The Sept 2017 Stress Release’][contact-field label=’Name’ type=’name’ required=’1’/][contact-field label=’Email’ type=’email’ required=’1’/][contact-field label=’Email Me The Sept 2017 Media Release’ type=’radio’ required=’1′ options=’Yes Please’/][contact-field label=”Comment If You Like” type=”textarea”/][/contact-form]

Note that the detailed results from our surveys and analysis are made available to our paying clients.

[1] RBA E2 Household Finances – Selected Ratios June 2017

[2] Gill North ‘The Australian House Party Has Been Glorious – But the Hangover May Be Severe: Reforms to Mitigate Some of the Risks’ in R Levy, M O’Brien, S Rice, P Ridge and M Thornton (eds), New Directions For Law In Australia (ANU Press, Canberra, 2017). An earlier version of this book chapter is available at https://ssrn.com/author=905894.

[3] See also, Gill North, ‘Regulation Governing the Provision of Credit Assistance & Financial Advice in Australia: A Consumer’s Perspective’ (2015) 43 Federal Law Review 369. An earlier draft of this article is available at https://ssrn.com/author=905894.