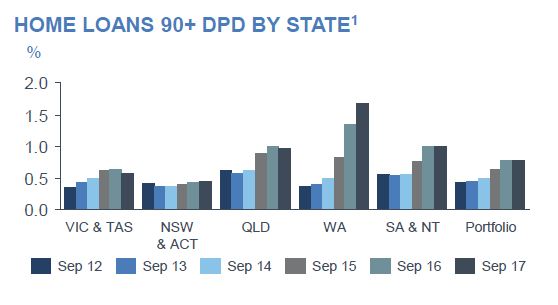

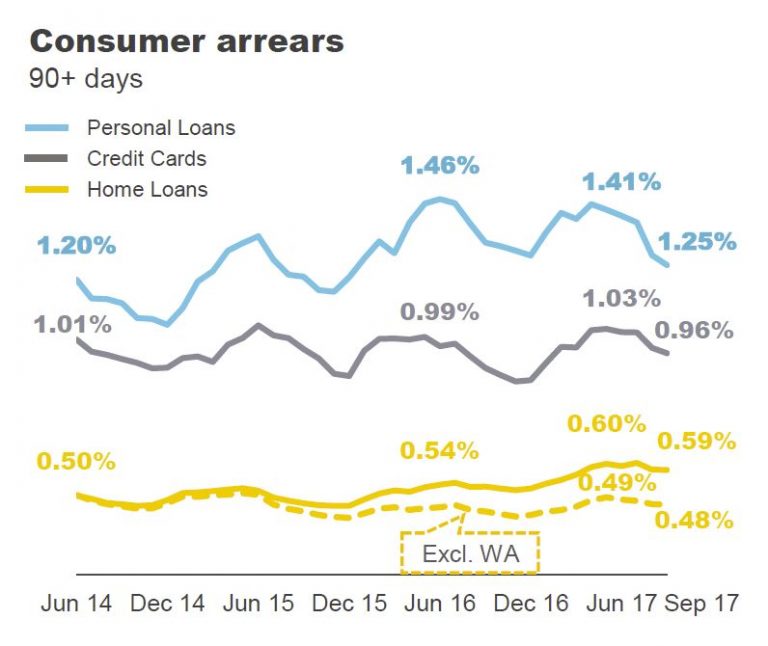

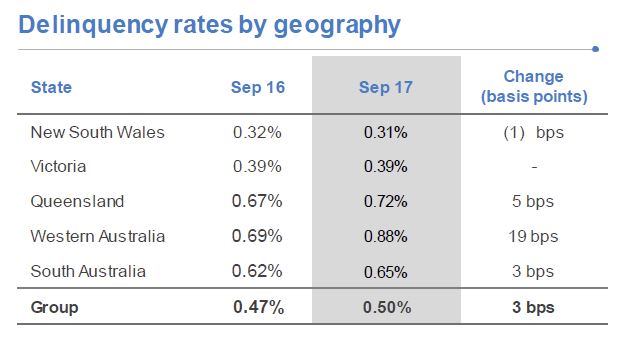

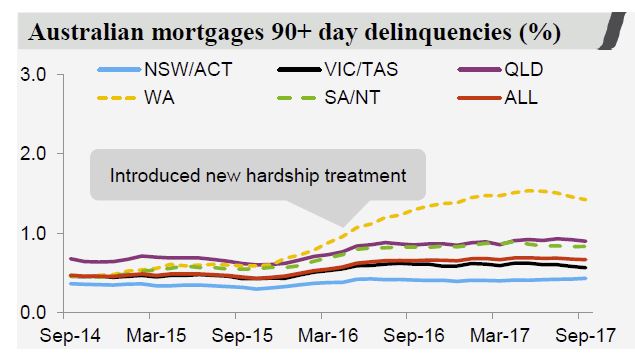

We have now had results in from most of the major players in retail banking this reporting season. One interesting point relates to mortgage defaults. Are they rising, or not?

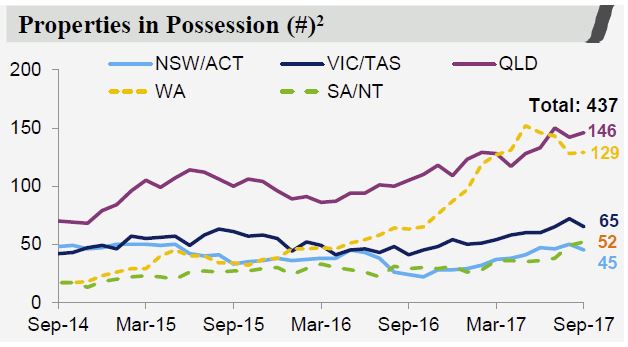

Below are the key charts from the various players. Actually, there are some significant differences. Some are suggesting WA defaults in particular are easing off now, while others are still showing ongoing rises.

This may reflect different reporting periods, or does it highlight differences in underwriting standards? Our modelling suggests that the rate of growth in stress in WA is slowing, but it is rising in NSW and VIC; and there is a 18-24 month lag between mortgage stress and mortgage default. So, in the light of expected flat income growth, continued growth in mortgage lending at 3x income, rising costs of living and the risk of international funding rates rising, we think it is too soon to declare defaults have peaked.

One final point, many households have sufficient capital buffers to repay the bank, thanks to ongoing home price rises. Should prices start to fall significantly, this would change the picture significantly.

One thought on “What Does The Recent Bank Results Tell Us About Mortgage Defaults?”