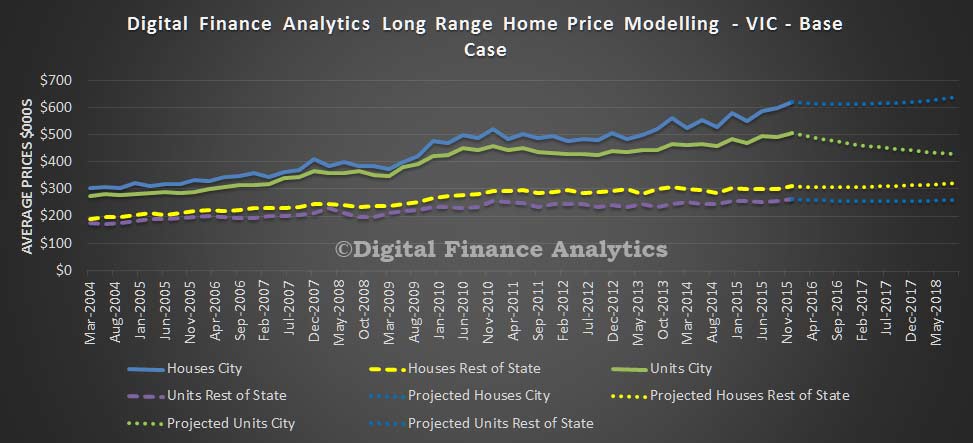

Continuing our econometric modelling of home prices trends, today we examine Melbourne. As we discussed our model takes account of a range of factors and runs a series of future scenarios out to mid 2018. We look at prices both within Melbourne and also across the state and split the analysis into houses and units.

In our base case to mid 2018, we expect to see the average house price in Melbourne rise by 2.8% to $639,000 and the average unit in Melbourne fall by 15.1% to $429,000. In regional areas, the average house price will rise 3.5% to $321,000 and units will fall by 0.4% to $260,000. The oversupply of units in the CBD explain the projected price falls.

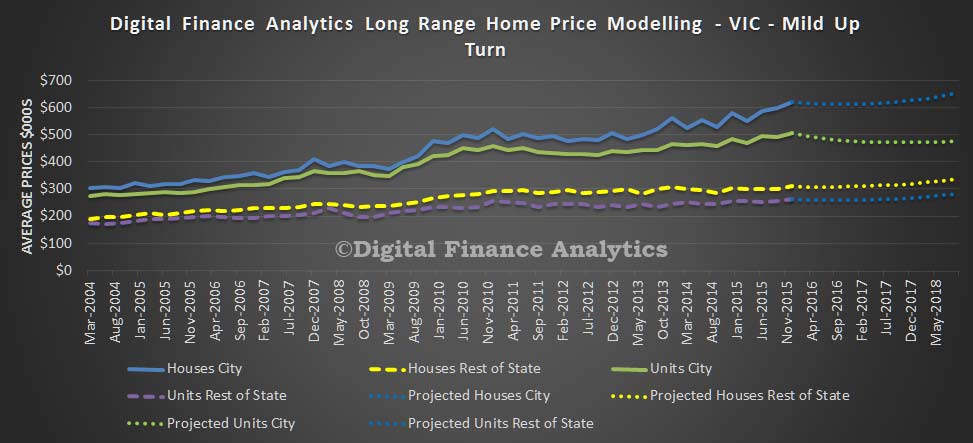

If economic momentum becomes stronger, to mid 2018, the average house price in Melbourne will rise by 5.1% to $653,000 and the average unit in Melbourne will fall by 5.7% to $476,000. In regional areas, the average house price will rise 3.4% to $337,000 and units will rise by 7.9% to $282,000. The rise in Melbourne will continue despite lower demand for investment property and static incomes. Over supply of units in the CBD will depress unit prices.

If economic momentum becomes stronger, to mid 2018, the average house price in Melbourne will rise by 5.1% to $653,000 and the average unit in Melbourne will fall by 5.7% to $476,000. In regional areas, the average house price will rise 3.4% to $337,000 and units will rise by 7.9% to $282,000. The rise in Melbourne will continue despite lower demand for investment property and static incomes. Over supply of units in the CBD will depress unit prices.

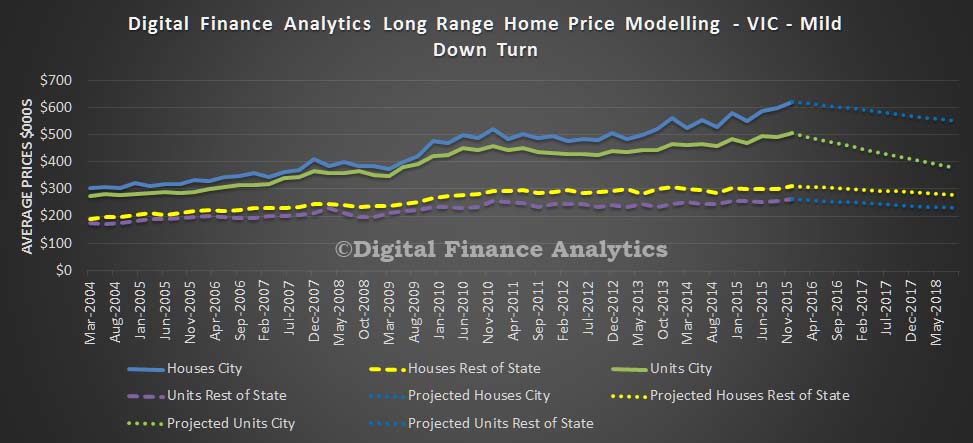

If economic momentum falls, to mid 2018, we expect to see the average house price in Melbourne fall by 11.6% to $549,000 and the average unit in Melbourne fall by 25.2% to $378,000. In regional areas, the average house price will fall 10.6% to $277,000 and units will fall by 12.6% to $228,000. In this scenario, growth remains low, unemployment moves higher, incomes remain flat, and demand for property slows.

If economic momentum falls, to mid 2018, we expect to see the average house price in Melbourne fall by 11.6% to $549,000 and the average unit in Melbourne fall by 25.2% to $378,000. In regional areas, the average house price will fall 10.6% to $277,000 and units will fall by 12.6% to $228,000. In this scenario, growth remains low, unemployment moves higher, incomes remain flat, and demand for property slows.

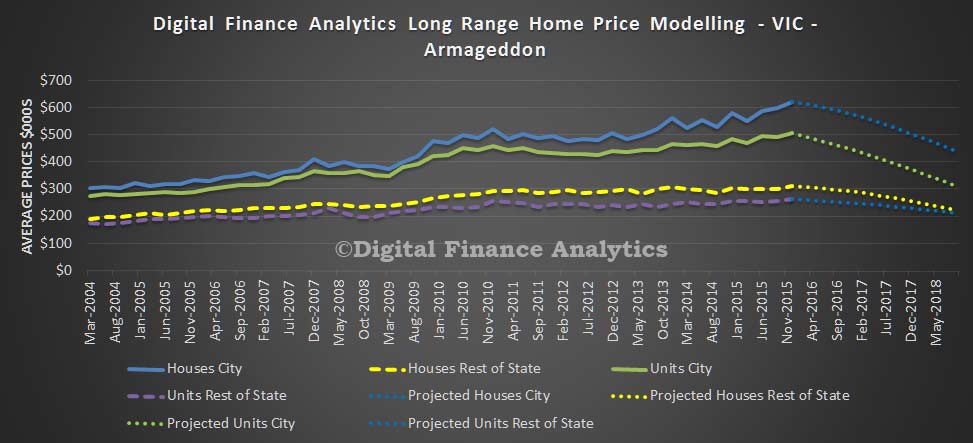

If economic momentum falls significantly, to mid 2018, we expect to see the average house price in Melbourne fall by 29.2% to $439,000 and the average unit in Melbourne fall by 38.4% to $311,000. In regional areas, the average house price will fall 28% to $223,000 and units will fall by 18.8% to $221,000. In this scenario, cash interest rates are cut further, unemployment rises, income falls in real terms, and demand for property falters. This is our Armageddon scenario.

If economic momentum falls significantly, to mid 2018, we expect to see the average house price in Melbourne fall by 29.2% to $439,000 and the average unit in Melbourne fall by 38.4% to $311,000. In regional areas, the average house price will fall 28% to $223,000 and units will fall by 18.8% to $221,000. In this scenario, cash interest rates are cut further, unemployment rises, income falls in real terms, and demand for property falters. This is our Armageddon scenario.

We see that the main area of risk centres on units in Melbourne, especially those within the CBD and surrounds. Supply is rising fast, at a time when demand is not matched.

We see that the main area of risk centres on units in Melbourne, especially those within the CBD and surrounds. Supply is rising fast, at a time when demand is not matched.

And a caveat, this modelling will be wrong, but it does give an indication of relative sensitives. Next time we will look at Brisbane and QLD.