Ten years ago this week, the first hints of risks in US mortgage portfolios emerged. French bank BNP Paribas wrote a warning of the risks in the US securitised mortgage system. Later, UK lender Northern Rock saw customers queuing to get their money from the bank, a reminder of what happens when confidence fails. Later still, Lehmann Brothers crashed. In the ensuing mayhem, as banks fell from grace and were either left to die, or were bailed out – mostly with public funds – and as mortgage arrears rocketed away in many northern hemisphere centres, the die was cast. In the subsequent period, growth has been sluggish, central government have cut their benchmark rates, and households have seen their incomes squashed, whilst asset prices have risen to amazing levels. Regulators responded with measures to force banks to hold more capital, but we are not out of the woods yet.

Australia, it seems dodged the bullet, either thanks to luck or good judgement, so we never directly experienced the full impact. But, on the 10th anniversary, its worth reflecting on whether our version of the GFC is still to come.

In 2009,the RBA’s then Head of Financial Stability Department, Luci Ellis gave a speech ” The Global Financial Crisis: Causes, Consequences and Countermeasures“. It is, in my view well worth reading in hindsight.

She makes the point that low policy rates in the early 2000’s allowed a flood of mortgages to to be written, lending standards to fall, (helped by the securisation of loans) and leverage to rise, significantly.

But in 2005, the Fed started to lift rates.

But you can’t borrow your way to a good time forever, and this recent example of a credit-fuelled boom was no exception. The first signs of trouble were in the US mortgage market. Lending standards had eased so far – and outright fraud had gotten to be such a problem – that arrears rates started to rise more than lenders and investors expected. The rise started in around 2006 for both prime and sub-prime mortgages, but became more obvious through 2007. The extraordinary thing was that, unlike in every other housing bust, arrears rates increased significantly before the labour market started to weaken.

Banks had enjoyed a bumper period of growth, as an article in the balance highlights. That created an asset bubble, and a building boom. (Any of this sound familiar?)

Banks, hit hard by the the 2001 recession, welcomed the new derivative products. In December 2001, Federal Reserve Chairman Alan Greenspan lowered the fed funds rate to 1.75 percent. The Fed lowered it again in November 2002 to 1.24 percent.

That also lowered interest rates on adjustable-rate mortgages. The payments were cheaper because their interest rates were based on short-term Treasury bill yields, which are based on the fed funds rate. But that lowered banks’ incomes, which are based on loan interest rates.

Many homeowners who couldn’t afford conventional mortgages were delighted to be approved for these interest-only loans. As a result, the percent of subprime mortgages doubled, from 10 percent to 20 percent, of all mortgages between 2001 and 2006. By 2007, it had grown into a $1.3 trillion industry. The creation of mortgage-backed securities and the secondary market ended the 2001 recession. (Source: Mara Der Hovanesian and Matthew Goldstein, “The Mortgage Mess Spreads,” BusinessWeek, March 7, 2007.)

It also created an asset bubble in real estate in 2005. The demand for mortgages drove up demand for housing, which homebuilders tried to meet. With such cheap loans, many people bought homes as investments to sell as prices kept rising.

Many of those with adjustable-rate loans didn’t realize the rates would reset in three to five years. In 2004, the Fed started raising rates. By the end of the year, the fed funds rate was 2.25 percent. By the end of 2005, it was 4.25 percent. By June 2006, the rate was 5.25 percent. Homeowners were hit with payments they couldn’t afford. For more, see Past Fed Funds Rate.

Housing prices started falling after they reached a peak in October 2005. By July 2007, they were down 4 percent. That was enough to prevent mortgage-holders from selling homes they could no longer make payments on. The Fed’s rate increase couldn’t have come at a worse time for these new homeowners. The housing market bubble turned to a bust. That created the banking crisis in 2007, which spread to Wall Street in 2008.

Now consider Australia. We have very high household debt, high home prices, flat income, rising living costs and ultra low, but rising mortgage rates. We also have a construction boom, with a large supply of new (speculative) property, and banks that have around 60% of their assets in residential property. Arguably lending standards are still too lose despite recent tightening (which note, had to be imposed on the lenders by the regulators!).

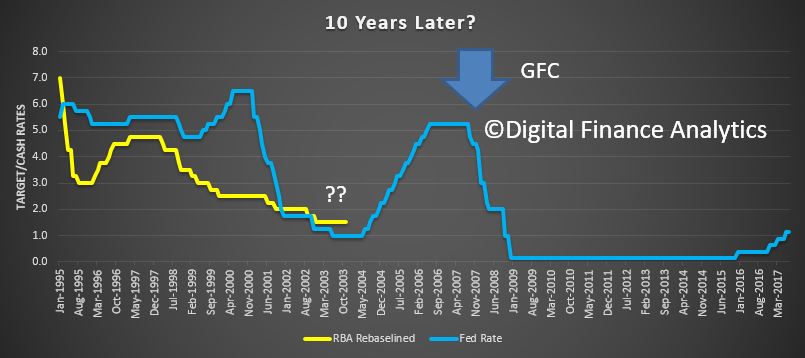

So, consider this illustrative chart. I plotted the Fed benchmark rate – you can clearly see the run-up to 2008/9 when the GFC hit, from low levels in 2003-2004. It took 3-4 years and a 4% uplift to lead to the crash.

Then I look the RBA cash rate and placed the current low rate in 2003. Do we face a series of rises ahead – the RBA says the neutral setting is 2% higher than current rates? If rates do rise, then mortgage rates will surely follow, and given the majority of households are on variable rates, pain will follow too. 25% of owner occupied borrowers are having cash flow problems already – at current low rates.

Then I look the RBA cash rate and placed the current low rate in 2003. Do we face a series of rises ahead – the RBA says the neutral setting is 2% higher than current rates? If rates do rise, then mortgage rates will surely follow, and given the majority of households are on variable rates, pain will follow too. 25% of owner occupied borrowers are having cash flow problems already – at current low rates.

So it seems to me the conditions are set for our own version of the GFC, and the bear-traps have already been laid by too high lending, high asset prices, and large debts in an ultra-low rate environment.

Of course banks hold more capital, of course the regulators are more aware, but is that enough? Judging by recent home price rises and continued lending growth such that household debt has never been higher, it may not be.