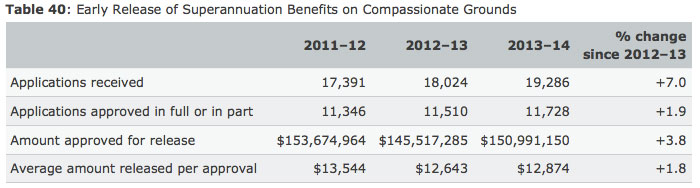

The Department of Human Services released their 2013-14 Annual Report. One topic of note is the rise in the early release of superannuation savings.

According to the DHS, Superannuation cannot generally be accessed before a person reaches their preservation age. In some limited circumstances the law allows for early access to superannuation. Most of the grounds under which early access is permitted are administered directly by the superannuation funds. These include:

- severe financial hardship

- terminal illness

- permanent incapacity

- balances of $200 or less

- permanent departure from Australia

The DHS is responsible for assessing applications for the early release of superannuation on compassionate grounds. These include payments for:

- medical or dental treatment for you or your dependent

- transport for medical or dental treatment for you or your dependent

- arrears on your mortgage to prevent your home being sold by your lender

- modification to your home or vehicle to accommodate a severe disability for you or your dependent

- palliative care for a terminal illness for you or your dependent

- expenses associated with your dependent’s death, funeral or burial

The regulations of compassionate grounds are set out in Australian law. While early access to superannuation is possible it is always subject to strict legal criteria. Applications must be supported by evidence. You must not be able to meet the costs by other means, such as savings

There was 7% uplift in withdraws, from last year, but the increase in applications was not matched by a rise in approvals by the department. Two-thirds of all applications were approved in full or part, with the total value of early payouts rising only 3.8%, or $5.4 million, to $151 million. The average payment approved by the department rose only two per cent to $12,874 from $12,643 in 2012/13. This is small beer relative to the $1.85 billion in super held by Australians and will reduce the chatter about the rising hardship levels amongst households. The main motivation is to pay down the mortgage, and this is confirmed by our household surveys.