The NZ Reserve Bank today left the Official Cash Rate unchanged at 2.5 percent. The statement by Reserve Bank Governor Graeme Wheeler highlights the risks in the outlook.

Uncertainty about the strength of the global economy has increased due to weaker growth in the developing world and concerns about China and other emerging markets. Prices for a range of commodities, particularly oil, remain weak. Financial market volatility has increased, and global inflation remains low.

The domestic economy softened during the first half of 2015 driven by the lower terms of trade. However, growth is expected to increase in 2016 as a result of continued strong net immigration, tourism, a solid pipeline of construction activity, and the lift in business and consumer confidence.

In recent weeks there has been some easing in financial conditions, as the New Zealand dollar exchange rate and market interest rates have declined. A further depreciation in the exchange rate is appropriate given the ongoing weakness in export prices.

House price inflation in Auckland remains a financial stability risk. There are signs that the rate of increase may be moderating, but it is too early to tell. House price pressures have been building in some other regions.

There are many risks around the outlook. These relate to the prospects for global growth, particularly around China, global financial market conditions, dairy prices, net immigration, and pressures in the housing market.

Headline CPI inflation remains low, mainly due to falling fuel prices. However, annual core inflation, which excludes temporary price movements, is consistent with the target range at 1.6 percent. Inflation expectations remain stable.

Headline inflation is expected to increase over 2016, but take longer to reach the target range than previously expected. Monetary policy will continue to be accommodative. Some further policy easing may be required over the coming year to ensure that future average inflation settles near the middle of the target range. We will continue to watch closely the emerging flow of economic data.

Information received since the Federal Open Market Committee met in December suggests that labor market conditions improved further even as economic growth slowed late last year. Household spending and business fixed investment have been increasing at moderate rates in recent months, and the housing sector has improved further; however, net exports have been soft and inventory investment slowed. A range of recent labor market indicators, including strong job gains, points to some additional decline in underutilization of labor resources. Inflation has continued to run below the Committee’s 2 percent longer-run objective, partly reflecting declines in energy prices and in prices of non-energy imports. Market-based measures of inflation compensation declined further; survey-based measures of longer-term inflation expectations are little changed, on balance, in recent months.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. The Committee currently expects that, with gradual adjustments in the stance of monetary policy, economic activity will expand at a moderate pace and labor market indicators will continue to strengthen. Inflation is expected to remain low in the near term, in part because of the further declines in energy prices, but to rise to 2 percent over the medium term as the transitory effects of declines in energy and import prices dissipate and the labor market strengthens further. The Committee is closely monitoring global economic and financial developments and is assessing their implications for the labor market and inflation, and for the balance of risks to the outlook.

Given the economic outlook, the Committee decided to maintain the target range for the federal funds rate at 1/4 to 1/2 percent. The stance of monetary policy remains accommodative, thereby supporting further improvement in labor market conditions and a return to 2 percent inflation.

In determining the timing and size of future adjustments to the target range for the federal funds rate, the Committee will assess realized and expected economic conditions relative to its objectives of maximum employment and 2 percent inflation. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments. In light of the current shortfall of inflation from 2 percent, the Committee will carefully monitor actual and expected progress toward its inflation goal. The Committee expects that economic conditions will evolve in a manner that will warrant only gradual increases in the federal funds rate; the federal funds rate is likely to remain, for some time, below levels that are expected to prevail in the longer run. However, the actual path of the federal funds rate will depend on the economic outlook as informed by incoming data.

The Committee is maintaining its existing policy of reinvesting principal payments from its holdings of agency debt and agency mortgage-backed securities in agency mortgage-backed securities and of rolling over maturing Treasury securities at auction, and it anticipates doing so until normalization of the level of the federal funds rate is well under way. This policy, by keeping the Committee’s holdings of longer-term securities at sizable levels, should help maintain accommodative financial conditions.

Globalisation – and the global economic crisis – have contributed to the erosion of national tax bases and in recent years some of the biggest multinationals, among them Apple, Vodafone, Amazon, Google, Starbucks and Microsoft, have been scrutinised for their aggressive tax planning practices. Using (among other techniques) transfer pricing, inter-company lending, royalty payments for licensing agreements, cost-sharing agreements and offsetting group losses, multinational groups can achieve very low effective tax rates.

The ability to shift profits into low or no-tax jurisdictions with little corresponding change in business operations has also been criticised. Fuelled by media attention the reporting of these practices has in some countries led to public outcry and politicians seem to have jumped on this bandwagon.

Google’s £130m tax deal with HMRC is the latest instalment in a “UK vs Google” saga. Google’s encounters with the UK’s parliamentary public accounts committee had already been recorded in a report: “Tax Avoidance – Google. At the time, the committee questioned how Google, which generated US$18 billion (£12.6 billion) in revenue from the UK between 2006 and 2011, could only pay the equivalent of just US$16m (£11.2m) of UK corporation taxes in that same period.

The company used the now-defunct “double Irish” structure to achieve these low effective tax rates. Central to Google’s tax planning was the position that sales of advertising space to UK clients took place in Ireland. The public accounts committee found this “deeply unconvincing” back in 2013. But arguments against Google’s position relied on concepts of morality and fairness rather than clear tax rules – and this is the problem.

Google has now agreed to pay £130m in back taxes. To put this into context, consider that Google made more than £3 billion in UK sales in 2013 alone. Some (mainly the chancellor of the exchequer and HMRC) see this as a big success, while others have labelled it as “derisory” and “a sweetheart deal”.

These stories provide fertile ground both for the government and the opposition to raise the stakes: the government is arguing that it is doing more to curb tax avoidance than previous (Labour) governments and the opposition is arguing that this government is not doing enough.

Letter of the law

What underpins the whole anti-Google, anti-Starbucks, anti-Vodafone rhetoric is the idea that multinationals should follow the spirit and not just the letter of the law – and pay taxes accordingly. This is buttressed by an overriding concept of “tax morality” or “tax justice” which trumps the actual legislation.

Facebook is thought likely to strike a similar deal to Google’s.Reuters/Dado Ruvic

By contrast, what underpins the comments of those who defend the tax planning practices of these multinationals is the idea that legality and illegality is determined according to whether or not they complied with the law. If people disapprove of tax planning practices, whether perceived to be aggressive or not, but still legal, then they should press their governments to change the relevant tax laws.

You can understand why words like “morality”, “fairness” and “justice” are attractive in this context, but the reality of the situation is that most of these instances of aggressive tax planning (or stateless income, as coined in the US) are not technically illegal. In other words, current domestic tax laws and the vague non-binding principles of international tax law seem to facilitate such tax planning – some might even say, encourage it.

New initiative

What has clearly emerged in the last few years of “tax crusades” is the inadequacy and unsuitability of existing principles of international tax law to deal with the internationalisation of business. Some argue that existing tax rules on jurisdiction in particular need to be adapted to new business models such as digital. Others argue that existing principles are sufficient but there is discord as to how tax authorities ought to apply them.

The OECD/G20, in the context of its Base Erosion and Profit Shifting (BEPS) project, has tried to find solutions to some of these issues through consensus – something initially thought of as nearly impossible.

The OECD launched its BEPS action plan on multinational tax minimisation in 2015.OECD

However, to the surprise of some, the OECD did meet its deadlines and produced recommendations for the issues raised in an action plan. These recommendations were set out in the final reports it published in October 2015. Whether the BEPS project will make it easier (and more transparent) for tax authorities to tackle aggressive tax planning remains to be seen. However the international tax community, through the OECD/G20, is making an effort to address existing problems and should be at the very least congratulated for its efforts and encouraged to continue.

The European Union has also been at the forefront of these developments. While most associate the European Union with open borders and market liberalisation – with member states’ budgetary concerns of secondary importance – the European Commission has seized on this unique political momentum to further its agenda. The various commission action plans and recommendations evince the inception of a strong EU policy against international tax avoidance. The recent state aid actions, also spearheaded by the commission – which prevent national governments from giving corporations “an unfair competitive advantage” – seem to corroborate this.

Whether or not one agrees with the EU’s – some would say slightly overkill – approach, it should nevertheless remain a priority for those working in tax to address the inadequacy of the existing rules with new or refined rules and principles – not with the injection of vague notions of morality and fairness. The UK has made a valiant attempt to (partially) address the problems with its Diverted Profits Tax also known as “Google Tax”. This legislation broadly allows HMRC (under certain circumstances) to tax the profits of multinationals arising from business activities taking place in the UK when there is no taxable presence, because of contrived arrangements diverting these profits from the UK.

While this unilateral stance has been criticised for going against the spirit of multilateralism in the BEPS project, it is a welcome example of rules – some would say imperfect rules – filling in the gaps of the international tax system. The enemy is not just complacency – it is also uncertainty and vagueness.

Author: Christiana HJI Panayi, Senior Lecturer in Tax Law, Queen Mary University of London

ANZ Chief Executive Officer Shayne Elliott today announced changes to the bank’s senior leadership team to improve focus on its retail, commercial and institutional customers. Commenting on the changes Mr Elliott said: “ANZ has terrific retail and commercial businesses in Australia and New Zealand and we have a great global institutional bank servicing regional trade and capital flows.

“These changes simplify how we work internally and allow us to bring greater focus to what we do uniquely well for our customers. The aim is to ensure we successfully compete in a world where connectivity and digital are more important to customers than ever before and where community expectations have never been higher,” he said.

Announcing the changes, which are effective from Monday 1 February, Mr Elliott also set out a number of medium-term priorities for ANZ:

Delivering value for customers through more innovative, convenient and engaging financial services.

Being Australia’s only truly regional bank by delivering solutions for customers through a more focussed, better connected international network.

Continuing to build a strong, cohesive culture known for ethics, values and fairness.

Delivering consistently strong financial results for investors balancing growth and return.

“The new structure brings greater clarity to what we do best for our customers with a leadership team that reflects a diverse mix of experience and new talent from inside and outside ANZ,” Mr Elliott said.

Institutional

Mark Whelan – Group Executive, Institutional with responsibility for Institutional Banking. Mr Whelan is one of ANZ’s most experienced executives having most recently been CEO Australia. Formerly Mr Whelan was Managing Director Commercial Australia and his previous roles include Managing Director Institutional Asia Pacific, Europe and America based in Hong Kong, and Joint Managing Director Global Markets.

Farhan Faruqui, Group Executive, International reporting to Mr Whelan and based in Hong Kong, will have responsibility for ANZ’s Institutional business in Asia, Europe and America. He will also join ANZ’s Executive Committee reflecting the strategic importance of Asia to ANZ’s future success.

Retail and Commercial

Fred Ohlsson – Group Executive, Australia with responsibility for Retail and Commercial Banking in Australia. Mr Ohlsson comes to the role from ANZ New Zealand where he has been Managing Director, Retail and Business Banking since 2013. He has worked in a range of senior roles at ANZ since 2001 including General Manager Commercial Products (Australia) and General Manager Products and Marketing for Esanda

David Hisco – Group Executive and CEO, New Zealand. Mr Hisco will continue in his role as Chief Executive Officer, ANZ Bank New Zealand Limited and will have additional responsibility for the Pacific (excluding Papua New Guinea), given its strong New Zealand linkages, and for ANZ’s retail business in Asia.

Joyce Phillips – Group Executive, Wealth, Marketing and Innovation with responsibility for ANZ’s insurance, investments and private banking businesses, as well as Group Marketing and Innovation.

A new role of Group Executive, Digital Banking will be established with responsibility for ANZ’s digital transformation. An external appointment to the role is expected to be announced in the coming months.

Other members of ANZ’s Executive Committee continuing to report to Mr Elliott are:

Graham Hodges – Deputy Chief Executive Officer who will have responsibility for ANZ’s international partnership investments in Indonesia, Malaysia, China and The Philippines. Mr Hodges will also remain Acting Chief Financial Officer. The internal and external search for a new Chief Financial Officer is well advanced and is expected to be finalised in the coming months.

Susie Babani – Chief Human Resources Officer

Alistair Currie – Chief Operating Officer

Nigel Williams – Chief Risk Officer

As part of the changes Gilles Planté, Deputy CEO Institutional and International Banking, Managing Director Business Portfolio Management and a member of ANZ’s former Management Board will be leaving ANZ.

DFA observes that the new GE Digital Banking is interesting, given that digital touches every aspect of banking and their customers. How will digital capabilities be overlaid on the existing operations?

The latest Australian Bureau of Statistics (ABS) figures show the Consumer Price Index (CPI) rose 0.4 per cent in the December quarter 2015, following a rise of 0.5 per cent in the September quarter 2015.

The most significant price rises this quarter were in tobacco (+7.4 per cent), domestic holiday travel and accommodation (+5.9 per cent) and international holiday travel and accommodation (+2.4 per cent). These rises were partially offset by falls in automotive fuel (–5.7 per cent), telecommunication equipment and services (–2.4 per cent) and fruit (–2.6 per cent).

The increase of 0.1 per cent for the housing group is the weakest movement since March quarter 1998 as price rises for rents (+0.2 per cent) and new dwelling purchase by owner occupiers (+0.1 per cent) have been subdued through the quarter. The 0.1 per cent rise for new dwellings purchase by owner occupiers is the weakest movement since March quarter 2014.

The CPI rose 1.7 per cent through the year to the December quarter 2015, following a rise of 1.5 per cent through the year to the September quarter 2015.

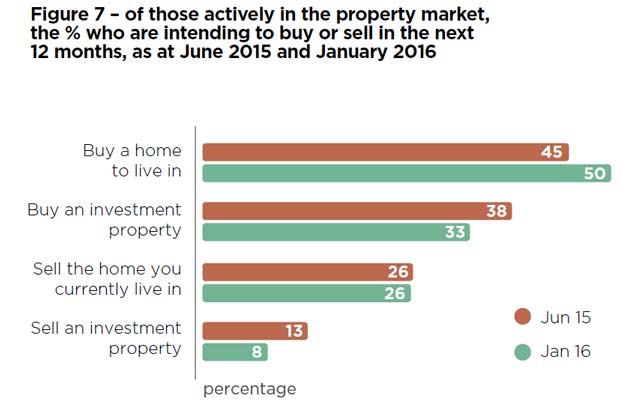

ME’s latest Property Buying Intentions Report indicates demand for residential property may remain strong over the next 12 months despite prudential changes and tightening of lending criteria for some home buyers. The Report shows a big jump in demand for property by owner occupiers potentially offsetting falling demand by investors, while buyers continue to outnumber sellers.

According to the Report:

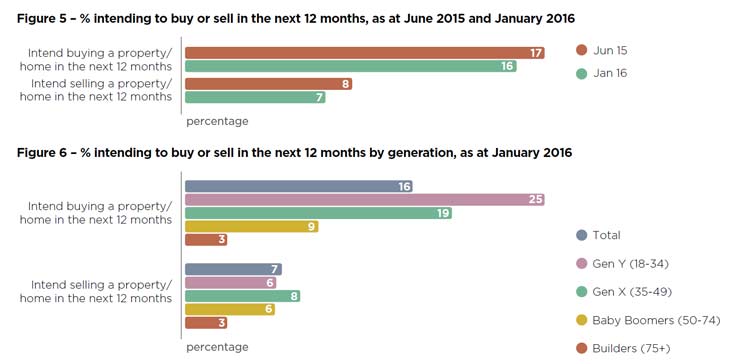

In the six months to December 2015, the proportion of Australians intending to buy a property/home fell 1 point to 17%, matched by a correspondingly small fall in the proportion intending to sell a property/home (down 1 point to 7%). Buyers continue to outnumber sellers by more than two-to-one.

Over the same six month period and among those actively looking to buy and/or sell property during 2016, there was a 5 point increase to 50% in the proportion looking to buy a home to live in (owner occupier buyers) offsetting a 5 point fall to 33% in the proportion looking to buy an investment property (investor buyers).

Also among those active in the property market, planned sales by home owners remained unchanged over the six months to December at 26%, while there were fewer intended sellers of investment properties (down 5 points to 8%).

ME Treasurer, John Caelli, said notwithstanding other factors, the findings indicate property demand pressures from buyers may remain strong over the next 12 months. “While recent tightening in bank prudential regulations and lending criteria have reduced the proportion of investor buyers, overall demand for property may remain strong due to increased demand by owner occupier buyers. “Demand expectations from buyers may also remain strong due to unmet demand from owner occupiers supported by continued low borrowing costs and recent improvements in the labour market.”

Other findings

23% of Gen Y are saving to buy a property to live in and 25% intend to buy a property to live in in the next 12 months, the most of any age group.

10% of Gen X are saving to buy an investment property and 8% intend to buy an investment property in the next 12 months, the most of any age group.

The proportion of first home buyers has increased slightly to 22% in the six months to December 2015, up 1 point.

Of those actively looking to buy or sell a home to live in in the 12 months, 19% are downsizers, 22% are upgraders and 59% are looking for property with a similar price point.

About the House Buying Intentions Report

ME commissioned DBM Consultants to conduct an online survey of approximately 1,500 Australians aged 18 years and older who do not work in the market research or public relations industries. The population sample was weighted according to ABS statistics on household composition, age, state and employment status to ensure that the results reflected Australian households.

Each quarter CommSec attempts to find out by analysing eight key indicators: economic growth; retail spending; equipment investment; unemployment; construction work done; population growth; housing finance and dwelling commencements. The latest data is just released, and NSW has retained top spot as the best performing economy, edging a little further ahead of Victoria. Both states are maintaining a healthy lead over the other states and territories.

The big change over the past quarter has been the lift of the ACT economy to equal third position alongside the Northern Territory. Western Australia has dropped from fourth to fifth. But there is little to separate the ACT and the Northern Territory in the second grouping of economies.

In the third grouping of state and territory economies, Queensland is sixth ranked, ahead of the South Australia (seventh) and Tasmania (eighth).

Their measurement has a strong bias towards housing and finance, with 3 metrics directly linked, and others indirectly influenced. The slowing resources sector is hitting QLD and WA in particular.

NAB has launched its new mobile payment service NAB Pay, enabling customers to use their Android mobile phone to make purchases, without the need for a physical card. Customers with a compatible Android mobile device and a NAB Visa Debit Card can start using NAB Pay from today, available as part of the NAB Mobile Internet Banking App. NAB Executive General Manager for Consumer Lending, Angus Gilfillan, said customers were driving the agenda and increasingly wanted simple and easy digital payment solutions.

“We’re excited to launch our digital wallet and enable customers to make fast and safe purchases with their mobile phone”

NAB will also be the first Australian bank to utilise Visa Token Service in Australia, providing an important extra layer of security for customers. Tokenisation replaces a customer’s credit card number with a unique digital ‘token’ that can be used for digital payments, without revealing sensitive account information.

“Tokenisation improves protection for customers because physical card details are never used in the payments process, reducing the risk of fraud. NAB Pay gives consumers another reason to choose NAB as we continue to focus on delivering the number one cards experience in Australia.”

Last year, NAB announced a ten-year strategic partnership with Visa to collaborate on payments innovation and product development for customers.

“Our partnership with Visa is enabling us to significantly invest in our credit and debit card portfolio and act more quickly to deliver innovative solutions for our customers – as today’s announcement shows. We have a number of exciting initiatives planned this year and look forward to extending the NAB Pay application to support NAB credit cards in coming months.”

To use NAB Pay, customers will need a compatible Android device, have downloaded the latest NAB Mobile Internet Banking App and have a NAB Visa Debit card. NAB Pay is available wherever contactless payments are accepted.

This can see seen as a competitor to Apple Pay. which currently in Australia only works with Amex cards.

It’s been a shaky start to 2016 for global stock markets, with substantial falls across all international markets, followed by some weak rallies.

The overall decline has been partly blamed on the price of crude oil, which is hovering around US $30 a barrel down from $100 over a year ago, along with market fears on the overall health of the Chinese economy.

However the most likely driver of further market deterioration is not a further decline in oil prices, but the negative sentiment itself. This is due to a flaw in the way analysts ascribe value in markets that behavioural economists call “anchoring bias”.

This is the idea that people tend to start from what they know and then attempt to make appropriate adjustments based on this. Over 40 years of research has found that these adjustments tend to be insufficient.

Everyone can be prone to this bias, there are a few studies that demonstrate this. For example, when people were asked which year George Washington became the first US President, most would start from the year the US became a country (in 1776). They would reason that it might have taken a few years after that to elect the first president so they add a few years to 1776 to work it out, coming to an answer of 1778 or 1779. George Washington actually became president in 1789.

Similarly, most people would know the freezing point of water (0 degrees celcius) as compared to vodka. So if they were asked what the freezing temperature of vodka is, they would tend to start from 0 and adjust downwards. The freezing temperature of vodka is around -24 degrees celcius, much lower than what people usually answer.

Both these examples demonstrate how the reasoning associated with anchoring bias leads to people falling significantly short of the right answer.

In the case of the stock market, analysts look to the performance of blue-chip stocks linked to commodities like oil because they are associated with large, well established companies with time-tested business models. There are large data sets available with which to analyse these stocks.

However less than 4% of companies are classified as blue-chips globally. What about the remaining 96%? To value them, analysts may start from the payoffs of blue-chips and then attempt to make appropriate adjustments for size and other differences.

The overreaction of the market in relation to oil prices is further exposed by the fact that lower oil prices aren’t all bad news. Low oil prices can be good for countries that import oil as well as their consumers, retailers and industry because higher production of goods drives cheaper prices leaving more money in the pockets of consumers to spend.

Other economic indicators also tell a very different story to the oil price. Job numbers are good both in the European region and US, and growth seems to be picking up.

If analysts and investors continue to display anchoring bias and the oil price drops, it could become a self fulfilling prophecy where a prolonged market slump cuts off investment, reduces consumption, and pushes the global economy into a recession. Central banks will do what they can to prevent this from happening by talking of quantitative easing. However, the interest rates are already near zero so they do not have much room to move.

Author: Hammad Siddiqi, Research Fellow in Financial Economics, The University of Queensland

At a time of global economic insecurity, an insightful commentator identified the existential threat that technology poses to work:

We are being afflicted with a new disease of which some readers may not yet have heard the name, but of which they will hear a great deal in the years to come – namely, technological unemployment. This means unemployment due to our discovery of means of economising the use of labour outrunning the pace at which we can find new uses for labour.

These words by John Maynard Keynes in 1930 remind us that contemporary anxiety over jobs being taken from us by robots is not so far removed from fears of a greater vintage.

Indeed, the more these fears are periodically recycled and perennially assuaged, the less potent they appear to those who are sensitive to the long arc of human history. Nonetheless, this has been one of the major themes of discussion by world leaders at Davos.

John Maynard Keynes.

The exponential growth of digital technology since the 1990s has brought us to the “fourth industrial revolution”. Advancements have reached the point where highly skilled jobs are as susceptible to replacement by automation as ones which do not require much education or training. This is vividly exemplified by Silicon Valley entrepreneur Martin Ford’s contrasting of the radiologist’s vulnerability to automation with that of a housekeeper, whose decision-making processes are less easily replicated.

This is compounded by the concern that this new type of economy does not provide enough compensating positions for the jobs automated out of existence. As an illustration of how the most innovative digital companies can generate huge wealth on the back of the toil of relatively small numbers of people, look at how Google’s market value of US$377 billion is supported by just 53,600 global employees. Contrast this with General Motors‘ market value of US$60 billion and 216,000 employees.

This divergence would not be significant in an economy where the business of each company was completely separate. Now, though, the tech giants’ operations have seeped into other spheres of business, such that Google’s driverless cars makes the company a direct competitor of General Motors.

Martin Wolf, the Financial Times’ chief economics commentator, argues that these tectonic shifts should open up a space for a rethinking of our attitudes towards work and leisure. Rather than lamenting what automation robs us of, why not use it to generate greater opportunities for leisure and education, as well as liberate us from our constant anxiety that we will not be able to support our families in this unstable environment?

An obvious way to do this is by way of a basic income – redistribute wealth and give all citizens a flat, unconditional income. The idea is grounded in decades-old ideas and experiments. The Democratic candidate in the 1972 US election, George McGovern, for example, proposed a “Demogrant” of US$1,000 a year for every American.

Robert Reich, the labour secretary in Bill Clinton’s first presidential term has also advocated a combination of minimum income, earnings insurance and a US$60,000 nest egg for each citizen to cushion against the violent vicissitudes of the modern global networked economy. And, as Wolf advocated, Swiss campaigners for a basic income framed their arguments around the notion of improving citizens’ work-life balance.

It might surprise the reader to discover that ideas for a basic income come from figures on the right too, including the libertarian economist Friedrich Hayek. They were manifest in proposals for a negative income tax, first advocated by Milton Friedman in 1962, and which almost came to fruition during the Richard Nixon presidency in the form of the Family Assistance Plan.

The failure of this plan to get off the ground was accompanied by a series of negative income tax pilot schemes in a number of US cities with less than stellar results. Despite this, Conservative thinkers like David Frum argue that introducing a basic income would cut bureaucracy by eradicating the thicket of anti-poverty programmes currently in place. A number of new schemes – most recently in the Dutch city of Utrecht – might give us a better indication than their 1970s forebears of how these experiments might work in our highly automated economies.

Something that the head of the World Economic Forum, Klaus Schwab, has been keen to emphasise is the increasing tendency for benefits of the digital revolution to accrue to the many not the few. “As automation substitutes for labour across the entire economy, the net displacement of workers by machines might exacerbate the gap between returns to capital and returns to labour,” he said.

Keynes prediction in 1930 that within a hundred years people in the richest nations would be working only 15 hours a week might not come to pass. But given the potential of automation to confound economists’ employment projections, those gathering at Davos would be remiss to not consider a basic income as a credible policy response to contemporary anxieties about our role in the modern workplace.

Author: Andrew White, Associate Professor of Creative Industries & Digital Media, University of Nottingham

{kind=link}