The Turnbull government’s budget this week went a long way to neutralising the policy issues that Labor exploited at the last federal election, especially by whacking the big banks. But the government deliberately left itself exposed on the one issue that could bring it down.

The Coalition can now claim to have cracked down on big banks, who have managed to make themselves public enemy number one by treating customers poorly while raking in huge profits and showing inadequate contrition for the shonky operators among their ranks.

It’s impossible to tell definitively which budget measures were the result of rigorous policy analysis within the bureaucracy, and which were cooked up as a quick political fix in the minister’s office.

The deficit levy in 2014 on very high income earners was reported to be a relatively last-minute decision by the Abbott administration to pre-emptively counter accusations that the budget only imposed cuts on students, the elderly and the unemployed.

This year’s levy on the banks could be seen in a similar light, with reports emerging that Treasury officials who met with bank representatives after the budget knew very little about the levy or how it might operate.

The crackdown on banks involves more than just the levy. There is also a new requirement for bank executives to be registered with the industry’s regulator, with the attendant threat that bankers can be struck off the register for misconduct and stripped of their bonuses. Banks found guilty of misconduct will also face increased fines.

The government could argue these reforms would have been the likely outcome of a royal commission.

This of course does not sate the community’s desire for bankers to be subjected to a public inquisition and then metaphorically placed in the stocks or strapped to a crackling pyre.

Even though the government was prepared to reverse its position on a number of other policy issues, such as Gonski, it apparently didn’t see the benefit of conceding to Labor on a banking royal commission.

Perhaps this is because it occurred to Treasurer Scott Morrison that he could discipline the banks while filling a revenue hole at the same time.

It is no secret the Treasurer is unhappy with the banks – and not just because they’re singularly ungrateful for the government’s protection against the indignities of a royal commission.

ScoMo is unhappy because they appointed a senior Labor identity – former Queensland premier Anna Bligh – as their chief lobbyist.

That role had reportedly been earmarked for one of Mr Morrison’s senior advisers, and the Treasurer had apparently given his blessing for the appointment.

Anyone with an ounce of political common sense knows that lobby groups are unwise to appoint someone of the opposite political flavour to the government of the day.

The only exception to this rule is if it’s close to an election and there is a good chance the government will change.

Canberra circles are rife with stories of ministers and their staff not only refusing to meet with such lobbyists, but excluding them from other consultation processes.

Retribution can even extend to unfavourable policy decisions, as the bankers learned on budget night.

The Treasurer would be pretty happy with the outcome of the decision so far.

The bankers are squealing, voters don’t like one of the most trusted political faces in recent history shilling for the banks, and Labor can’t claim any credit for the crackdown.

ScoMo will also be confident in the knowledge that if the banks try to pull a mining tax rebellion – with a multimillion dollar advertising campaign – they will only reinforce voters’ resentment and the resulting backlash will demonstrate just how unpopular the banks are.

Big business tax cuts may be ScoMo’s undoing

However, just as Tony Abbott’s deficit levy didn’t magically make the rest of the 2014 budget fair, the banks levy can’t do the same for this year’s budget.

The decision to double down on promised tax cuts for the big end of town will be an albatross that PM Turnbull carries to the next election.

This is even more the case now that low-income taxpayers will be required to pay the Medicare levy increase for the NDIS and the total 10-year bill for business tax cuts has blown out to $65 billion. This weakness could have so easily been avoided.

The government could have set aside the big business tax cuts until the budget was in surplus (until we can afford it), or the average net tax raised from big corporates exceeded a certain threshold (until they are paying their fair share of tax).

For a budget that was so smart on politics, the decision to keep the tax cut for big business was dumb.

Leaving it on the books simply gives Labor a free kick. No wonder it was the main feature of Opposition leader Bill Shorten’s budget in reply address.

If voters conclude the Turnbull government is no better than the banks in wanting to rip them off, it will be the PM and the Treasurer being dragged to the stocks and the pyre at the next election.

With it’s latest budget the government has made a number of moves to create a level playing field in the banking system. It’s taxing the five largest banks, announced a review of rules around data sharing, a new dispute resolution system for banks and other financial institutions, and new powers for the regulator to make bank executives accountable.

All of this is on top of a Productivity Commission inquiry into the competition within the Australian financial system, announced this week.

While some of these moves – such as the bank levy – will have a positive effect on making smaller banks more competitive, there are more policies that could be considered. These could include the separating out of the retail arms from the other areas of the large banks, increasing the capital requirements of larger banks to equal those of smaller banks, and developing new sources of funding for smaller banks.

More for competition

A new “one-stop shop” for dispute resolution will replace the existing three schemes – Financial Ombudsman Service, the Credit and Investments Ombudsman and the Superannuation Complaints Tribunal. Called the Australian Financial Complaints Authority (AFCA), it will give consumers, businesses and investors a binding resolution process when dealing with financial services companies. The scheme will provide for a basis for more competition as disputes on financial services are consistently resolved regardless of the provider.

And A$1.2 million has been given to fund a review of an open banking system in which customers can request banks to share their data, which could assist financial startups and other competitors enter the market and compete against the big four banks. Banks will likely be forced to provide standardised application programming interfaces (API) that enable financial technology companies to provide services for interested consumers.

The government has also provided A$13.2 million to the Australian Competition and Consumer Commission (ACCC) to further scrutinise bank competition and to run the AFCA. This follows a House of Representatives report that called for an entity to make regular recommendations to improve competition and change the corporate culture of the financial industry.

The ACCC will provide Treasury with ongoing advise on how to boost competition in the sector. This may include a reduction of cost advantages of big banks, barriers to entry for new firms including change costs for consumers.

A more concentrated and changing finance sector

All of these changes come after a decade of consolidation and upheaval in the financial system, which has hurt competition and increased risk.

This chart shows the market shares of the big four Australian banks in terms of Australian loans and deposits:

Market share Big 4 banks.Australian Prudential Regulation Authority

As you can see, since 2002 their market share has grown from 69.7% to 79.6% for loans and from 66.3% to 77.3% for deposits. Also, the gap between market dominance in loans versus deposits has closed since the global finance crisis. This means the big banks are attracting a greater share of bank deposits, which has an impact on the smaller banks.

With limited access to deposits, which is a relatively cheap way of raising capital, smaller banks have had to rely on the more expensive wholesale debt markets. Small banks also have difficulties to tap other funding sources such as covered bonds. This makes their products less competitive, and they have struggled as a result.

In part, that’s because a number of banks disappeared or merged with the big banks after the global financial crisis. This includes St George, Bankwest, Bendigo Bank, Aussie Home Loans, Adelaide Bank, RAMS and Wizard.

The Murray Inquiry found the big four banks have less than half the capital set aside for emergencies than some smaller financial institutions do. Again, this makes the smaller banks less competitive and needs to be addressed. The government should increase the capital requirements of larger banks to close the cost advantage for larger banks.

In addition, rising house prices have led to a further increase in the concentration of mortgage and other housing loans in the Australian banking system. Today Australian banks have about twice as many mortgages on their books as in the next highest developed economy.

New financial startups, such as peer-to-peer lenders, have entered the banking system. In time they may rival the big banks in areas like personal lending, but they remain small in terms of market share. And the big banks’ unwillingness to share data may be a hindrance.

Something needed to be done

The concentration in the banking sector does not provide the best outcome to all Australians. It has led to a low range and low quality of financial services as well as high costs. This needed to be addressed.

The new banking levy will support competition, as it pushes up the cost for the big banks. The review into data sharing could also be a boon to financial startups and other competitors, although we don’t yet know what the outcome will be.

But even stronger government actions may needed to create a level playing field. The government should consider separating out of the retail arms, from the other areas, of the large banks. Failing that, the low capital buffers of the big banks need to be addressed.

Author: Harry Scheule, Associate Professor, Finance, UTS Business School, University of Technology Sydney

The latest edition of our weekly digest is published today. In the week the big banks copped it in the budget, and investor borrowing momentum is predicted to slow, we look at events over the past seven days. Watch the video, or read the transcript.

We start with the main announcements in the Budget. First there is the $6 billion liabilities levy to be imposed on the big four banks and Macquarie. Whilst many were surprised by this move, the fact is that banks around the world are getting hit with various taxes and levies and we have some of the most profitable banks in the world, not because they are really expert managers, but because of the structural issues which exist here.

Most of the tax grabs around the world are aligned to providing extra support in case a bank failures, but others are now using the income to support general government spending. In some ways the banks are easy targets, given their massive incomes, and poor public perception, but in our view the move looks more like a late tax grab to fill a hole than clear sighted policy. Of course the banks squealed, whilst smaller players suggested it might help to level the competitive playing field. Banks have so many ways to recover such an impost, that despite the mandate given to the ACCC to monitor price changes, we think consumers and small business will pay, and so it is really just another indirect tax. The Government linked the move to the earlier Financial System Inquiry as part of making Banks “Unquestionably Strong”, but this is a long bow.

We think the other developments relating to banking in the budget are perhaps more significant. APRA is to be given extra powers to supervise the growing non-bank sector, which may help to cool the supply of higher risk mortgages. Bank executives will be on a register and risk being delisted if they do the wrong thing. This is all about tightening the bank system further, and it makes good sense. It also represents a vote of no-confidence in their self-managed campaigns to improve the culture in banks, and which do not necessarily get to the heart of the issues which need to be addressed.

But it is the Productivity Commission review of the financial system, and especially the issues around vertical and horizontal integration which may have the most profound impact. Today, the large financial conglomerates control hosts of financial advisers and mortgage brokers, as well as branch networks and other channels, and play across the spectrum from retail banking, through wealth management and Insurance. But such integration means that smaller players cannot compete, and large players are able to dictate prices across the system. As a result, Australians are paying more for their financial services than they should, many sectors are making excess profits, and competition is just not working. So the big question becomes, will the Productive Commission get to the heart of the issues, and can the financial services omelette be unscrambled?

Going back to the levy for a moment, we cannot figure why Macquarie is caught along with the big four, who are classified by APRA as Domestically Significant Banks or D-SIBS. The basis of selection appears to be a quick back of the envelope assessment of the size of liabilities (less consumer deposits below $250k and Basel Capital). The fact is the major banks have an implicit government guarantee that in case of emergency they would be bailed out. As a result, they can raise funds more cheaply. This is worth way more than the 6 basis points of the levy, so you could argue they are getting off cheaply.

The first half results from Westpac were good in parts, but although declared profit was up, this was thanks mainly to trading income which may not be repeatable, whilst net interest income was down 4 basis points and consumer provisions were higher. Again consumer debt in Western Australia was an issue. The number of consumer properties in possession rose from 261 a year ago to 382 in Mar 17. Investment property 90+ day delinquencies rose from 38 basis points to 47 basis points. They hope the recent mortgage repricing will help to repair their net interest margin in the second half.

We published our top ten post codes with households at risk of mortgage default, and Western Australia came out the worst. In top spot, at number one, is 6210, Mandurah. This also includes suburbs such as Meadow Springs and Dudley Park. Mandurah is a southwest coast suburb, 65 kilometres from Perth. The average home price is around $300,000 and has fallen from $340,000 since 2014. Here there are 1,430 households in mortgage stress but we estimate 388 are at risk of default in the next few months.

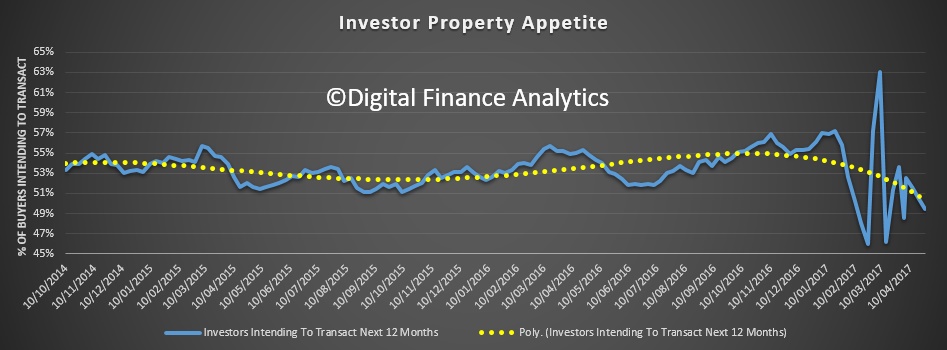

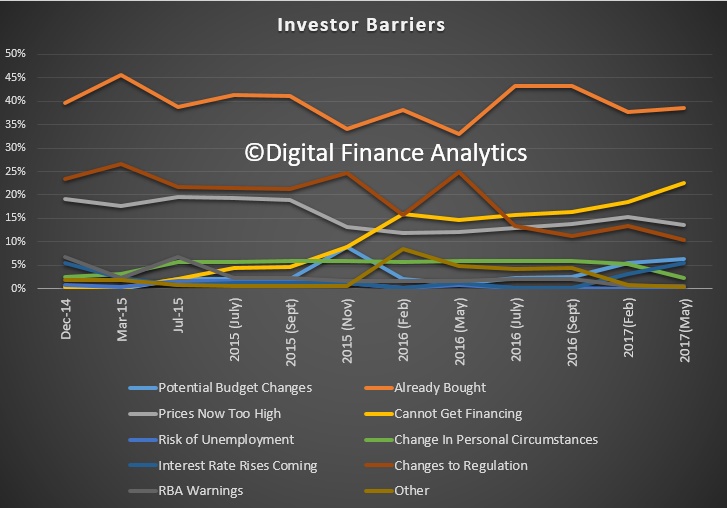

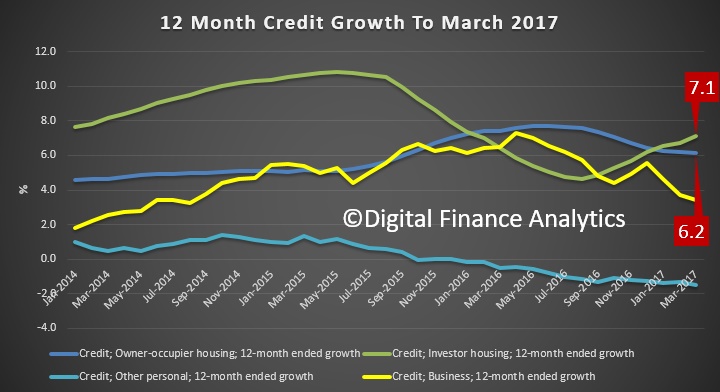

Our surveys also highlighted that financial confidence slipped in April, with investor households a little less confident, and our surveys also showed that less property investors are planning to purchase property in the next 12 months, thanks to the impact of higher mortgage rates and less availability of finance. Our core model suggest that investor loan growth is set to fall from around 7% down to 1 to 2 % in coming months. This will have a profound impact on the property market and the banks.

It may also impact the stamp duty flowing to most states. Data this week highlighted that taxation revenue from housing continued to climb. State and local governments collected about 52% of their total taxation revenue from property, a record which was worth almost $50 billion. So if property momentum does sag, there are significant economic consequences.

And finally back to the budget and its approach to housing affordability. There was a raft of measures announced, some focussing on land release and other supply measures, as well as the option to save for a deposit in a super account tax shelter, and the ability for down-traders to put proceeds back into their super accounts (but no extra tax breaks there). One headline-grabber was the creation of a new entity, the National Housing Finance and Investment Corporation. This will source private funds for on-lending to affordable housing providers to finance rental housing development. However, the bigger issue for the sector remains federal and state funding.

There were very minor tweaks to the negative gearing tax breaks which may adversely hit investors in regional areas, but the perks remain pretty much intact. In fact, if you add up all the measures, we do not think they will fundamentally solve the housing affordability conundrum.

And that’s the Property Imperative Week. Check back next time for more news.

The pick-up in global growth remains on track, with disappointing first-quarter US GDP data offset by better-than-expected numbers in China, and sustained growth in the eurozone and Japan, says Fitch Ratings in its Global Economic Update report.

“Weaker 1Q US growth was explained by consumption and looks to have been affected by temporary factors. Falling unemployment, wealth gains, improved consumer confidence and the prospect of income tax cuts should support a recovery in consumption from 2Q17. In China, the impact of earlier policy stimulus on activity has proved more powerful than anticipated and the slowdown in the housing market has taken longer to materialise than expected,” said Brian Coulton, Fitch’s Chief Economist.

The resilience and breadth of the eurozone recovery continues, with the region posting its eighth consecutive quarter of steady growth at an annual pace of 1.5%-2%.

“Rising bank credit to the private sector and strengthening housing markets suggest accommodative monetary policies are gaining traction in the eurozone, while a mild easing of fiscal policy since 2015 and strong job growth have also helped,” added Coulton.

Fitch expects world growth to rise to 2.9% in 2017 from 2.5% in 2016 and has slightly revised up its 2018 forecast to 3.1% from 3.0% in March. The US growth forecast for 2017 has been revised down slightly but this has been offset by a better outlook for China and Japan.

The Australian Bankers’ Association Chief Executive Anna Bligh has written to the Hon Scott Morrison MP calling on him to immediately release Treasury modelling of the major bank tax.

The letter highlights the severely truncated consultation period and the risk of unintended consequences and seeks individual levy calculations as promised during their earlier meeting with Treasury officials.

Ms Bligh said in order to meet the request by Treasury to comment on the draft legislation, the ABA was seeking further information by 5pm Tuesday 16 May on fundamental aspects of the bank levy, including:

Treasury’s modelling on the economic impacts of the bank levy, including the wider impact on Australian households and businesses.

Treasury’s technical analysis that underpinned the design of the tax, including the coverage of banks and the design of the levy.

Treasury’s modelling including assumptions of the total revenue projections to be collected by the bank levy over the forward estimates.

Ms Bligh said it was no longer acceptable to keep the banks or the Australian community in the dark about a $6.2 billion political tax grab that would have a major impact on all sections of the Australian economy.

“Senior executives of the major banks in good faith attended what they expected to be a comprehensive briefing from Treasury yesterday, only to find to their dismay that Treasury was also in the dark,” she said.

“Fundamental questions about how this tax has been calculated and how the $6.2bn figure was reached have not been answered.

“Yet the Treasurer Mr Morrison continues to maintain that this tax will be ready for implementation by July 1, which is only around six weeks away.

“The Government seems to be putting intolerable pressure on its Treasury officials to meet a ridiculous political timetable,” she said.

“The major banks are terribly concerned about the risk of major unintended consequences of this new tax, and there is an urgent need for more detailed information so we can properly assess its impacts.

“This process is already breaking all the rules and conventions about major taxation implementation, including no prior consultation, no exposure draft legislation for public comment, and an extraordinarily brief timetable before a hastily designed tax is presented to the Parliament.

“Disastrous unintended consequences could flow from this rush,” Ms Bligh said.

OK, I am calling it. Looking at the recent data from our household surveys, property investor appetite is indeed on the decline. Here is the trend chart showing responses in recent weeks.

There were a couple of wobbles, reflecting the heightened speculation about negative gearing and capital gains changes, but there is now a consistent drift lower.

Actually when you look at the root cause of this, it is not so much changes in future expectation of capital growth, it is all to do the availability and price of loans. More than 22% now say they cannot get funding (due to tighter underwriting standards and less access to interest only loans) plus some concerns about future interest rate rises. Concerns about changes in regulation have reduced.

So we expect to see a slowing in the investor credit lending trends. In fact in our core modelling, we are think investor lending could slow to 1-2% p.a. growth ahead. Very different from the trends the RBA showed recently (see below). This would have a significant impact on lenders growth and profitability.

The attitudes of the banks are responsible for the government introducing its surprise bank levy, according to certain political heavyweights.

“I think the banks have set themselves up for this,” John Hewson, former leader of the Federal Liberal Party, said on a panel at a PwC Budget wrap-up event, Prosperity or Peril, held in Sydney on Wednesday (10 May).

“The banks have a very significant social license and a very clear responsibility and they’ve been snubbing their noses at the political system for quite some time.”

The banks had left themselves exposed to this, noting that talk about a Royal Commission and inquiries into the excesses of the banks and the financial system in general had helped persuade the government to take this step.

“There’s a bank bashing mood out there and the government’s got a fertile ground from which to extract some money. You could call it a license fee because they’ve got a very significant privileged position. Our salaries go to them before we even see them,” Hewson said.

The government had plenty of arguments to run with this tax and would get away with it, he predicted. However, the Coalition would have to deal with the fear that this is the thin edge of the wedge and that other sectors could be next.

Also on the panel was former senator for the Australian Labor Party Graeme Richardson who said the banks were the softest target available.

“The arrogance of the banks is extraordinary. If we go back to the GFC, they’ve got that guarantee and that kept them existing,” he said.

“But you’ve got to remember that they’ve thumbed their noses at every government since. They’ve refused to pass interest rate cuts on in full, sometimes at all. And they did so while saying ‘See? You can’t touch us’ and they’ve got that horribly wrong.”

However, he urged the audience to remember one thing about the current bank levy: the banks wouldn’t pay a cent; we would.

“Every bit of that $6bn will finish up being in fees and charges to us so while I can celebrate this morning, I have a feeling over the next few years, they’ll take the smile off my face.”

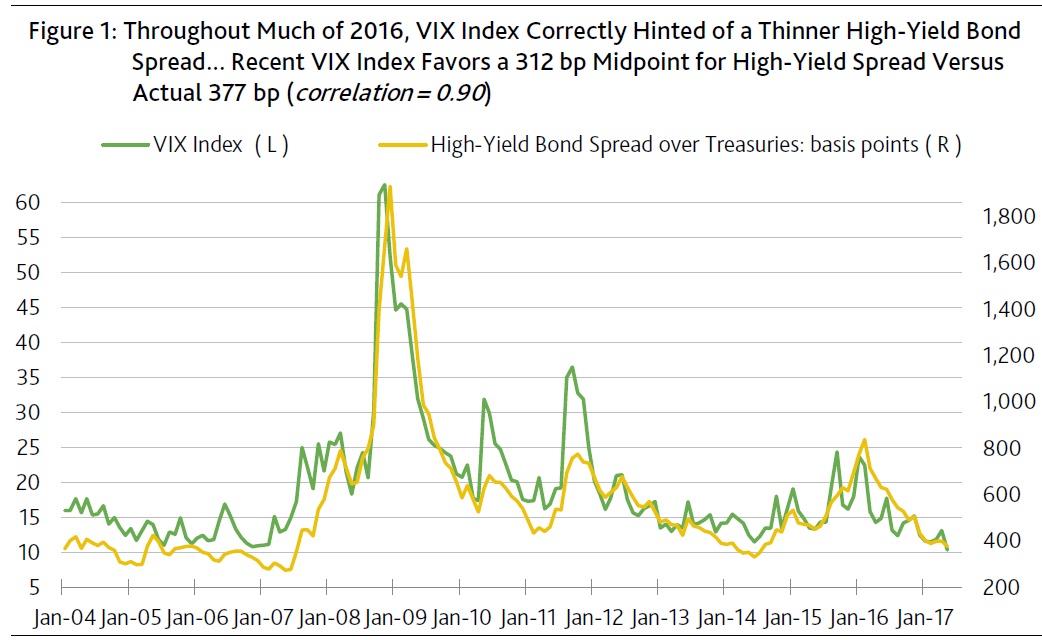

Financial markets were recently visited by a rarity. During the past week, the VIX index closed under 10 points on May 8 and 9. Since its start in 1990, the VIX index has closed under 10 points on only 11, or 0.1%, of the span’s nearly 7,000 trading days.

Today’s very low VIX index reflects a great deal of confidence that there won’t be a deep sell-off by equities. Not only is there effectively little demand for insuring against a harsh correction, but sellers of such insurance are will to accept a low price for protection against a market plunge.

This insouciance seems odd given how richly priced the US equity market is relative to corporate earnings and the prospective returns from other assets such as corporate bonds. The current market value of US common stock — according to a model based on pretax profits from current production and Moody’s long-term Baa industrial company bond yield — exceeds its midpoint valuation by a considerable 24%. During 1999-2000’s memorable equity rally, the market value of US stocks first climbed 24% above its projected midpoint in 1999’s first quarter and would remain at least that high through 2000’s second quarter. During January 1999 through June 2000, the actual market value of US common stock exceeded its projected midpoint by 51%, on average.

Another comparison of the two periods shows a similarly striking difference between them. The earlier period averages of a 15.4:1 ratio for the market value of common stock to pretax operating profits and 8.05% for the long-term industrial company bond yield were far above the recent ratio of 11.7:1 and the latest Baa industrial yield of 4.68%.

In stark contrast to the current situation, during January 1999 through June 2000 the VIX index averaged a substantially higher 24.3 points when the market value of US common stock was at least 24% above its projected midpoint. Back then, the market had a greater appreciation of the considerable downside risk implicit in an overvalued equity market.

Two prior cases of a below-10 VIX index preceded vastly different outcomes

January 2007 and December 1993 were the two prior moments when the VIX index spent some time under the 10-point threshold. What followed them differed drastically.

January 2007 was merely 11 months before the December 2007 start to the worst recession since the Great Depression. In contrast, December 1993 was followed by 1994’s 4.0% annual advance by real GDP that was the first of a seven year span that had real GDP growing by a now unheard of 4.0% annually, on average. Far different was 2007’s 1.8% annual rise by real GDP that was at the start of what would be real GDP’s 0.9% average annual rise of the seven-years-ended 2013.

In the year following December 1993’s ultra-low VIX score, the market value of US common stock fell by -3.2% despite 1994’s 18.6% surge by pretax operating profits. A lift-off by the average 10-year Treasury yield from Q4-1993’s 6.13% to Q4-1994’s 7.96% was to blame for 1994’s short-lived drop by share prices. Nevertheless, partly because of 1994’s very strong showing by business activity, the earnings-sensitive high-yield bond spread narrowed from Q4-1993’s 438 bp to Q4-1994’s 350 bp.

For the year following January 2007’s brief stay by a less than 10-point VIX index, a drop by the 10-year Treasury yield from January 2007’s 4.64% to January 2008’s 4.00% failed to stave off a -3.4% drop by the market value of US common stock largely because of yearlong 2007’s -7.5% contraction of pretax operating profits. A swelling by the high-yield bond spread from January 2007’s 287 bp to January 2008’s 674 bp stemmed from the worsened outlook for business activity.

VIX Index and high-yield EDF differ drastically on yield spreads

May-to-date’s average VIX index of 10.4 points favors a 312 bp midpoint for the high-yield bond spread, which is much thinner than the recent actual spread of 377 bp. Throughout much of 2016, the VIX index proved to be a reliable leading indicator of where the high-yield spread was headed. Nevertheless, if only because the VIX index now resides in the bottom percentile of its historical sample, a higher VIX index is practically inevitable. Once the VIX index approaches its mean, the high-yield spread will be much wider than the recent 377 bp. (Figure 1.)

Mortgages will bear the brunt of the federal government’s new big bank tax, according to one analyst, who believes rate hikes will not be enough to prompt customers to switch lenders.

The surprise levy in Tuesday’s federal budget has widened the rift between government and the banks. All four majors have now publicly slammed the tax, which aims to raise up to $6.2 billion.

ANZ CEO Shayne Elliott labelled the tax a “regrettable policy” and said it is time for Australia’s leaders to “move on from populist bank bashing” and work together with the banking sector to support the national economy.

In a research note, Morningstar analyst David Ellis said that the increase in funding costs to the four major banks and Macquarie will be passed on to borrowers.

“This tax is on all Australian households, with residential borrowers likely to feel the bulk of the burden,” Mr Ellis said.

Morningstar considered the potential impact of further mortgage repricing on customers, who could flock to smaller banks or non-bank lenders.

“We believe the major banks’ strong competitive positions remain firmly entrenched, and collectively, the targeted banks will see little negative impact from customer migration to smaller competitors,” the analyst said.

He added: “The major banks have a long and successful history in coping with profit headwinds, particularly higher funding costs, and we see no difference this time, despite government threats of increased scrutiny on potential mortgage repricing.

“We expect mortgage rates to bear the brunt of future repricing, with interest rates on investor loans likely to be hardest hit.”

Mr Ellis explained that the pricing power of the majors is “alive and well” despite widespread media coverage to the contrary, and stressed that the big four are in no way “on their proverbial knees”.

Morningstar expects the proposed big bank levy to be passed by both houses of parliament.

Australia’s smaller banks have largely supported the initiative. ME chief executive Jamie McPhee said the levy will further “level the playing field”, which the regionals have been calling for since the Murray Inquiry was established in 2013.

“A level playing field is the best means of fostering competition, and producing good value and innovative products into the future.

“Australia’s borrowers and depositors will be the ultimate beneficiaries from a truly competitive environment.”

Morningstar’s Mr Ellis highlighted that while the tax could potentially be positive for the smaller banks, he does not expect any material change to the current competitive position of the banks.

“The changes could lead to greater competition for retail deposits as the major banks increasingly target the levy-free under $250,000 segment, thereby raising the cost of funds for the smaller banks, which are more reliant on this source of funding,” he said.

Under pressure to tackle deepening housing affordability problems, Treasurer Scott Morrison has included various housing policy measures in his budget, some relating to Australia’s small sector of social and affordable housing.

This public funding is the money that, along with tenants’ rents, co-funds state and territory housing and homelessness services. Here too Morrison is proposing reform, particularly to the primary federal-state funding arrangement for social and affordable housing, the National Affordable Housing Agreement (NAHA).

A couple of months ago we suggested the NAHA needed a reboot. Recognising the seriously run-down state of the system, we argued for an increase in funding from its present starvation level. Morrison now proposes a new federal-state funding agreement, the National Housing and Homelessness Agreement (NHHA).

The level of federal funding will be the same as under the old NAHA. But the Commonwealth will press states and territories for action in defined “priority areas”. In effect, this looks like a return to a Canberra-led reform agenda for social and affordable housing unseen since the early Rudd government.

Setting aggregate supply targets

In what appears a significant passage, the budget papers reveal the government’s “priority areas” for the NHHA. We’ll consider these in turn, and then the recurring issue of inadequate funding.

Lack of transparency on the costs incurred by state and territory housing authorities in operating their social housing portfolios has been a particular problem under the NAHA. This is an area where federal engagement is welcome.

All levels of government should be pressed to quantify the level and type of need for housing in the community. And they should be made to set clear “new supply” targets for meeting that need.

That said, the federal government should stop pretending to be shocked at the lack of new social housing delivered by those authorities under the NAHA. The shortfall in NAHA funding has been obvious for years. It simply is too low to bridge the gap between the rents low-income public housing tenants can afford to pay and the costs of properly maintaining the system, let alone growing it to keep pace with rising need.

Residential land development

The stress laid on this issue within the budget policy statement reflects the federal government’s stated concern about “the supply side” of the housing affordability problem. It has framed state government planning controls as an impediment to new housing development.

However, merely loosening requirements and offering existing land owners the prospect of greater development does not ensure it will actually happen.

To ensure land owners don’t just sit on development opportunities speculatively, the federal government should use its NHHA leverage. This could include pushing the states and territories to make greater use of land tax, which would spur development and bring under-utilised land and housing to market.

Inclusionary zoning

Inclusionary zoning is a specific type of planning mechanism. It requires housing developments (above a certain size) to include some proportion of dedicated affordable housing. Ideally, this should be rental housing preserved as “affordable” in perpetuity.

Inclusionary zoning is long established in other countries and has long been demanded by housing advocates in Australia. It is now the subject of increasing interest from planning authorities – for example, the Greater Sydney Commission.

The co-financing arrangements for the NHFIC could incorporate active use of land-use planning powers for inclusionary zoning. Development sites – or developer levy proceeds – could be part of state and territory contributions to funding affordable housing development.

A commitment to build into the NHHA incentives for stepped-up use of inclusionary zoning by state governments is, therefore, very welcome.

However, the budget papers indicate that state compliance with this NHHA expectation might involve not only housing dedicated to affordable rental housing, but also “dedicated first home buyer stock”. This seems to raise the prospect of developers meeting inclusionary zoning requirements simply by reserving some newly built units for first home buyers rather than investors.

The best way to enhance first home buyer prospects vis a vis investor landlords would be to level the playing field by winding back investor negative gearing and capital gains tax concessions, not through this kind of tinkering. And to cast such “FHB reservation” initiatives as in any way equivalent to inclusionary zoning for affordable rental housing would be a highly retrograde step.

Renewing affordable housing stock

An interesting inclusion in the proposed terms of the NHHA is a clause about renewing affordable housing stock.

First, it appears positive in acknowledging the need for a public housing overhaul and indicating a new level of federal government interest in making this happen.

At a minimum, states and territories should be required to undertake a comprehensive audit of their existing portfolios. The level of outstanding disrepair has to be costed. They also should identify where renewal can best take place, balancing need for expanded and upgraded housing with sensitive treatment of existing communities.

Second, it indicates federal backing for further transfers of public housing as a growth path for the affordable housing industry. However, as our recent research for AHURI shows, this is feasible only if the operating cost gap is funded.

Past community housing growth through transfers, particularly following the 2009 housing ministers’ commitment to expand community housing to 35% of all social housing, involved an understanding that Commonwealth Rent Assistance, paid through Centrelink to transferred tenants, would help cover that gap.

Without additional funding in the NHHA, a new phase of growth through transfers requires a recommitment by governments to use rent assistance as an effective operational subsidy to community housing providers. A new target and timeframe to replace the 35% benchmark also need to be considered.

Homelessness services

Previously the subject of a separate funding agreement (the National Partnership Agreement on Homelessness), homelessness services have struggled for years in the face of that agreement’s pending expiry and short-term extensions.

The NHHA will fund homelessness services on an ongoing basis, which the sector has welcomed.

Funding shortfall remains

As we’ve indicated throughout, the objectives of the NHHA – and of the social and affordable housing system generally – will continue to run up against the reality that decent housing of this kind costs more than low-income households can afford to pay.

This applies especially to people living on the miserable level of benefits such as Newstart. A subsidy is required, both to build up the stock and to keep it in good order.

Clearer targets, more transparent cost accounting, and innovations like NHFIC finance won’t bridge the gap. On the contrary, to successfully use those initiatives to build more stock, both state and territory housing authorities and non-government affordable housing providers need a larger subsidy than present funding provides.

The budget has indexed NHHA funding to wages. It would be nice to think that land and housing prices will increase only in line with wages.

In reality, properly funding the growth and maintenance of our social and affordable housing stock will require more than what the federal government is offering.

Authors: Chris Martin, Research Fellow, Housing Policy and Practice, UNSW; Hal Pawson, Associate Director – City Futures – Urban Policy and Strategy, City Futures Research Centre, Housing Policy and Practice, UNSW