Australia’s slowness to offer open data leaves the country’s banking sector open to an incursion from more competitive foreign companies, according to Tyro Payments.

Speaking to members of the French-Australian Chamber of Commerce on Wednesday, 3 May, Tyro Payments executive director Jost Stollmann said that globally, banking is on the cusp of transformation.

“Transformations happen in windows, if you miss the window it’s gone, and I see that now the window of digital transformation opens in those business places that are more complicated and tend to be more regulated,” he said.

“I personally think that banking is ripe for disruption.”

Mr Stollmann said there are three ways this disruption could play out; the major banks could reinvent and disrupt themselves, innovative start-ups could come through to challenge the incumbent players, or data aggregators such as Alibaba’s Ant Financial could become the dominant force in financial services.

The primary challenge facing Australia’s banking sector at present is that it is “hopelessly far behind” its international peers when it comes to the availability of open data and open APIs, Mr Stollmann said, noting that the country is “at risk of losing the opportunity” to innovate and become more competitive.

“The productivity commission has tabled its report to the government and it’s nice, and they’ve discovered that open data has benefits for the community and we need it, which is all heading in the right direction, but it falls completely short in terms of scope,” he said.

“It’s really a problem; you compare this with the UK, the UK went through the global financial crisis and they do not have a high regard for their banks, so the government and the regulator are very keen to open up banking for competition.”

Mr Stollmann added that the European Commission has mandated that European banks must deliver open data from January 2018.

“That’s less than a year away. You can imagine that the European banks have screamed that this was the end of the world but they’ve moved on,” he said.

“Now that it’s mandated, it has unleashed investment into the space, and in my view there’s going to be a revolution in banking.”

The shift to an open data economy in Australia is critical to the ongoing competitiveness of the country’s banks, Mr Stollmann said, cautioning that without an open data economy to provide a “level playing field” for start-ups, the sector will suffer.

“If we don’t get our act together and move fast, the major banks will have a problem because they don’t know how to compete, the fintechs will have a problem scaling up and the foreign colonisers will win,” he said.

“The foreign giants will colonise – it’s nothing new, we’ve seen it in media and advertising, maybe we’ll see it now in commerce.”

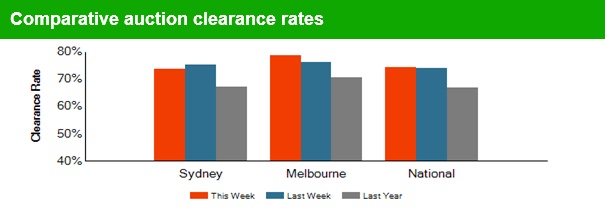

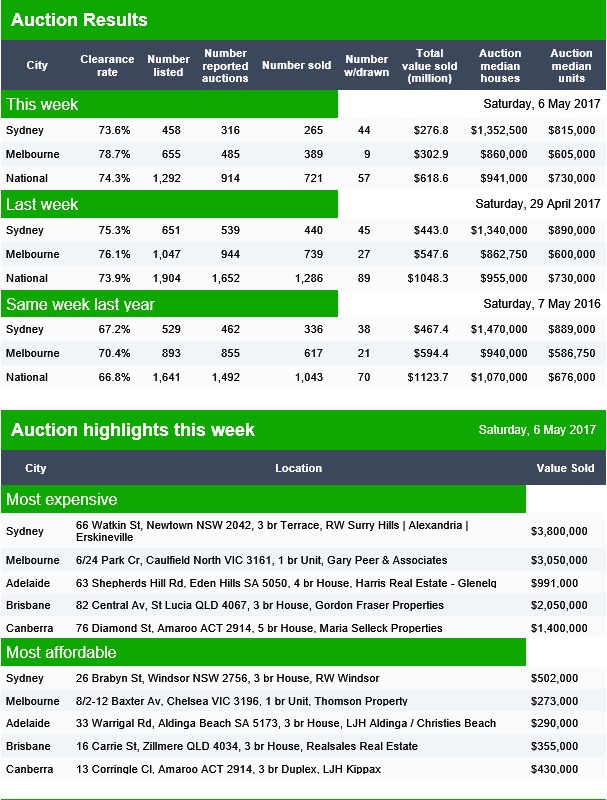

The preliminary data from Domain shows that the number of listings are down, though clearance rates are still quite high. Nationally, 721 properties were sold, compared with 1,286 last week and 1,043 a year ago. Looks like momentum is indeed easing.

This equates to a 74.3% clearance compared with 73.9% last week and 66.8% a year ago. Sydney achieved 265, at 73.6% compared with 539 at 75.3% last week, and Melbourne sold 721, compared with 1,286 last week, at 78.7% this week and 76.1% last week.

Brisbane cleared 55% of 69 listings, Adelaide 62% of 74 listings and Canberra 55% of 36 listed.

The latest edition of our weekly summary of events in the finance and property industry has been released, a week in which the RBA told us more about household finances, major banks reported lifts in delinquencies and the number of households in mortgage stress continued to rise.

You can watch our video summary.

We start our review of the week by looking at data from the RBA. They held the cash rate again, and in a speech Governor Philip Lowe said the bank is not overly concerned that a “severe correction in property prices” would trigger a banking collapse, as happened in the US in 2008-09. However, he was far more worried that Australians would bring the economy to a grinding halt by curbing their spending. He said Household debt is “high” relative to incomes, making it likely that many Australians would respond to a market correction with a “sharp correction in their spending”, in an attempt to pay down debt. As a result, an otherwise manageable downturn could be turned into something more serious.

He also made the point that allowing young Australians to use their superannuation for a deposit will not assist affordability and downplayed the importance of tax policies. “The best housing policy is really a transport policy,” he said during a question-and-answer session. The latest RBA chart showed household debt rose again.

The Quarterly Monetary statement highlighted the risks from low income growth, although the underlying causes are not that clear, and that the Bank is still relatively optimistic about future growth. However, again the theme of high household debt came to the fore with data showing that one third of households had no mortgage repayment buffer. It’s worth saying this data comes from securitised loans which may be regarded as the cream of the crop, so risks in other portfolios may be higher.

We have several results in the week, with impressive full year numbers from Macquarie; but less impressive results from NAB, ANZ and Genworth, the Lenders Mortgage Insurer. From this we learnt that delinquencies are rising, especially in the mining heavy states of WA and QLD. Genworth in particular reported a rise in claims. Whilst tighter lending rules are lower the LVR bands, heightened risks seem to be baked in. Yellow Brick Road, who also reported, highlighted the impact of recent regulatory tightening on the mortgage sector.

We also saw how the retail banks net interest margins are under pressure, this despite recent mortgage rate rises, and hikes to the small business sector, which is the soft underbelly of the portfolio when banks seek to recover NIM. NIM is being hit by the higher capital requirements which are being imposed on the banks. This suggests that more out of cycle rate rises are likely, despite the fact that funding costs appear to have stabilised.

According to the HIA, new home sales fell slightly in March down 1.1% mainly due to fall in new houses; but there were significant state variations, with NSW the only state to record an increase in detached house sales, posting a 10.4 per cent rebound after a soft result in February. Detached house sales fell by 4.6 per cent in Victoria, by 5.4 per cent in Queensland and fell in South Australia and Western Australia by 1.7 per cent and 1.2 per cent respectively.

We released the latest mortgage stress report, which showed of the 3.1 million mortgaged households, an estimated 767,000 are now experiencing mortgage stress. This is a 1.5% rise from the previous month and maintains the trends we have observed in the past 12 months. The rise can be traced to continued static incomes, rising costs of living, and more underemployment; whilst mortgage interest rates have risen thanks to out-of-cycle adjustments by the banks and bigger mortgages thanks to rising home prices.

We think the affordability calculations the banks use need to be reviewed, and the regulators need to do more to get to the bottom of the continuing reclassification of loans between owner occupied and investment – more than $51 billion have been switched, which is around 10 per cent of all investor loans.

Next week we will publish our stress by post code data, and the latest household finance confidence index.

The speculation around whether Sydney home prices are wobbling continues, with the latest CoreLogic numbers flagging a potential fall. But one swallow does not make a summer, and we will need to see more data. Remember there are technical issues behind the CoreLogic index. Auction clearance rates were relatively good, but on lower volumes. We will see what today’s results deliver.

Finally, we expect more discussion on the future shape of capital requirements for the banks, with the Reserve Bank of New Zealand announcing it is undertaking a comprehensive review of the capital adequacy framework applying to locally incorporated registered banks over 2017/18. The aim of the review is to identify the most appropriate framework for setting capital requirements for New Zealand banks, taking into account how the current framework has operated and international developments in bank capital requirements.

In the UK, the Bank of England released details of their approach to setting MREL (a minimum requirement for own funds and eligible liabilities) for UK banks, building societies and the large investment firms. These rules represent one of the last pillars of post-crisis reforms designed to make banks safer and more resilient, and to avoid taxpayer bailouts in future.

Banks are now required to hold several times more loss-absorbing resources than they did before the crisis, while annual stress tests check firms’ resilience to severe but plausible shocks. Banks are now also structured in a way that supports resolution and The Bank of England has the legal powers necessary to manage the failure of a bank, and significant progress has been made to ensure there is coordination between national authorities should a large international bank fail.

We are expecting APRA to release a discussion paper on capital rule tweaks to ensure our banks are unquestionably strong later in the year. This all signals potential higher interest rates for consumers and small business down the track, as more capital is costly.

He argued that competition law and the work of the ACCC is essential to maintaining faith in Australia’s free market system. He also highlights that penalties actually imposed here in Australia are stunningly lower than those in other comparable jurisdictions.

It is an important time to be talking about competition. Competition law and policy are essential underpinnings of our free market economy. We are, however, in the midst of a crisis of faith in free markets which should, and I know does, worry us all. Today I want to make four points, as follows.

First, I will briefly outline the loss of faith in the free markets and why this should concern us all

Second, I will briefly discuss how some prominent economists have seen the role of competition policy and law in our market economy through time, and today

Third, I will explain why effective enforcement of the Competition and Consumer Act (CCA) is so important to people having faith in free markets, and

Fourth, I will suggest how we can improve the effectiveness of the CCA, particularly through higher penalties for competition law breaches.

Of specific interest was his comments on the low typical fines imposed on corporates, such that there may be little financial incentive to do the right thing.

The ACCC is very concerned that penalties imposed by Australian Courts in both competition and consumer cases historically have not been sufficiently high to deter contraventions, particularly in cases involving larger businesses.

On the consumer side, the ACCC strongly welcomes the current Australian Consumer Law Review. This review acknowledges that the maximum penalties for breaches of consumer law are inadequate. They are too low to provide a powerful deterrent effect, and this is particularly the case for breaches by large corporate players that are unlikely to be deterred by a maximum penalty of $1.1 million per contravention.

The ACL Review recommends that the ACL penalties be comparable to competition law penalties that also operate across the economy. There appears to be no policy reason for the maximum penalties under the ACL being lower than those available for breaches of competition laws.

As one example, we were pleased late last year when Nurofen maker, Reckitt Benckiser, had its penalty increased by the appeal court from $1.75 million to $6 million, after it was found that the original penalty could not be viewed as substantial or as achieving deterrence.

The Court held that the penalty imposed by the first instance judge of $1.75 million was “manifestly inadequate”, and that a penalty at that level “would reinforce a view that the price to be paid for the contraventions was an acceptable business strategy, and was no more than a cost of doing business.”

Perhaps had competition law penalties been available to the court we could have seen a penalty many times higher than the amount awarded to act as specific deterrents to large, multinational companies such as Reckitt Benckiser.

I suggest, although we have no way of knowing, that the vast majority of Australians would consider a $60 million penalty more appropriate as a specific deterrent for Reckitt Benckiser, which is a large multinational company.

Turning now to competition law, we have a very different story. The penalties available in Australia are broadly in line with international trends. However, penalties actually imposed here in Australia are stunningly lower than those in other comparable jurisdictions.

The key reason for this is that Australian competition law penalties were only brought into line with those overseas in 2009. From that date Australian courts now have been able to impose penalties of up to 10% of turnover where, as is usual, the benefits obtained from the illegal activity cannot be calculated.

For a company that, say, has an Australian turnover of $1 billion, the maximum penalty per contravention can now be $100 million, rather than $10 million as it was before this change was introduced in 2009.

While we are only now encountering cases where the relevant behavior occurred post 2009, the Parliament has clearly spoken. It now wants higher competition penalties as, I suspect, does the average Australian.

As with the Nurofen case in consumer law, the courts also seem to be focusing on the level of deterrence required. In his judgment on our proceedings against ANZ Bank and Macquarie Bank last December, Justice Wigney expressed reservations about the amount of the penalty that was by agreement jointly submitted to the court.

He said that the penalties were “at the very bottom of the range of agreed penalties” and that he would have ordered a much higher penalty had there been no agreed penalty. He also said:

“A very sizable penalty is plainly required to deter a financial institution of the size of ANZ from engaging in such conduct again. Equally, a very sizeable penalty is required to deter institutions in positions similar to ANZ who might be tempted to engage in similar contravening conduct”.

Clearly the size of the company does matter when having regard to the level of penalty required to achieve specific and general deterrence.

The ACCC has been for some time giving this issue careful thought. In particular we have had regard to the way in which other countries quantify their penalties in order to achieve deterrence.

In December 2016, for example, Australia participated in a Global Forum on competition hosted by the OECD. A key issue discussed was sanctions in competition cases. The research revealed that most other OECD jurisdictions, including the US, UK and the EU have very transparent methodologies for determining penalties.

In the United States, Europe and the UK the methodology used to determine penalties includes the calculation of a ‘base fine’. This is usually done by reference to a set percentage (between 10% and 30%) of the relevant turnover of the business being penalised. The turnover figure is often the turnover of the firm in the jurisdiction concerned but sometimes it is the relevant global turnover of the firm.

Commonly once the base fine is calculated, it is increased having regard to duration of the conduct and numbers of contraventions, and other aggravating factors. Mitigating factors are then applied which reduce the fine before a final figure is determined.

An important difference between our approach and that of other overseas jurisdictions is that our Courts do not start the exercise of determining penalties by calculating a base figure calculated by reference to turnover of the firm.

If the base penalty approach was applied in Australia, firms with smaller turnover might end up with similar fines to those currently imposed, but importantly firms with substantially larger turnovers would generally end up with much higher penalties.

As an example, Professor Caron Beaton-Wells of the University of Melbourne has used the USA methodology to calculate that in the Visy case, instead of the penalty of $33m imposed then by the Court, the starting figure would have been $212 million, with potential to increase above that level. Under the EC’s 2006 Guidelines, Visy’s base figure would have been even higher.

In the ACCC’s view, penalties imposed under the CCA need to be many times higher than they are now to have a sufficient deterrent effect on larger firms. The current ACL Review has recommended such higher penalties for consumer law breaches; and we, the ACCC, must work with the courts to give effect to Parliament’s clear intention of a step change in penalties for competition law breaches by larger companies.

Encouraging senior Australians to downsize their homes is one of the more popular ideas to make housing more affordable. The trouble is, incentives for downsizing would hit the budget, but make little difference to housing affordability.

It sounds good: new incentives would encourage seniors to move to housing that better suits their needs, while freeing up equity for their retirement and larger homes for younger families.

But the reality is different. Research shows most seniors are emotionally attached to their home and neighbourhood and don’t want to downsize.

When people do downsize, financial incentives are generally not the big things on their minds. And so most of the budget’s financial incentives will go to those who were going to downsize anyway.

Financial barriers to downsizing

There are three financial hurdles to downsizing. Downsizers risk losing some or all of their Age Pension, because the family home is exempt from the pension assets test, but any home equity unlocked by downsizing is not.

Downsizers also have to stump up the stamp duty on any new home they buy. For a senior purchasing the median-priced home in Sydney that’s now A$32,000. Finally earnings from the cash released are taxed, whereas capital gains on the home are not.

The Turnbull government has flagged the possibility of financial incentives in next week’s federal budget for superannuants and pensioners to downsize their home.

One proposal would exempt downsizers from the A$1.6 million cap on super balances eligible for tax-free earnings in retirement, or from the A$100,000 annual cap on post-tax contributions. But this would benefit only the very wealthiest retirees – just 60,000 retirees have super fund balances exceeding A$1.6 million.

More seniors would benefit from a proposal to exempt them from stamp duty when purchasing a smaller home. And many would benefit from a Property Council proposal to quarantine some portion of the proceeds from the pension assets test for up to a decade.

The trouble with all these proposals is that they would hit the budget – because everyone who downsized would get the benefits – but they would not encourage many more seniors to downsize.

Staying – or downsizing – is seldom about the money

Research shows that for two-thirds of older Australians, the desire to “age in place” is the most important reason for not selling the family home. Often they stay put because they can’t find suitable housing in the same local area.

In established suburbs where many seniors live, there are relatively few smaller dwellings because planning laws restrict subdivision. And even if the new house is next door, there’s an emotional cost to leaving a long-standing home, and to packing and moving.

And so, few older Australians downsize their home. According to the Productivity Commission, about 20% aged 60 or over have sold their home and purchased a less expensive one since turning 50. Another 15% have “strong intentions” to do so in the future.

When older Australians do downsize, their decision is dominated by non-financial considerations, such as a preference for a different style of house and living, a concern that it is getting too hard to maintain the house and garden, or the loss of a partner.

These emotional factors typically dwarf financial considerations. According to surveys, no more than 15% of downsizers are motivated by financial gain. Stamp duty costs were a barrier for only about 5% of those thinking of downsizing. Only 1% of seniors listed the impact on their pension as their main reason for not downsizing.

There are better and cheaper ways to encourage seniors to downsize

If governments do want to use financial incentives to encourage downsizing, budget sticks would be cheaper and fairer than budget carrots. Even if they have little effect on downsizing rates, at least they would contribute to much-needed budget repair and economic growth.

The federal government should include the value of the family home above some threshold – such as A$500,000 – in the Age Pension assets test. This would encourage a few more seniors to downsize. More importantly, it would make pension arrangements fairer, and contribute up to A$7 billion a year to the budget.

Asset-rich, income-poor retirees could continue to receive a full pension by borrowing against the value of the home until the house is sold. The federal government would then recover the cost from the proceeds of the sale. If well designed, this scheme would have almost no effect on retirees – instead it would primarily reduce inheritances.

State governments should abolish stamp duties on property, and replace them with a general property tax, as the ACT Government is doing. This would encourage downsizing, although only at the margins.

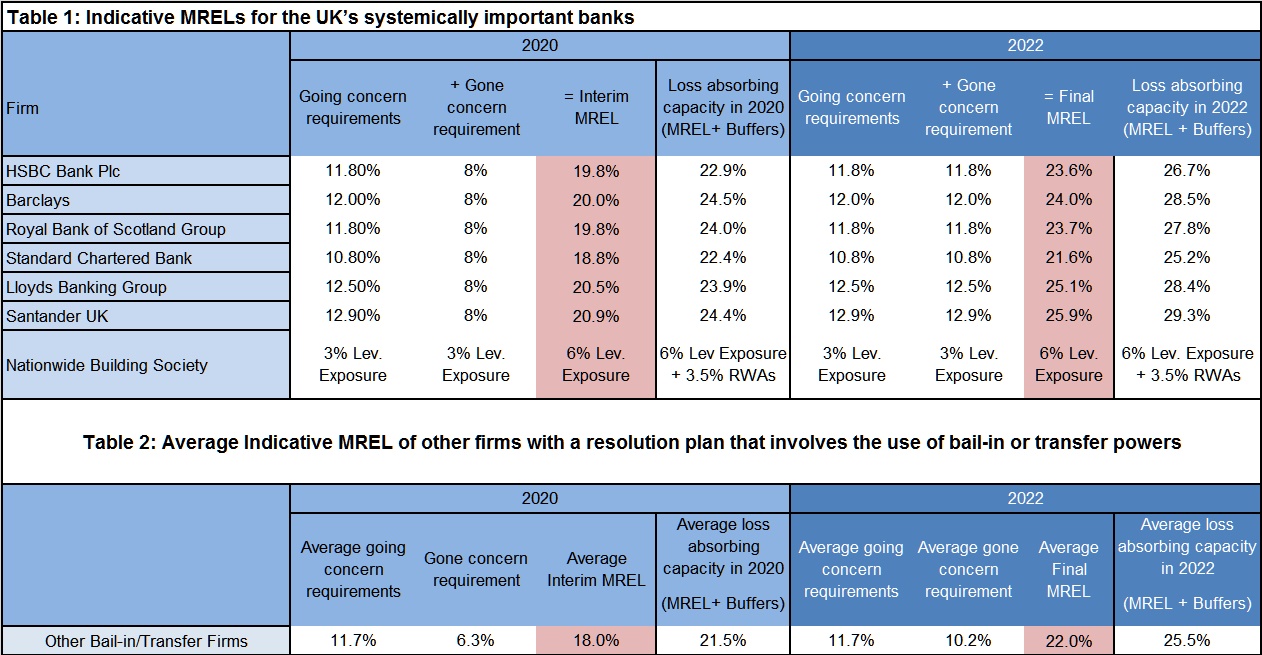

Given the current debate about “Unquestionably strong” banks, it is worth reading the Bank of England’s approach to minimum loss-absorbing capacity these institutions must hold, and how it can comprise both ‘going concern’ and ‘gone concern’ resources.

These rules represent one of the last pillars of post-crisis reforms designed to make banks safer and more resilient, and to avoid taxpayer bailouts in future. Banks are now required to hold several times more loss-absorbing resources than they did before the crisis, while annual stress tests check firms’ resilience to severe but plausible shocks. Banks are now also structured in a way that supports resolution. The Bank of England now has the legal powers necessary to manage the failure of a bank, and significant progress has been made to ensure there is coordination between national authorities should a large international bank fail.

The new rules will be introduced in two phases. Banks will be obliged to comply with interim requirements by 2020. From 1 January 2022, the largest UK banks will hold sufficient resources to allow the Bank of England to resolve them in an orderly way.

What is MREL?

MREL is a critical part of a resolution strategy. It determines the minimum loss-absorbing capacity these institutions must hold, and it can comprise both ‘going concern’ and ‘gone concern’ resources.

Going-concern resources, typically in the form of common equity, absorb losses in times of stress and ensure that a bank can keep operating and that it can maintain the supply of credit to the economy.

Gone-concern resources, typically in the form of debt, absorb losses when a bank undergoes resolution or is placed into insolvency.

Smaller institutions that provide banking activities of a scale that means that they can be allowed to go into insolvency if they fail, will satisfy MREL by simply meeting their minimum regulatory capital requirements as a going concern. There is no gone-concern requirement for these firms. More detail on the capital framework for bank capital is set out in the Supplement to the December 2015 Financial Stability Report.

But larger banks and building societies with a size or functions that mean they have a resolution plan involving the use of the Bank’s resolution tools will be required to hold additional MREL beyond their going-concern requirements.

In addition, firms are expected to hold going-concern capital buffers on top of these requirements. The buffers are calibrated to recognise systemic importance or idiosyncratic exposures, and are intended to be used so that banks can absorb losses without breaching minimum requirements. As these capital buffers are not permitted to count towards meeting MREL, they add to the total loss-absorbing capacity of each bank.

How much MREL must larger firms hold?

The MREL for large firms is needed in a resolution both to absorb losses and to recapitalise their continuing business. Our policy is that from 1 January 2022 they should be required to hold both their going-concern requirements together with additional MREL of an amount equal to those going concern requirements. In other words, their MREL will be two times their going-concern requirements.

These UK firms will become subject to interim requirements on 1 January 2020, prior to the final requirements coming into force in 2022. We will review our approach to calibration of the 2022 MREL for all firms before the end of 2020, before we set final MRELs. In doing so, we will have particular regard to any intervening changes in the UK regulatory framework, as well as institutions’ experience in issuing liabilities to meet their interim MRELs.

Table 1 below provides the estimates of the interim and final consolidated MREL requirements that we have sent to each of the UK’s global and domestic systemically important banks. As a firm’s MREL will depend upon its going concern requirements in a particular year, these 2020 and 2022 MRELs are simply indicative and are based on the calibration methodology set out in our Statement of Policy, with reference to the firms’ minimum capital requirements and balance sheets as at December 2016.

In addition to the global and domestic systemically important UK banks, there are eight other UK banks and building societies that currently have a resolution plan that involves the use of resolution tools by the Bank (rather than reliance on the insolvency regime). These are:

Clydesdale Bank

The Co-operative Bank

Coventry Building Society

Metro Bank

Skipton Building Society

Tesco Bank

Virgin Money

Yorkshire Building Society.

Table 2 provides the average of the indicative 2020 and 2022 MRELs and total requirements for these other firms.

We have provided an average for these firms as publishing MRELs for each of them would also reveal the firm-specific element of their capital assessments, many of which have not previously been disclosed. Accordingly, the Prudential Regulation Authority will consider its disclosure policy and undertake the appropriate consultations before a final decision on publishing individual MRELs for these firms is taken.

The Co-operative Bank has been excluded from the calculation of the average because the firm is currently seeking a sale, which has the potential to significantly affect The Co-operative Bank’s balance sheet. Therefore an indicative MREL based on The Co-op’s balance sheet today may not be a useful guide to the eventual requirement.

Quarterly earnings generally improved for U.S. banks in the first quarter of 2017, but loan growth came to a halt and loan losses are likely to increase over the near to medium term, according to Fitch Ratings’ U.S. Banking Quarterly Comment. Provision expenses for the 18 largest U.S. banks covered in the report rose 8% in 1Q17 from 4Q16 and loan losses in nominal terms increased on a linked-quarter basis. Growing concern in asset quality, particularly in credit cards, auto, and retail loan exposure from the disruption of e-commerce could contribute to increased loan losses going forward.

“Better capital markets results, lower taxes from new accounting guidance and modest improvement in spread income boosted earnings for the majority of U.S. banks, however, loan growth came to a standstill, expenses and credit costs climbed and mortgage revenue slowed during the quarter,” said Julie Solar, Senior Director, Fitch Ratings.

Overall industry-wide loan balances declined 2.5% on an annualized basis. For the large U.S. banks, this trend was less pronounced, with total loans down approximately 0.8% on an annualized basis. Pay-downs in energy credits, large corporate borrowers accessing the capital markets, discipline in maintaining risk-adjusted returns, and seasonally lower credit card balances all contributed to the decline in loans. Many borrowers are also waiting for more definitive policies from Washington despite improving business optimism before borrowing.

“Looking ahead, loan growth will be dependent on continued economic growth and will vary by loan category particularly with concerns in auto and signs that banks are demonstrating greater commercial lending discipline,” said Joo-Yung Lee, Managing Director, Fitch Ratings.

Twelve of the 18 banks reported higher net income in 1Q17 than in 4Q16 and several banks reported increases in net interest margins (NIM) including M&T Bank, Bank of America, Fifth Third Bancorp, and BB&T. The better NIM is largely due to the December 2016 interest rate increase as the March rate rise came too late in the quarter to materially impact the results. Capital markets results for the five large global trading and universal banks increased 19% in aggregate from 1Q16, with most of the improvement in equity and debt underwriting, up 92% and 51%, respectively, from the prior year.

In addition, several banks benefited from one-time tax benefits from the adoption of new stock-based compensation guidance. Goldman Sachs saw a large benefit witch the change accounting for 21% of its income. The new guidance is expected in impact first quarter results going forward.

Bank capital ratios remain solid with a median CET1 of 10.8% at March 31, 2017. Commentary from banks indicates that capital distributions will increase across the industry.

High household debt and further strong house-price gains are fuelling Australian investor’s concerns around a domestic housing-market downturn, according to Fitch Ratings’ latest survey of the country’s fixed-income investors. Investors also believe developments in the Eurozone now pose a greater risk to Australian credit markets than a China hard landing.

The 2Q17 survey was undertaken in partnership with KangaNews – a specialist publishing house that provides commentary on fixed-income markets in Australia and New Zealand. Findings represent the views of managers of more than AUD300 billion of fixed-income assets, accounting for over three-quarters of Australia’s domestic real-money market.

Australia is facing mildly tougher economic conditions according to fixed-income investors. Their outlook for three key economic indicators suggests the next three years will see modest interest rate increases, a drift to slightly higher unemployment and house price declines. Interestingly, 60% of investors expect house prices to rise by between 2% and 10% by end-2017, while 52% expect house prices to decline by between 2% and 10% by end-2019.

Investors believe banks are better placed to manage risks, despite their less-than-rosy economic outlook, following steps taken to strengthen bank balance sheets and tighten lending standards. Property market exposure remains investors’ key concern, but the proportion ranking it as ‘critical’ has dropped to 30%, from 43% in our previous 4Q16 survey.

Corporate Australia’s credit profile is also expected to strengthen, with more investors taking the view that corporates will deleverage. The proportion of investors expecting corporate leverage to decrease has risen to 23%, from 4%, over the three surveys conducted over the past twelve months. Investors have nominated the corporate asset class as their preferred investment choice.

Australian investors anticipate a strong rebound in structured finance RMBS and ABS issuance over the next 12 months. Fifty-eight percent believe there will be increased issuance in 2017, up from just 16% in our 4Q16 survey.

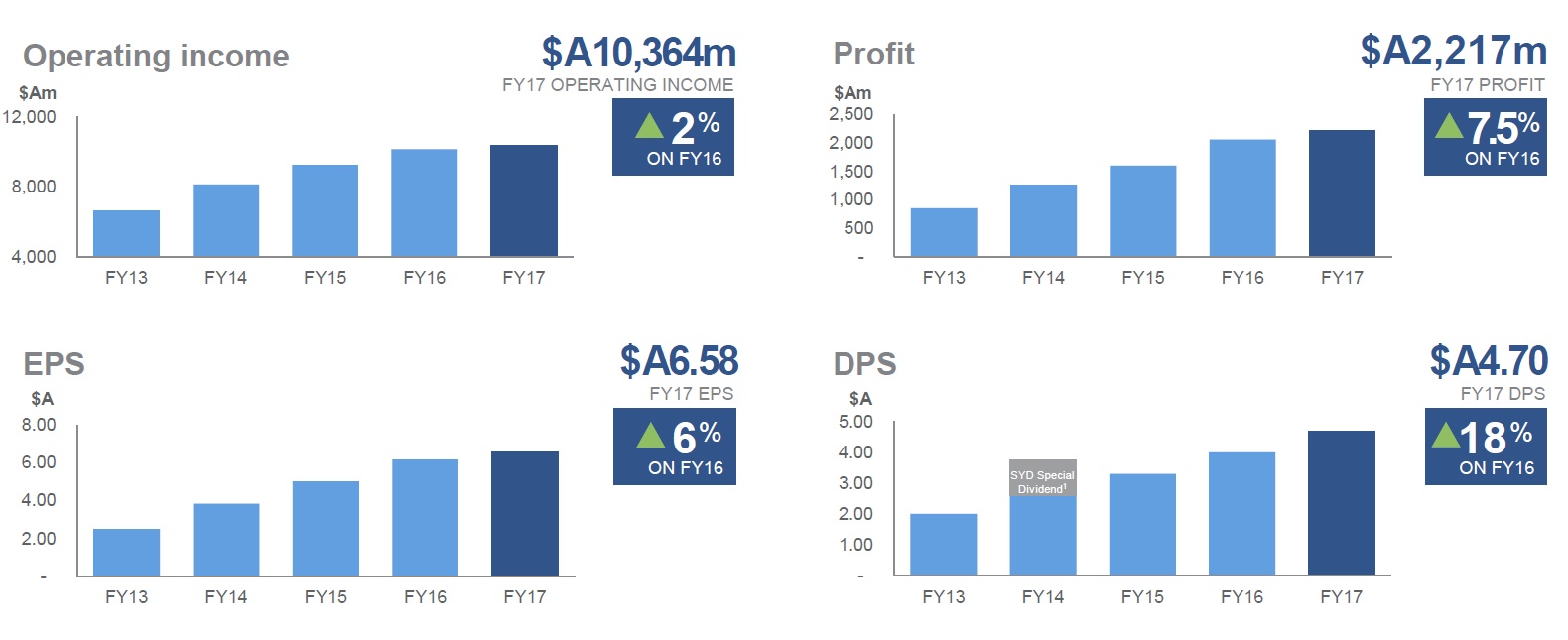

Macquarie Group has announced a net profit after tax attributable to ordinary shareholders of $A2,217 million for the full year ended 31 March 2017 (FY17), up 7.5 per cent on the full year ended 31 March 2016 (FY16).

Profit for the half-year ended 31 March 2017 (2H17) was $A1,167 million, up 11 per cent on the half-year ended 30 September 2016 (1H17) and up 18 per cent on the half-year ended 31 March 2016 (2H16).

There was a nine per cent decrease in combined net interest and trading income to $A3,954 million, an 11 per cent decrease in fee and commission income to $A4,331 million, a five per cent increase in net operating lease income to $A921 million, whilst other operating income and charges of $A1,107 million in FY17 increased significantly from $A66 million in FY16. The primary drivers were increased gains on the sale of investments and businesses; and lower charges for provisions and impairments across most operating groups. Total operating expenses increased two per cent whilst staff numbers were down.

Macquarie Group Managing Director and Chief Executive Officer (CEO) Nicholas Moore said: “Macquarie’s annuity-style businesses (Macquarie Asset Management (MAM), Corporate and Asset Finance (CAF) and Banking and Financial Services (BFS)), which represent approximately 70 per cent of the Group’s performance5, continued to perform well, with combined net profit contribution of $A3,249 million, up four per cent on FY16.

“Macquarie’s capital markets facing businesses (Commodities and Global Markets (CGM) and Macquarie Capital) also performed well with a combined net profit contribution of $A1,454 million, up 12 per cent on FY16.”

Net operating income of $A10,364 million in FY17 was up two per cent on FY16, while operating expenses of $A7,260 million were also up two per cent on FY16.

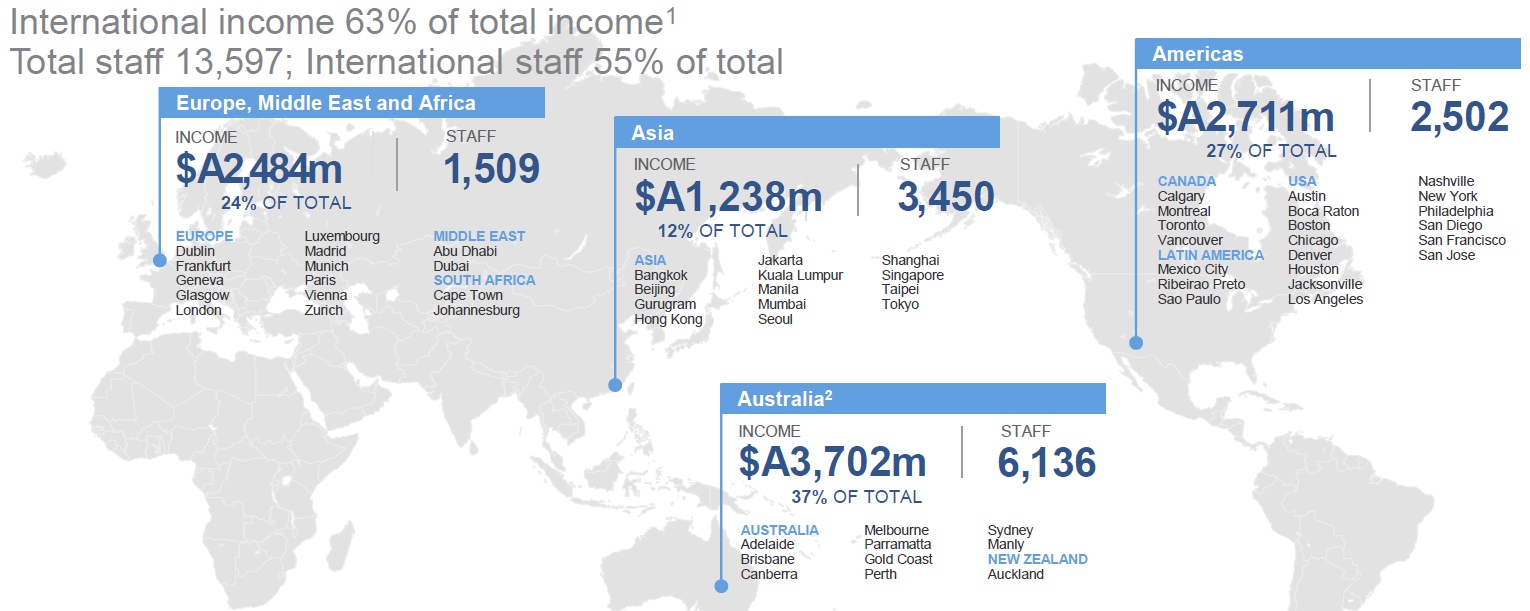

While Macquarie continued to build on the strength of its Australian franchise, its international income accounted for 63 per cent of the Group’s total income for FY17. Total international income was $A6,433 million in FY17, a decrease of five per cent on FY16.

Macquarie’s assets under management (AUM) at 31 March 2017 were $A481.7 billion, broadly in line with $A478.6 billion at 31 March 2016, due to favourable market movements and additional fund investments in Macquarie Infrastructure and Real Assets (MIRA), partially offset by a decrease in insurance assets and unfavourable foreign exchange movements.

Macquarie announced a 2H17 final ordinary dividend of $A2.80 per share (45 per cent franked), up from the 1H17 interim ordinary dividend of $A1.90 per share (45 per cent franked) and up from the 2H16 final ordinary dividend of $A2.40 per share (40% franked). The total ordinary dividend payment for the year of $A4.70 per share, is up from $A4.00 in the prior year. This represents an annual ordinary dividend payout ratio of 72 per cent. The record date for the final ordinary dividend is 17 May 2017 and the payment date is 3 July 2017.

Macquarie currently expects the year ending 31 March 2018 (FY18) combined net profit contribution from operating groups to be broadly in line with the year ended 31 March 2017 (FY17). The FY18 tax rate is currently expected to be broadly in line with FY17. Accordingly, the Group’s result for FY18 is currently expected to be broadly in line with FY17.

Operating group performance

Macquarie Asset Management delivered a net profit contribution of $A1,538 million for FY17, down six per cent from $A1,644 million in FY16. FY17 base fees of $A1,574 million were broadly in line with FY16. Base fee income benefited from investments made by MIRA-managed funds, growth in the MSIS Infrastructure Debt business and positive market movements in MIM AUM, largely offset by asset realisations by MIRA-managed funds, net AUM outflows in the MIM business and foreign exchange impacts. Performance fee income of $A264 million, predominately from infrastructure assets, was down from a particularly strong $A693 million in FY16. Investment-related income included principal gains from the partial sale of MIRA’s holdings in MQA and MIC, the sale of the trustee-manager of APTT as well as the sale of unlisted real estate and infrastructure holdings. Assets under management of $A480.0 billion were broadly in line with 31 March 2016.

Corporate and Asset Finance delivered a net profit contribution of $A1,198 million for FY17, up six per cent from $A1,130 million in FY16. The increase reflected the full year contribution of the AWAS and Esanda acquisitions as well as lower provisions for impairment, partially offset by the impact of lower loan volumes in the Lending portfolio, unfavourable foreign exchange and the sale of nine aircraft in the aircraft leasing portfolio. The AWAS and Esanda acquisitions continue to perform in line with expectations. CAF’s asset and loan portfolio of $A36.5 billion decreased seven per cent on 31 March 2016 due to the impact of unfavourable foreign currency movements, net repayments and realisations in the Lending portfolio and asset depreciation.

Banking and Financial Services delivered a net profit contribution of $A513 million for FY17, up 47 per cent from $A350 million in FY16. The improved result reflects increased income from growth in Australian lending, deposit and platform average volumes, as well as a gain on sale of Macquarie Life’s risk insurance business. This was partially offset by a loss on the disposal of the US mortgages portfolio, increased impairment charges predominately on equity investments and intangible assets, increased costs mainly due to elevated project activity as well as a change in approach to the capitalisation of software expenses in relation to the Core Banking platform. BFS deposits of $A44.5 billion increased ten per cent on 31 March 2016 and funds on platform of $A72.2 billion increased 24 per cent on 31 March 2016. The Australian mortgage portfolio of $A28.7 billion increased one per cent on 31 March 2016, representing approximately two per cent of the Australian mortgage market. NIM up across Australian mortgages and business lending portfolios,

partially offset by lower NIM across business banking deposits.

Commodities and Global Markets delivered a net profit contribution of $A971 million for FY17, up 15 per cent from $A844 million in FY16. The result reflects an increase in investment-related income generated from the sale of a number of investments and a reduction in provisions for impairment compared to the prior year. This was partially offset by reduced commodities-related net interest and trading income compared to FY16 due to mixed results in power markets and base metals partially offset by increased client activity in precious metals. CGM continued to experience strong results for the energy platform, particularly in Global Oil and North American Gas and increased customer activity in foreign exchange, interest rates and futures markets due to ongoing market volatility. Equities was down on a strong prior year which benefited from strong equity market activity, particularly in China. Macquarie was awarded the 2016 Commodity House of the Year for the third consecutive year.

Macquarie Capital delivered a net profit contribution of $A483 million for FY17, up seven per cent from $A451 million in FY16. The increase was largely due to improved M&A Advisory in the US and Europe and DCM in the US and a decline in impairment charges partially offset by a decline in ECM income due to subdued equity market conditions in Australia. During FY17, Macquarie Capital advised on 417 transactions valued at $A159 billion including being joint lead manager, joint bookrunner and joint underwriter to Boral Limited’s ~$A2.1 billion equity raising to partially fund its acquisition of Headwaters Incorporated; financial adviser for a consortium led by Maeda Corporation for the privatisation of eight toll roads in Aichi Prefecture, Japan; financial adviser and debt arranger to a group of North American infrastructure investors on the acquisition of Cleco Corporation; exclusive financial adviser on Laureate Education’s $US400 million of convertible securities; capital raising and acquisition in conjunction with CGM of a 50 per cent Principal Investment in the 299MW Tees Renewable Energy Plant; and acquisition of a 25 per cent stake in the £1.6 billion, 573MW Race Bank offshore wind farm, also advising MIRA on the acquisition of a 25 per cent stake in the project.

Full year result overview

Chief Financial Officer (CFO) Patrick Upfold said: “Net operating income of $A10,364 million for FY17 was up two per cent on FY16, while total operating expenses of $A7,260 million were also up two per cent on FY16.”

Key drivers of the change from the prior year were:

A nine per cent decrease in combined net interest and trading income to $A3,954 million, down from $A4,346 million in FY16. CGM was impacted by limited trading opportunities in equity markets compared to FY16 which benefited from strong activity, particularly in China, as well as lower levels of commodities-related client activity and trading opportunities in energy markets compared to a strong FY16. Additionally, CAF was impacted by lower loan volumes in the CAF Lending portfolio and the full year impact of funding costs of the AWAS portfolio. Partially offsetting these declines was growth in average volumes and improved margins across the Australian loan portfolios in BFS, a stronger performance in foreign exchange, interest rates and credit markets products in CGM and the full year contribution of the Esanda dealer finance portfolio.

An 11 per cent decrease in fee and commission income to $A4,331 million, down from $A4,862 million in FY16. Performance fees were $A264 million in FY17, down 63 per cent on a particularly strong FY16 which benefited from significant performance fees of $A714 million. Brokerage and commissions income of $A813 million was down eight per cent from $A888 million, mainly in equities due to reduced client trading activity. Mergers and acquisitions, advisory and underwriting fees of $A963 million in FY17 was broadly in line with $A962 million in FY16 with a strong performance in mergers and acquisitions and debt capital markets fees partially offset by reduced fee income from equity capital markets activities, particularly in Australia due to subdued equity market conditions.

A five per cent increase in net operating lease income to $A921 million, up from $A880 million in FY16, mainly driven by the full year contribution of the AWAS portfolio acquisition in CAF, partially offset by unfavourable foreign currency movements for GBP denominated energy assets.

Other operating income and charges of $A1,107 million in FY17 increased significantly from $A66 million in FY16. The primary drivers were increased gains on the sale of investments and businesses; and lower charges for provisions and impairments across most operating groups with the largest decrease in CGM as a result of reduced exposures to underperforming commodity-related loans. Gains on the sale of investments and businesses included the sale of the trustee-manager of Asian Pay Television Trust (APTT) and the partial sale of holdings in Macquarie Atlas Roads (MQA) and Macquarie Infrastructure Corporation (MIC) by MAM, a significant gain from BFS’ sale of Macquarie Life’s risk insurance business to Zurich Australia Limited, as well as the sale of a number of investments in the energy and related sectors in CGM.

Total operating expenses increased two per cent, mainly due to higher employment expenses driven by increased share-based payments expenses relating to increased retained equity awards granted in previous years, higher performance-related remuneration expense largely driven by the improved overall performance of the operating groups and increased fixed remuneration due to a small increase in average headcount, partially offset by favourable foreign currency movements.

Staff numbers were 13,597 at 31 March 2017, down from 14,372 at 31 March 2016.

The income tax expense for FY17 was $A868 million, a six per cent decrease from $A927 million in FY16. The decrease was mainly due to changes in the geographic composition of earnings, with increased income being generated in Australia and the UK, and lower income in the US, combined with reduced tax uncertainties. These were partially offset by an increase in operating profit before income tax and the write-off of certain tax assets. The effective tax rate of 28.1 per cent was down from 31.0 per cent in FY16.

Strong funding and balance sheet position

“Macquarie remains well funded with a solid and conservative balance sheet, while pursuing its strategy of diversifying funding sources by continuing to grow its deposit base and accessing a variety of funding markets.” Mr Upfold said.

Total customer deposits increased by 9.6 per cent to $A47.8 billion at 31 March 2017 from $A43.6 billion at 31 March 2016. During FY17, $A10.5 billion of new term funding was raised covering a range of tenors, currencies and product types.

Capital management

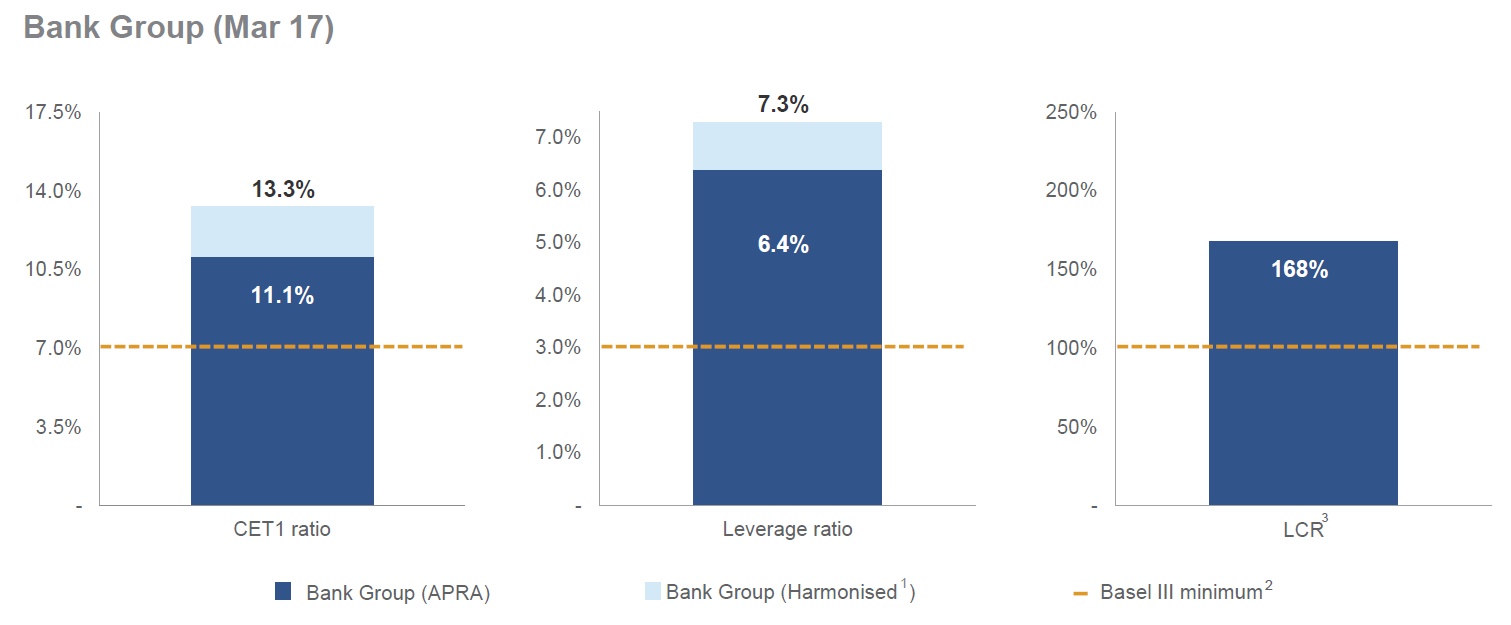

Macquarie’s financial position comfortably exceeds APRA’s Basel III regulatory requirements, with Group capital surplus of $A5.5 billion at 31 March 2017, which was up from $A3.9 billion at 31 March 2016. The Bank Group APRA Basel III Common Equity Tier 1 capital ratio was 11.1 per cent (Harmonised: 13.3 per cent) at 31 March 2017, up from 10.7 per cent (Harmonised: 12.5 per cent) at 31 March 2016. The Bank Group’s APRA leverage ratio was 6.4 per cent (Harmonised: 7.3 per cent) and LCR was 168 per cent.

Macquarie intends to purchase shares, to satisfy the MEREP requirements of approx. $A378 million. The buying period for the MEREP will commence on 16 May 2017 and is expected to be completed by 7 July 2017. No discount will apply for the 2H17 DRP and the shares are to be acquired on-market.

Exchangeable Capital Securities buyback

Macquarie today announced that following the issue of $US750 million Macquarie Additional Capital Securities (MACS) hybrid capital in March 2017, it intends to buyback $US250 million Exchangeable Capital Securities (ECS) hybrid capital in June 2017. The ECS are Basel III – transitional Additional Tier 1 securities listed in 2012. Under the proposed transaction, a Resale of ECS will take place, whereby all ECS Holders will sell to a third party financial institution for par value on 20 June 2017 after interest has been paid. Macquarie Bank Limited (London Branch) will buyback ECS immediately following the Resale such that no Exchange to Macquarie’s ordinary shares will occur. A Resale Notice will be required to be delivered to ECS Holders shortly in accordance with the ECS Terms.

Regulatory update

The Basel Committee has delayed the finalisation of proposals to amend the calculation of certain risk weighted assets under Basel III. Any impact on capital will depend upon the final form of the proposals and local implementation by APRA.

APRA has delayed until at least 1 January 2019 the implementation of a new standardised approach for measuring counterparty credit risk exposures on derivatives (SA-CCR); and capital requirements for bank exposures to central counterparties (CCPs). APRA will consult again on these requirements in 2017. APRA has also announced that it does not expect to finalise a new market risk standard until at least 2020, with implementation from 2021 at the earliest.

APRA will give more detail around the middle of the year on how it proposes to address the Financial Systems Inquiry recommendation that Australian Authorised Deposit-Taking Institutions (ADI’s) capital ratios should be unquestionably strong.

APRA released final Net Stable Funding Ratio (NSFR) requirements at the end of 2016, however the exact application of certain elements of the standard remains under discussion. The NSFR and associated changes to APRA ADI Prudential Standard APS 210 will be effective from 1 January 2018. Macquarie Bank’s NSFR was greater than 100 per cent at 31 March 2017.

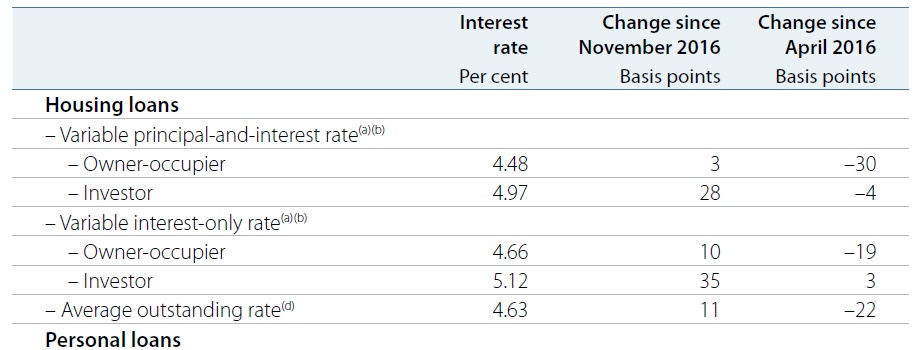

The latest RBA Quarterly Statement on Monetary Policy says low wages growth will cramp growth, and also includes information on household finances and mortgage lending. They say that interest only investors have seen an average rise of 35 basis points since Nov 2016, and a principal and interest investor of 28 basis points. Personal loan rates have also risen by 25 basis points since April 2016 (despite cash rate cuts). Major banks have a lower share of the home loan market as more business to the non-banks and other lenders.

Housing credit growth was stable in recent months at an annualised rate of around 6½ per cent. Growth in credit extended to investors has steadied at an annualised pace of around 8 per cent, after accelerating through the second half of 2016. This stabilisation in investor credit growth is consistent with the slight reduction in investor loan approvals and may have been partly driven by the increases in interest rates for investors in late 2016 along with further tightening in lending standards by lenders around that time.

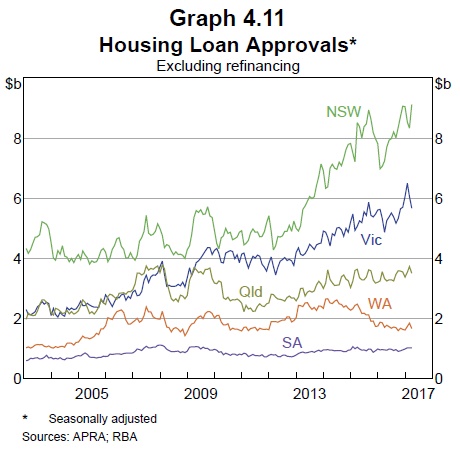

The decline in loan approvals in recent months has been driven by a decline in approvals in Victoria, while loan approvals in New South Wales have remained near record highs (Graph 4.11).

Housing finance for new dwellings has been little changed recently following rapid growth through 2016; housing finance for the construction of new homes has remained stable (Graph 4.12). Overall, loans for new dwellings or dwellings under construction are estimated to have contributed more than half of credit growth over the past year. This contribution is expected to rise, based on the pipeline of residential construction work under way.

The major banks’ share of housing loan approvals has fallen in recent months to its lowest level since 2008. Most of this reduction appears to have been absorbed by other Australian and foreign banks (Graph 4.13). Housing credit issued by entities that are not licensed by APRA as authorised deposit-taking institutions (ADIs) is estimated to have increased slightly in recent quarters, but at around 3 per cent remains a very small share of housing credit.

The further increases in housing interest rates announced by some lenders in March and April and prudential guidance from APRA and ASIC regarding interest-only lending can be expected to affect housing credit growth over the months ahead.

As outlined in the April Financial Stability Review, the Council of Financial Regulators (CFR) has been monitoring and evaluating the risks to household balance sheets. APRA announced further measures in March 2017 to reinforce sound housing lending practices. ADIs will be expected to limit new interest-only lending to 30 per cent of total new residential mortgage lending and, within that, to tightly manage new interest‑only loans extended at loan-to-value ratios above 80 per cent. APRA also reinforced the importance of banks: managing their lending so as to comfortably meet the existing investor credit growth benchmark of 10 per cent; using appropriate loan serviceability assessments, including the size of net income buffers; and continuing to exercise restraint on lending growth in higher risk segments. APRA also announced that it would monitor the growth in warehouse facilities provided by ADIs. These facilities are used by non-bank mortgage originators for short-term funding of loans until they are securitised.

In addition, the Australian Securities and Investments Commission (ASIC) announced in April further steps to ensure that interest‑only loans are appropriate for borrowers’ circumstances and that remediation can be provided to borrowers who suffer financial distress as a consequence of shortcomings in past lending practices.

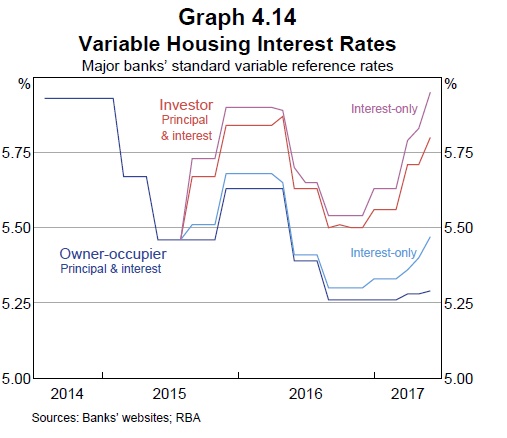

Since February, the major banks have announced an average cumulative increase to their standard variable rates of around 25 basis points for investors and a few basis points for owner‑occupiers. Also, borrowers will pay an additional premium for interest-only loans of around 15 basis points for investors and 20 basis points for owner-occupiers (Graph 4.14).

The rates actually paid on new variable rate loans are likely to differ from the major banks’ standard variable rates. The major banks and other lenders offer discounts to their standard variable rates, which can vary through time particularly for new borrowers; for example, in 2015, increases in interest rates on existing borrowers were reportedly accompanied by larger unadvertised discounts for new borrowers.

Overall, the increases that have been announced to date by lenders are expected to raise the average variable rate paid on outstanding housing loans by around 15 basis points. The average outstanding rate on all housing loans is expected to increase by slightly less than the variable rate since interest rates on new fixed-rate loans remain below those on outstanding fixed-rate loans.

As has been the case for some time, there is considerable uncertainty around the timing and extent to which domestic cost pressures will rise over the next few years. As wages are the largest component of business costs, the outlook for wage growth is particularly important for the inflation outlook. The recovery in wage growth could be stronger than anticipated if conditions in the labour market tighten by more than assumed, or if employees demand wage increases to compensate for the sustained period of low real wage growth. However, it could be the case that some of the factors currently weighing on wage growth, such as underemployment in the labour market or structural forces such as technological change, are more persistent or pervasive than assumed.

The path of inflation will also depend on whether the heightened competitive pressures in the retail sector continue to constrain inflation. On the other hand, the earlier increases in global commodity prices and increases in domestic utilities prices could flow through to domestic inflation (through higher business costs) by more than assumed.

Another factor affecting the outlook for CPI inflation is that the weight assigned to each expenditure class in the CPI will be updated in the December quarter 2017 CPI release. Measured CPI inflation is known to be upwardly biased because the weight assigned to each expenditure class is fixed for a number of years.

This means that the CPI does not take into account changes in consumer behaviour in response to relative price changes (known as ‘substitution bias’). As a result, the forthcoming re-weighting is expected to reduce measured inflation, although it is hard to predict by how much because the effects of past re-weightings have varied significantly and are not necessarily a good guide to future episodes. The ABS plans to re-weight the CPI annually in future, which will reduce substitution bias on an ongoing basis.