Though US consumer price inflation is well contained, Fed policymakers cannot help but notice the potential threat to financial stability emanating from ongoing equity price inflation. As long as US equities become more richly priced relative to both current and prospective earnings, the Fed has more than enough reason to hike rates. A further swelling of the US equity bubble will increase Fed rate-hike risks.

Not too long ago, the high-yield bond spread swelled and the projected default rate soared. However, that intensification of credit stress would be quickly reversed mostly because debt repayment problems were largely confined to the oil and gas industry. In other words, the late 2015 and early 2016 worsening of corporate credit conditions lacked enough breadth to endanger both financial stability and the business cycle upturn.

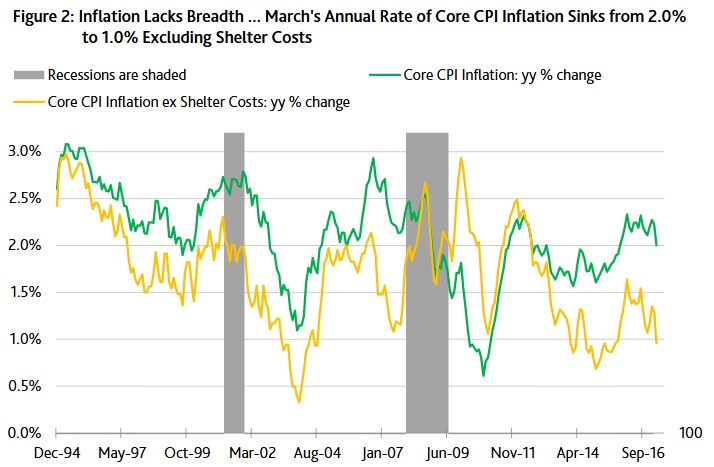

Some still hold that inflation will come roaring back. For now, however, price inflation has been confined to housing, medical care, share prices, and industrial commodities (including energy). However, industrial commodity prices have softened of late. For example, Moody’s industrial metals price index was recently -7.2% under its latest 52-week high of November 28, 2016 and was down by a deep -31.1% from its record high of April 2011. Moreover, the price of WTI crude oil was recently off by -12.2% from its latest 52-week high of February 23, 2017.

Despite the plunge by the US unemployment rate from Q1-2012’s 8.3% to Q1-2017’s 4.7%, the accompanying annual rate of PCE price index inflation slowed from 2.5% to 2.0%. Moreover, even after excluding food and energy prices, core PCE price index inflation also decelerated from Q1-2012’s 2.1% to the 1.7% of Q1-2017.

Excluding food and energy products, the US core consumer price inflation has been skewed higher by shelter costs. For example, March’s 2.0% annual rate of core CPI inflation slowed to 1.0% after excluding a 3.5% annual jump by shelter costs that supply 42% of core CPI. And recent indications are that renters’ rent inflation may soon slow owing to an abundance of new housing units coming on line in some of the US’ largest metropolitan regions.

Today, some cite the recent climb by broad measures of price inflation as signaling the approach of significantly higher interest rates. With real GDP growth expected to sputter along in a range of 2% to 2.5% annually through 2018 how else can you explain expectations of a climb by the 10-year Treasury yield from its recent 2.35% to 3.3% by 2018’s final quarter?

Often, reference is made to a tighter labor market for the purpose of invoking a sense of danger regarding a possible imminent return of runaway price inflation. According to one highly-respected economics group, “ the U.S. economy has now reached full employment and is likely to overshoot meaningfully, a path that has often proven risky”.

Nevertheless, large numbers of labor force dropouts suggest that the unemployment rate may be overstating labor market tightness. For example, though the unemployment rate plunged by -3.6 percentage points from Q1-2012’s 8.3% to Q1-2017’s 4.7%, the ratio of payrolls to the working-age population rose by a smaller +2.2 points from Q1-2012’s 55.1% to Q1-2017’s 57.3%. Coincidentally, despite how 2005-2007 showed a much higher 59.5% ratio of payrolls to the working-age population, by no means did any overheating by the labor market prove risky.

Put simply, the Phillips Curve is not what it used to be. A lower unemployment rate now supplies less of a lift to price inflation compared to the past. In fact, sometimes consumer price inflation slows notwithstanding a substantially lower jobless rate.

Automated advice is not a disruptive innovation and will only sustain the existing business models of the major banks, according to venture capital firm Reinventure.

Reinventure general partner Kara Frederick says the Westpac-backed venture capital fund will not be investing in robo-advice any time soon.

Ms Frederick, who is a Silicon Valley ‘native’, joined Reinventure founders Danny Gilligan and Simon Cant in March to help them broaden the fund’s reach into the US.

Speaking to InvestorDaily, she distinguished “sustaining” innovation products – such as robo-advice – from truly disruptive fintech technology. Reinventure is backing the latter, rather than the former, she said.

The venture capital fund has $100 million in total to invest, with approximately $45 million already committed to a portfolio of 15 companies.

When it comes to developing innovative technologies, banks typically have three approaches available to them, which are “build, buy or partner”, Ms Frederick said.

“If a bank’s going to go out of its way to do an incremental build or an entire build, that’s probably not where Reinventure’s going to play at all,” she said.

“Because we see that as sustaining innovation and that’s where we see most of the robo-advice products.”

Reinventure is more interested in the technologies that banks will either buy or partner with.

“The reason [banks want to buy or partner] is because it’s either too far in the future – it’s a potential real disruption but it’s not one or two years’ away,” Ms Frederick said.

“When you think of fintech globally, [Reinventure] sits in more of the ‘buy and partner’ side whereas the ‘build’ is more intrinsic to the banks themselves.”

Ms Frederick helped Reinventure invest in SME debt management start-up InDebted on Monday, and she has taken up a position on the start-up’s board.

In a landmark speech, Reserve Bank of Australia governor Philip Lowe has outlined his nightmare scenario of a property market crash, as well as his favourite solution to the affordability crisis.

The RBA is not overly concerned that a “severe correction in property prices” would trigger a banking collapse, as happened in the US in 2008-09, Dr Lowe said on Thursday.

No, he said he was far more worried that Australians would bring the economy to a grinding halt by curbing their spending.

“The Australian banks are resilient and they are soundly capitalised. A significant correction in the property market would, no doubt, affect their profitability. But the stress tests that have been done under APRA’s eye confirm that the banks are resilient to large movements in the price of residential property,” Dr Lowe told the Economic Society of Australia.

“Instead, the issue we have focused on is the possibility of future sharp cuts in household spending because of stretched balance sheets.”

Household debt is “high” relative to incomes, making it likely that many Australians would respond to a market correction with a “sharp correction in their spending”, in an attempt to pay down debt.

“An otherwise manageable downturn could be turned into something more serious.”

The golden solution

Dr Lowe’s speech contained a comprehensive answer to what has caused house prices to skyrocket, at least in Sydney and Melbourne, and what should be done to fix it.

The answer was unlikely to be comforting for either the Liberals or Labor, as it touched on both supply and demand-side fixes.

He dismissed allowing young Australians to use their superannuation for a deposit. “You don’t address affordability by adding to demand.”

But he also downplayed the importance of tax policies. “The best housing policy is really a transport policy,” he said during a question-and-answer session at the end.

In the speech itself, the Governor blamed the house price explosion on an encyclopaedic list of factors, including an increased ability to borrow via financial liberalisation and lower interest rates; supply constrained by zoning issues, geography and, crucially, inadequate roads and trains to link outer suburbs to the inner city.

He also pointed to Australians’ preference for big houses in the big cities; slow income growth; stronger-than-expected population growth; and the rise of investors.

While much has been made of the crackdown of APRA and ASIC on bank lending to investors — indeed, constraining investor demand is the centrepiece of Labor’s solution — Dr Lowe placed far more emphasis on supply issues.

“This borrowing [by investors] is not the underlying cause of the higher housing prices. But the borrowing has added to the upward pressure on prices caused by the underlying supply-demand dynamics. It has acted as a financial amplifier in some cities, adding to the already upward pressure on prices.”

The Governor noted in passing that tax policies (presumably negative gearing and the 50 per cent capital gains tax discount) would “have an effect”, but he was more optimistic about faster rates of home-building, better transport infrastructure, and an eventual rise in the RBA’s cash rate.

“Increased supply and better transport could be expected to help address the ongoing rises in housing prices relative to incomes. These changes and some normalisation of interest rates over time might also reduce the incentive to borrow to invest in an asset whose price is rising strongly.”

RBA Governor Philip Lowe spoke at the Economic Society of Australia (QLD) Business Lunch. Of note is the data which shows one third of households with a mortgage have little or no interest rate buffer, and that the Reserve Bank does not have a target for the debt-to-income ratio or the ratio of nationwide housing prices to income.

This afternoon I would like to talk about household debt and housing prices.

This is a familiar topic and one that has attracted a lot of attention over recent times. It is understandable why this is so. The cost of housing and how we finance it matters to us all. We all need somewhere to live and for many people, their home is their largest single asset. Real estate is also the major form of collateral for bank lending. The levels of debt and housing prices also affect the resilience of our economy to future shocks. Beyond these economic effects, high levels of debt and housing prices have broader effects on the communities in which we live. The high cost of housing is a real issue for many Australians and can have serious side-effects. High levels of debt and high housing costs can also reinforce the existing distribution of wealth in our society, making social and geographic mobility more difficult. So it is understandable why Australians are so interested in these issues.

At the Reserve Bank, we too have been focused on these issues in the context of our monetary policy and financial stability responsibilities. Our work has been in three broad areas. First, understanding the aggregate trends and their causes. Second, understanding how debt is distributed across the community. And third, understanding how the level of debt and housing prices affect the way the economy operates and its resilience to future shocks.

This afternoon, I would like to make some observations in each of these three areas.

Aggregate Trends

This first chart provides a good summary of the aggregate picture (Graph 1). It shows the ratios of nationwide housing prices and household debt to household income. Housing prices and debt both rose a lot from the mid 1990s to the early 2000s. The ratios then moved sideways for the better part of a decade – in some years they were up and in others they were down. Then, in the past few years, these ratios have been rising again. Both are now at record highs.

Graph 1

Although the debt-to-income ratio has increased over recent times, the ratio of debt to the value of the housing stock has not risen. This reflects the large increase in housing prices and the growth in the number of homes. Over recent times, there has also been a substantial increase in the value of households’ financial assets, with the result that the ratio of household wealth to income is at a record high (Graph 2). So both the value of our assets and the value of our liabilities have increased relative to our incomes.

Graph 2

Turning now to why the ratios of housing prices and debt to income have risen over time. A central factor is that financial liberalisation and the lower nominal interest rates that came with the lower inflation of the 1990s increased people’s ability to borrow. These developments meant that Australians could take out larger and more flexible loans. By and large, we took advantage of this new ability, as we sought to buy the housing we desired.

We could, of course, have used the benefit of lower nominal interest rates in the 1990s and the increased ability to borrow for other purposes. But instead we chose to borrow more for housing and this pushed up the average price of housing given the constraints on the supply side. The supply of well-located housing and land in our cities has been constrained by a combination of zoning issues, geography and inadequate transport. Another related factor was that our population was growing at a reasonable pace. Adding to the picture, Australians consume more land per dwelling than is possible in many other countries, although this is changing, and many of us have chosen to live in a few large coastal cities. Increased ability to borrow, more demand and constrained supply meant higher prices.

So we saw marked increases in the ratios of housing prices and debt to household incomes up until the early 2000s. At the time, there was much discussion as to whether these higher ratios were sustainable. As things turned out, the higher ratios have been sustained for quite a while. This largely reflects the choices we have made as a society regarding where and how we live (and how much at least some of us are prepared to spend to do so), urban planning and transport, and the nature of our financial system. It is these choices that have underpinned the high level of housing prices. So the changes that we have seen in these ratios are largely structural.

Recently, the ratios of housing prices and debt to household income have been increasing again. Lower interest rates both in real and nominal terms – this time, largely reflecting global developments – have again played some role. But there have also been other important factors at work over recent times.

One of these is the slow growth in household income. During the 2000s, aggregate household income increased at an average rate of over 7 per cent (Graph 3). In contrast, over the past four years growth has averaged less than half of this, at about 3 per cent. Slower growth in incomes will push up the debt-to-income ratio unless growth in debt also slows. This partly explains what has happened over recent years.

Graph 3

A second factor is that some of our cities have become major global cities. Reflecting this, in some markets there has been strong demand by overseas investors.

A third factor has been stronger population growth. Population growth picked up during the mining investment boom and, although it subsequently slowed, it is still around ½ percentage point faster than it was before the boom (Graph 4). For some time the rate of home-building did not respond to the faster population growth; indeed, the response took the better part of a decade. The rate of home-building has now responded and we are currently adding to the housing stock at a rate not seen for more than two decades. Over time, this will make a difference.

Graph 4

It is Melbourne and Sydney where population growth has been the fastest over recent times. Not surprisingly, it is these two cities where the price gains have been largest, and these price gains have helped induce more supply. Indeed, Victoria and New South Wales account for all of the recent upward movement in the national housing price-to-income ratio (Graph 5). In the other states, the ratio of housing prices to income is below previous peaks. So there is not a single story across the country. This is despite us having a common monetary policy for the country as a whole. Factors other than the level of interest rates are clearly at work.

Graph 5

In summary then, the supply-demand dynamics have been pushing aggregate housing prices in our largest cities higher relative to our incomes. With interest rates as low as they have been, and prices rising, many people have found it attractive to borrow money to invest in an asset whose price is increasing. The result has been strong growth in borrowing by investors, with investors accounting for 30 to 40 per cent of new loans.

This borrowing is not the underlying cause of the higher housing prices. But the borrowing has added to the upward pressure on prices caused by the underlying supply-demand dynamics. It has acted as a financial amplifier in some cities, adding to the already upward pressure on prices. The borrowing by investors is also obviously contributing to the rise in the aggregate debt-to-income ratio. Just like in the early 2000s, there is again a discussion as to whether these increases will continue and whether they are sustainable.

The Distribution of Debt

I would now like to turn to the distribution of housing debt across households. This is important, as it is not the ‘average’ household that gets into trouble. At the Reserve Bank we have devoted considerable resources to understanding this distribution. One important source of household-level information is the survey of Household Income and Labour Dynamics in Australia (HILDA).

If we look across the income distribution, it is clear that the rise in the debt-to-income ratio has been most pronounced for higher-income households (Graph 6). This is different from what occurred in the United States in the run-up to the subprime crisis, when many lower-income households borrowed a lot of money.

Graph 6

It is also possible to look at how the debt-to-income ratio has changed across the age distribution. This ratio has risen for households of all ages, except the very youngest, who tend to have low levels of debt (Graph 7). Borrowers of all ages have taken out larger mortgages relative to their incomes and they are taking longer to pay them off. Older households are also more likely than before to have an investment property with a mortgage and it has become more common to have a mortgage at the time of retirement.

Graph 7

We also look at the share of households with a debt-to-income ratio above specific thresholds. In 2002, around 12 per cent of households had debt that was over three times their income (Graph 8). By 2014, this figure had increased to 20 per cent of households. There has also been an increase, although not as pronounced, in the share of households with even higher debt-to-income ratios.

Graph 8

Another dataset that provides insight into distributional issues is one maintained by the Reserve Bank on loans that have been securitised. This indicates that around two-thirds of housing borrowers are at least one month ahead of their scheduled repayments and half of borrowers are six months or more ahead (Graph 9). This is good news. But a substantial number of borrowers have only small buffers if things go wrong.

Graph 9

At the overall level, though, nationwide indicators of household financial stress remain contained. This is not surprising with many borrowers materially ahead on their mortgage repayments, interest rates being low and the unemployment rate being broadly steady over recent years. At the same time, though, the household-level data show that there has been a fairly broad-based increase in indebtedness across the population and the number of highly indebted households has increased.

Impact on Economy and Policy Considerations

I would now like to turn to the third element of our work: the implications of all this for the way the economy operates and its resilience.

It is now commonplace to say that housing prices and debt levels matter because of financial stability. What people typically have in mind is that a severe correction in property prices when balance sheets are highly leveraged could make for instability in the banking system, damaging the economy. So the traditional financial stability concern is that the banks get in trouble and this causes trouble for the overall economy.

This is not what lies behind the Reserve Bank’s recent focus on household debt and housing prices in Australia. The Australian banks are resilient and they are soundly capitalised. A significant correction in the property market would, no doubt, affect their profitability. But the stress tests that have been done under APRA’s eye confirm that the banks are resilient to large movements in the price of residential property.

Instead, the issue we have focused on is the possibility of future sharp cuts in household spending because of stretched balance sheets. Given the high levels of debt and housing prices, relative to incomes, it is likely that some households respond to a future shock to income or housing prices by deciding that they have borrowed too much. This could prompt a sharp contraction in their spending, as they try to get their balance sheets back into better shape. An otherwise manageable downturn could be turned into something more serious. So the financial stability question is: to what extent does the higher level of household debt make us less resilient to future shocks?

Answering this question with precision is difficult. History does not provide a particularly good guide, given that housing prices and debt relative to income are at levels that we have not seen before, and the distribution of debt across the population is changing.

Given this, one of the research priorities at the Reserve Bank has been to use individual household data to understand better how the level of indebtedness affects household spending. The results indicate that the higher is indebtedness, the greater is the sensitivity of spending to shocks to income. This is regardless of whether we measure indebtedness by the debt-to-income ratio or the share of income spent on servicing the debt. If this result were to translate to the aggregate level, it would mean that higher levels of debt increase the sensitivity of future consumer spending to certain shocks.

The higher debt levels also appear to have affected how higher housing prices influence household spending. For some years, households used the increasing equity in their homes to finance extra spending. Today, the reaction seems different. This is evident in the estimates of housing equity injection (Graph 10). In earlier periods of rising housing prices, the household sector was withdrawing equity from their housing to finance spending. Today, households are much less inclined to do this. Many of us feel that we have enough debt and don’t want to increase consumption using borrowed money. Many also worry about the impact of higher housing prices on the future cost of housing for their children. As I have spoken about previously, higher housing prices are a two-edged sword. They deliver capital gains for the current owners, but increase the cost of future housing services, including for our children.

Graph 10

This change in attitude is also affecting how spending responds to lower interest rates. With less appetite to incur more debt for current consumption, this part of the monetary transmission mechanism looks to be weaker than it once was. There is, however, likely to be an asymmetry here. When the interest rate cycle turns and rates begin to rise, the higher debt levels are likely to make spending more responsive to interest rates than was the case in the past. This is something that we will need to take into account.

In terms of resilience, my overall assessment is that the recent increase in household debt relative to our incomes has made the economy less resilient to future shocks. Given this assessment, the Reserve Bank has strongly supported the prudential measures undertaken by APRA. Double-digit growth in debt owed by investors at a time of weak income growth cannot be strengthening the resilience of our economy. Nor can a high concentration of interest-only loans.

I want to point out that APRA’s measures are not targeted at high housing prices. The international evidence is that these types of measures cannot sustainably address pressures on housing prices originating from the underlying supply-demand balance. But they can provide some breathing space while the underlying issues are addressed. In doing so, they can help lessen the financial amplification of the cycle that I spoke about before. Reducing this amplification while a better balance is established between supply and demand in the housing market can help with the resilience of our economy.

There are some reasons to expect that a better balance between supply and demand will be established over time.

One is the increased rate of home-building. As we are seeing here in Brisbane and some parts of Melbourne, increased supply does affect prices. This increase in supply is also affecting rents, which are increasing very slowly in most markets.

A second reason is the increased investment in some cities, including in Sydney, on transport. Over time, this will increase the supply of well-located residential land, and this will help as well.

And a third reason is that at some point, interest rates in Australia will increase. To be clear, this is not a signal about the near-term outlook for interest rates in Australia but rather a reminder that over time we could expect interest rates to rise, not least because of global developments. Over recent years, the low interest rates in Australia have helped the economy adjust to the winding down of the mining investment boom. They have helped support employment and demand through a significant adjustment in the Australian economy. We should not, though, expect interest rates always to be this low.

It remains to be seen how the various influences on housing prices play out. Other policies, including tax and zoning policies, also have an effect. But increased supply and better transport could be expected to help address the ongoing rises in housing prices relative to incomes. These changes and some normalisation of interest rates over time might also reduce the incentive to borrow to invest in an asset whose price is rising strongly. To the extent that, over time, a better balance is established, we will be better off not incurring too much debt, and having housing prices go too high, while this is occurring.

I want to make it clear that the Reserve Bank does not have a target for the debt-to-income ratio or the ratio of nationwide housing prices to income.

As I spoke about earlier, there are good reasons why these ratios move over time. My judgement, though, is that, in the current environment, the resilience of our economy would be enhanced by an extended period in which housing prices and debt outstanding increased no faster than our incomes. Again, this is not a target or a policy objective of the Reserve Bank, but rather a general observation about how we build resilience.

Many of you will be aware that these issues have figured in the deliberations of the Reserve Bank Board for some time. This is entirely consistent with our flexible medium-term inflation targeting framework. With a medium-term target, it is appropriate that we pay attention to the resilience of our economy to future shocks. In the current environment of low income growth, faster growth in household debt is unlikely to help that resilience.

We have also been watching the labour market closely. The unemployment rate has moved up a little over recent months and wage growth remains subdued. Encouragingly, employment growth has been a bit stronger of late and the forward-looking indicators suggest ongoing growth in employment. We will want to see a continuation of these trends if the overall growth in the economy is to pick up as we expect. Stronger growth in incomes would of course also help people deal with the high levels of debt and housing prices. Overall, our latest forecast is for economic growth to pick up gradually and average around 3 per cent or so over the next few years.

To conclude, I hope these remarks help provide some insight into the Reserve Bank’s thinking about housing prices and household debt. As household balance sheets have changed, so too has the way that the economy works. Both from an individual and an economy-wide perspective, we need to pay attention to how the higher level of debt affects our resilience to future shocks.

Suncorp has announced an exclusive new offer for first home buyers to “help them realise their property ownership dreams”.

Suncorp’s Home Package Plus Special Offer for First Home Buyers allows customers to choose from a Standard Variable rate or a 5 Year Fixed rate of 3.99% p.a. on new lending of $150,000 or more.

The initial Home Package Plus annual fee will be waived and most customers will also be eligible for savings on their Lenders Mortgage Insurance (LMI) , as well as building and contents insurance.

Suncorp EGM Stores and Specialty Banking, Lynne Sutherland, said buying a home is one of the biggest financial commitments customers make and it’s becoming increasingly difficult for those looking to enter the market for the first time.

“Housing affordability is creating a barrier for young people wanting to purchase their first home,” Sutherland said.

“The average age of home owners across the country has increased by 10 years, and while we know property ownership isn’t for everyone, it’s still a goal for many Australians.

“Our Home Package Plus Special Offer for First Home Buyers gives customers choice by providing the same low rate on a Standard Variable or 5 Year Fixed loan, while also offering a range of discounts on some of the additional fees and products that go with home ownership.

“Where the customer is borrowing more than 80% of the property’s value, we will contribute $1,000 towards their mortgage insurance premium.

“Eligible customers will also be offered 20% off the first year’s premium for Suncorp issued building and contents insurance, as well as savings on Suncorp Home Loan Protect for new policies issued.

“This offer is especially timely for first home buyers in Queensland, with the Government’s First Home Owner’s $20,000 grant only available until 30 June 2017.

“Entering the property market can be daunting, but these savings could be the difference for many of our customers in realising home ownership.”

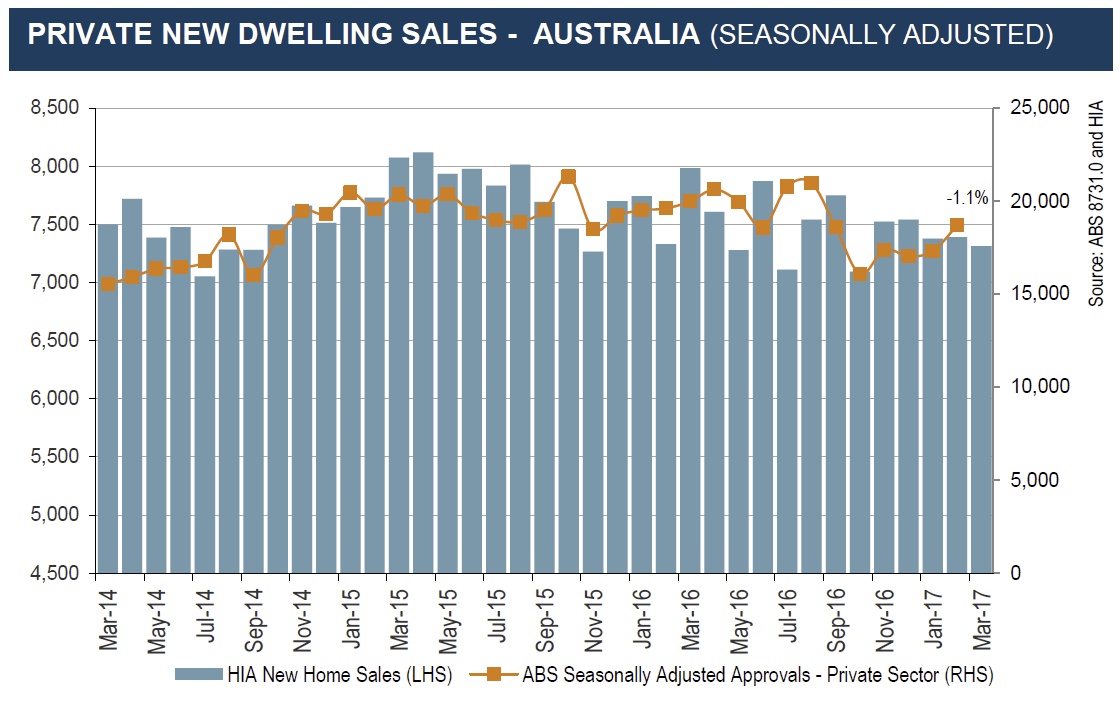

The HIA New Homes Sales Report – a survey of Australia’s largest home builders – shows a modest decline in total new home sales during March 2017.

Amongst the jurisdictions surveyed, NSW was the only state to record an increase in detached house sales in March, posting a 10.4 per cent rebound after a soft result in February. Detached house sales fell by 4.6 per cent in Victoria, by 5.4 per cent in Queensland and fell in South Australia and Western Australia fell by 1.7 per cent and 1.2 per cent respectively.

“New home sales across the country eased by around 1.1 per cent in March 2017,” said HIA Economist, Geordan Murray. “The decline was more evident in detached house sales which were down by 1.4 per cent in March. Sales of ‘multi-units’ eased by only 0.1 per cent in the month.

“With residential building activity having peaked at a record level in 2016, industry spectators are watching leading indicators closely to assess where activity may be headed in the next phase of the cycle.

“In particular, there has been a high degree of speculation about the trajectory of activity in the multi-unit market given the unprecedentedly large role it has played throughout the upside of the cycle. The new home sales survey shows that sales have been sustained at a relatively high level though to March this year.

“Similarly, detached house sales are indicating only a slight downward trend. This is consistent with other data on building approvals and dwelling commencements,” concluded Geordan Murray.

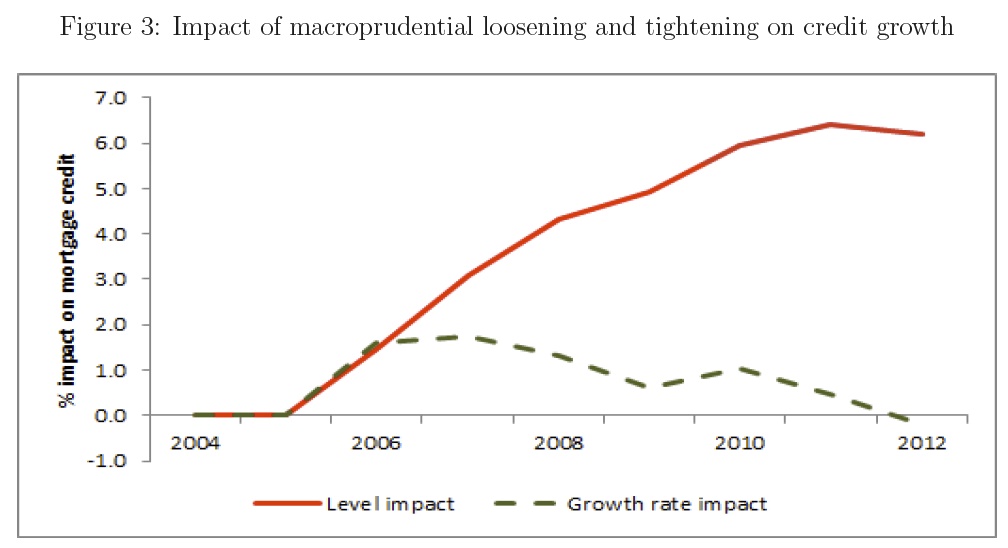

Do policies which seek to regulate serviceability, such as debt to income, or debt servicing ratios, work better than loan to value controls? A highly relevant question given the fact that some central banks are going down the debt to income approach (e.g Bank of England has implement high DTI thresholds) and Reserve Bank NZ is exploring this at the moment).

It seems from their research that income related constraints work well for higher income households, but loan to value methods work better for households with more constrained incomes. So perhaps DTI measures should be targetted at more wealthy households seeking larger loans.

This was a paper produced as part of the BIS Consultative Council for the Americas (CCA) research project on “The impact of macroprudential policies: an empirical analysis using credit registry data” implemented by a Working Group of the CCA Consultative Group of Directors of Financial Stability (CGDFS).

The paper combines loan-level administrative data with household-level survey data to analyze the impact of recent macroprudential policy changes in Canada using a microsimulation model of mortgage demand of first-time homebuyers.

They found that policies targeting the loan-to-value ratio have a larger impact on demand than policies targeting the debt-service ratio, such as amortization. In addition, they show that loan-to-value policies have a larger role to play in reducing default than income-based policies.

The results of the experiments suggest that wealth constraints are more effective than income constraints at affecting mortgage demand, particularly on the extensive margin, for a given proportional change and the given starting points of policy parameters (95% maximum LTV and maximum 25-year amortization for insured mortgages).

Income constraints, however, are just as effective as wealth constraints for high-wealth homebuyers. The focus of the empirical analysis and the model, however, is on mortgage demand, and ignores some aspects of the general market for housing as well as potential supply effects.

From changes in consumer demand, we fnd that LTV constraints, which work through the wealth channel, are effective housing finance tools. Given that the average household is able to meet changes in cash flow, we conclude that, at least with the types of changes we observe to amortization, that changes directed at household repayment constraint are less effective. Households are attracted to these products, however, they are not binding.

An important contribution of this paper is the use of microsimulation modeling to capture the interactions of multiple policy tools and the non-linearities in consumer responses. This model imposes some structure on how we interpret the data while still being highly flexible in capturing nonlinear responses that more traditional, rational forward-looking dynamic stochastic general equilibrium models generally have difficulty capturing. The model allows us to map the impact of a policy change on the percentage of FTHBs who enter the market and their demand for credit. The results of our microsimulation model suggest that the wealth constraint has the largest impact on the number of FTHBs who enter the housing market and amount of debt that they hold. However, the impact of changes in amortization, which affect the income constraint, do affect high-wealth households. Finally, we show that LTV policies seem to reduce the impact of interest rate shocks on household vulnerabilities relative to income-based policies.

A caveat of our results is that we have taken as given that lenders are able to change the supply of credit exogenously in response to changes in macroprudential policy. This appears

reasonable, given that banks do not face default risk in the Canadian (insured) mortgage market. However, if there is a tightening, banks might react strategically to price mortgages

in a way that partially offsets changes in macroprudential policies. More importantly, we do not capture general equilibrium effects. A relaxation of mortgage insurance guidelines leads to entry of FTHBs, which can lead to house price appreciation, which leads to further entry and greater house price appreciation. This can affect both current and future mortgage demand in a way that is not captured in the model.

Note: BIS Working Papers are written by members of the Monetary and Economic Department of the Bank for International Settlements, and from time to time by other economists, and are published by the Bank. The papers are on subjects of topical interest and are technical in character. The views expressed in them are those of their authors and not necessarily the views of the BIS.

ANZ has sold its stake in the ANZ ETFS joint venture with ETF Securities just two years after the partnership was launched in May 2015.

Graham Tuckwell’s ETF Securities has taken full control of the ANZ ETFs joint venture that was launched in May 2015 after ANZ sold back its stake in the business.

ANZ managing director of markets, institutional, Shayne Collins said the decision to sell the stake was “based on ANZ’s desire to simplify the Institutional business, and increase focus on supporting client trade and capital flows across the region”.

ANZ chief executive has previously stated his intention to exit product manufacturing, and is actively courting buyers for the bank’s wealth management business.

As a result of the sale, ANZ ETFS will be rebranded ETF Securities Australia, which will be a wholly-owned subsidiary of the ETF Securities Group.

The firm will continue to be led by Kris Walesby, the current head of ANZ ETFs.

“We are committed to delivering an ambitious programme of new products which we expect to start rolling out over the remainder of 2017,” Mr Walesby said.

“We already have a strong foundation here with 13 ETPs listed on the ASX (eight launched under the ANZ ETFS name and five existing ETF Securities products),” he said.

NAB has released their 2017 Half results. They reported cash earnings (“cash earnings” is calculated by excluding discontinued operations and certain other items) of $3.29 billion, up 2.3% compared to March 2016 half year.

There are some positives, with stronger contributions from markets and treasury (but of course less easy to replicate next time), net interest margin higher in the business sector, but lower momentum and margins in the home lending sector, rising delinquencies and higher provisions for commercial real estate. Capital ratios are strong, and funding well managed. Benefits from technology investments are flowing.

On a statutory basis, net profit attributable to the owners of NAB was $2.55 billion compared to a loss of $1.74 billion for the March 2016 half year. The improved result primarily reflects reduced losses from discontinued operations. Excluding discontinued operations, statutory net profit decreased 11.4%. The main difference between statutory and cash earnings relates to the effects of fair value and hedge ineffectiveness, and discontinued operations.

Revenue increased 1.8% benefitting from growth in lending, improved fee collection and stronger trading income.

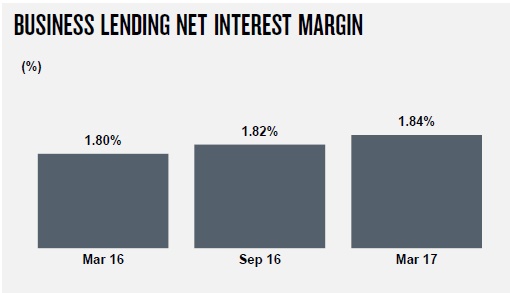

Group net interest margin (NIM) declined 11 basis points but excluding Markets and Treasury was down 4 basis points. Compared to the September 2016 half year NIM was stable at 1.82%.

Expenses rose 0.8% reflecting higher personnel costs including redundancy charges, and increased technology depreciation and amortisation charges, partly offset by productivity savings.

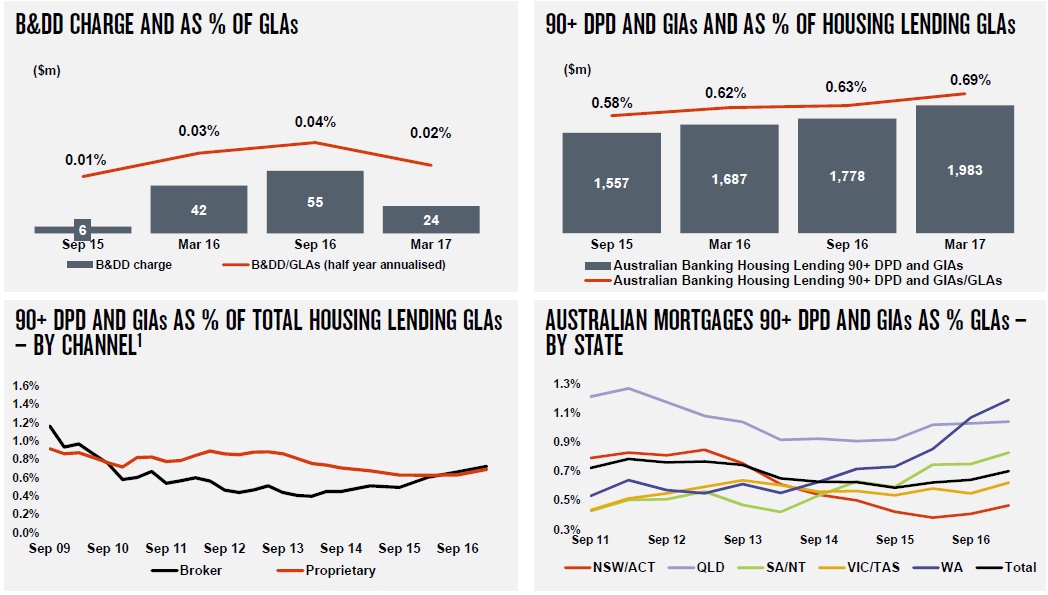

The total charge for Bad and Doubtful Debts (B&DDs) was $394 million, up $19 million or 5.1%. The charge this period includes an increase in collective provision (CP) overlays of $89 million mainly for potential risks relating to the commercial real estate (CRE) portfolio. The Group’s total CP overlays for CRE, agriculture, mining and mining related sectors now stand at $291 million.

The ratio of Group 90+ days past due and gross impaired assets to gross loans and acceptances of 0.85% at 31 March 2017 was stable compared to 30 September 2016.

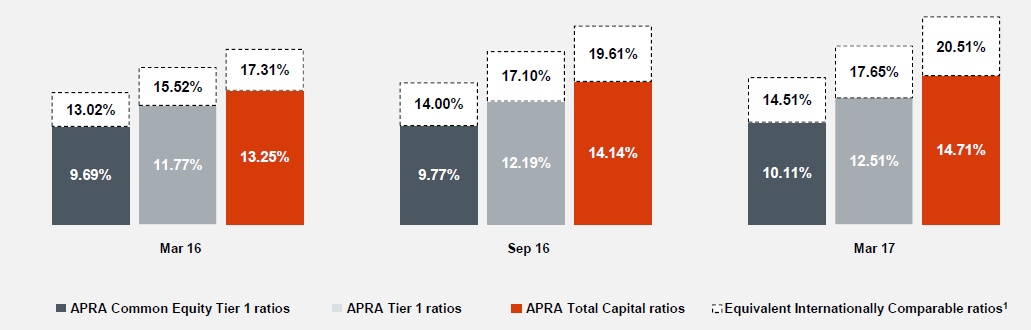

The Group’s Common Equity Tier 1 (CET1) ratio was 10.1% as at 31 March 2017, an increase of 34 basis points from 30 September 2016. The Group’s CET1 target ratio remains between 8.75% – 9.25%. On an internationally comparable basis3 the CET1 ratio increased 51 basis points from 30 September 2016 to 14.5%.

The interim dividend is 99 cents per share fully franked, unchanged from the 2016 interim and final dividends.

The Group says it maintains a well diversified funding profile and raised $18.8 billion of term wholesale funding in the March 2017 half year across a range of markets. The weighted average term to maturity of the funds raised by the Group over the March 2017 half year was 5.4 years. The net stable funding ratio (NSFR) was 108% at 31 March 2017.

The Group’s leverage ratio as at 31 March 2017 was 5.5% on an APRA basis and 5.9% on an internationally comparable basis.

The Group’s quarterly average liquidity coverage ratio as at 31 March 2017 was 122%.

Business & Private Banking grew cash earnings 2.5% to $1,368 million reflecting sound revenue growth and tight cost management, partly offset by higher B&DD charges. NIM improved and lending growth in specialised businesses such as Health and Agribusiness was strong.

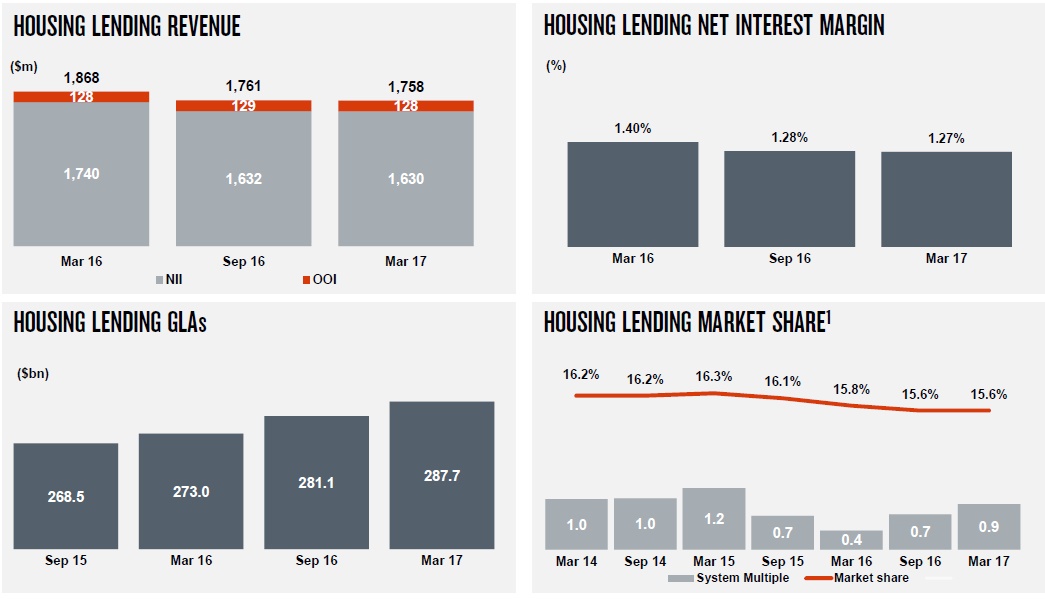

Consumer Banking & Wealth cash earnings were stable at $764 million impacted by higher funding costs, increased competition in home lending, and reduced Wealth income. NIM stabilised compared to the September 2016 half year and more recent home lending market share trends are improving.

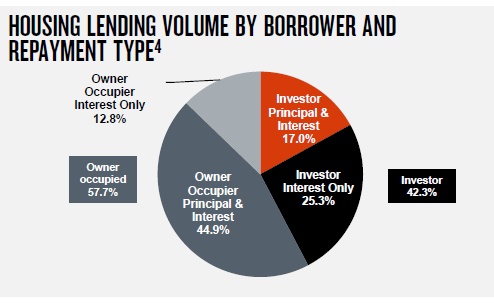

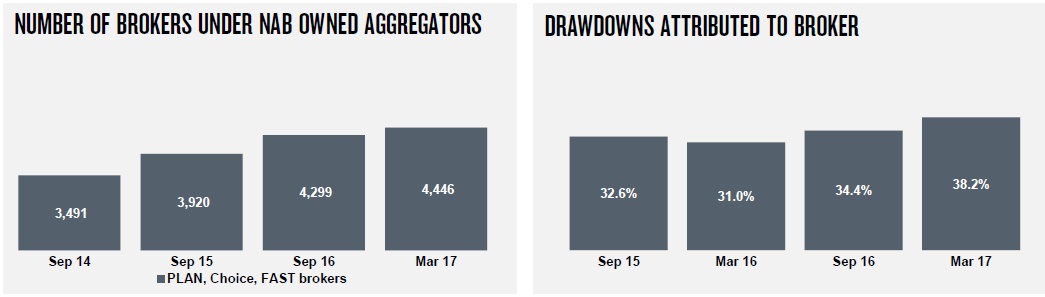

Looking at home lending, 42.3% are investor loans, and more than half of these are interest only.

Drawdowns from brokers continued to rise, as did the number of brokers under NAB owned aggregators.

Housing net interest margin fell, as did home lending revenue. They are growing below system.

Delinquencies are rising across the portfolio. They have limited exposure to commercial real estate (but provisions are up), and to higher risk mining post codes.

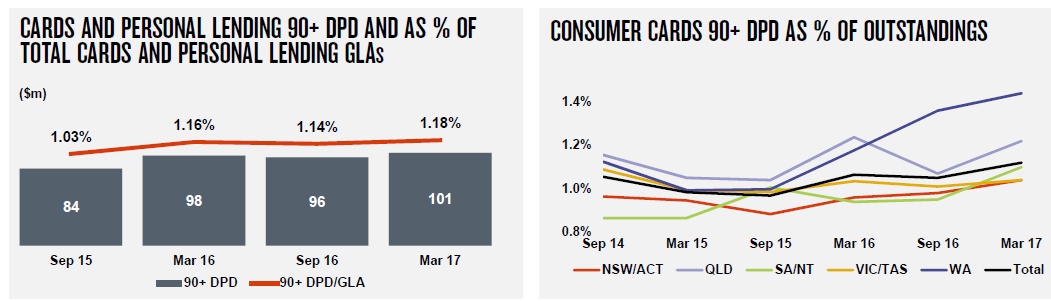

Card and personal lending delinquencies are also rising.

Corporate & Institutional Banking (CIB) cash earnings rose 17.9% to $791 million. This was a strong result underpinned by a disciplined focus on returns. Over the year to March 2017 CIB delivered revenue growth, lower costs, lower B&DD charges and a $15 billion reduction in risk weighted assets.

NZ Banking local currency cash earnings increased 10.4% to NZ$455 million. Improved economic conditions, and in particular a better outlook for the dairy sector, (provisions down ~90% compared with prior half) have resulted in lower B&DD charges. Strong growth in business and home lending reflect successful expansion in priority segments. NZ net interest margin fell.

NAB Group CEO Andrew Thorburn said:

“The rollout of the Net Promoter Score (NPS) system to all our front line teams is an important tool that helps bankers take greater ownership of the customer experience. Every branch, contact centre and business banking centre now receives localised weekly scores and real time customer feedback resulting in improved customer outcomes on our front line.

“Technology underpins our ability to serve customers better by becoming easier and simpler to deal with. Over the half we have made further progress embedding the Personal Banking Origination Platform (PBOP) into our network. Approximately 55% of customers are now receiving unconditional home loan approval within 5 days compared to 7% at September 2016.

“Disciplines in place to reshape our business, including use of automation and meeting more of our customers’ needs digitally, are delivering efficiency benefits. In 1H17 we achieved $102 million of productivity savings against an annual target of greater than $200 million. We remain confident of achieving positive ‘jaws’ over the full year as a number of initiatives gain further traction during the second half of 2017”.

The House Of Representatives Standing Committee on Economics released its Major Banks Second Report in April 2017. Right over the Easter break and just before the budget!

Its a pretty weak document, in that while the issues they raise are quite important they miss the core structural issues which beset the industry, from vertical integration, lack to real competition, price gouging and poor culture. In fact the FSI inquiry did a better job, and there are still open issues from that review.

We think the “review fest” needs to stop and the focus should shift to making real change. This is what the summary of report 2 says:

The Committee’s second round of hearings has confirmed that the Recommendations of the First Report should be implemented now in order to improve the Australian banking sector for the benefit of customers. The Committee reaffirms each Recommendation from the First Report. While the Committee is open to some modest variations to the Recommendations, it affirms the substance of each of them.

Recommendation 1 of the First Report proposed the establishment of a one-stopshop where consumers can access redress when they are wronged by a bank. The Committee retains its view that one dispute resolution body should be established to provide straightforward redress for consumers. It is highly preferable to have one body dealing with these matters rather than two or more. The Committee believes that the Ramsay review should determine the precise administrative structure of this body – the key point is that it should be a one-stop-shop.

Recommendation 2 of the First Report calls for a new public reporting regime to be put in place to hold senior bank executives much more accountable. This Recommendation is essential to achieving a change in bank culture. It will place relentless pressure on CEO-reporting executives to focus on the treatment of customers. While all of the banks except ANZ oppose this Recommendation, in the Committee’s view it will have a very substantial impact on the behaviour of banks, to the benefit of consumers. It should be implemented.

Recommendation 3 of the First Report proposed that a regulatory team be established to make recommendations on improving competition in the banking sector to the Treasurer every six months. The ANZ agreed with Recommendation noting that ‘analysis from a government agency would help demonstrate the nature and level of competition.’ The other banks oppose this Recommendation, for reasons that the Committee does not find persuasive. This team should be put in place to fill a substantial gap in Australia’s regulatory framework today: we do not currently have a permanent team focused on systemic competition issues in banking, and we should.

Recommendations 4 and 5 of the First Report seek to empower consumers. In particular, Recommendation 4 proposes that Deposit Product Providers be forced to provide open access to customer and small business data by July 2018. All four banks noted general support for data sharing. However, the banks are conflicted on this issue, as the process of opening up data means that an asset which is currently proprietary to the banks will be non-proprietary in the future. For this reason, it is critical that the banks are not allowed to control the process or set the rules by which consumer data is opened up. An independent body must lead the change and be responsible for implementation.

Recommendation 7 of the First Report proposes that there be an independent review of risk management frameworks aimed at improving how the banks identify and respond to misconduct. Each of the banks has responded claiming that APRA Prudential Standard CPS 220 performs this function. The Committee is not convinced that the CPS 220 risk management review process is sufficient in relation to misconduct. CPS 220 has a broad focus on the material risks to a bank. While these objectives are important for prudential reasons the Committee’s focus

in this Recommendation is the ongoing and serious nature of misconduct by the banks towards their customers. The Committee’s Recommendation will ensure that the banks give top priority to developing a risk management framework that truly puts customers first. This risk management review should work in parallel to CPS 220.

As part of the hearings in March 2017, the Committee scrutinised the banks over their use of non-monetary default clauses in small business loans. This matter was examined by the Australian Small Business and Family Enterprise Ombudsman, Ms Kate Carnell, as part of her inquiry into small business loans. Ms Carnell recommended that for all loans below $5 million, where a small business has complied with loan payment requirements and has acted lawfully, the bank must not default a loan for any reason. The Committee commends Ms Carnell on her important work on this issue and has recommended that non-monetary default clauses be abolished for loans to small business.

Here is an excellent piece from King & Wood Mallasons which puts their finger nicely on the key issues.

The House Of Representatives Standing Committee on Economics released its Major Banks Second Report in April 2017. Its ten recommendations largely repeat those contained in its first report and the Committee’s Chairman has called for each of them to be implemented.

We have used the heading of “Here we go again” as that is the truth: the majority of the recommendations represent another attempt at addressing issues identified by the comprehensive and properly considered Financial System Inquiry, but do little to address the underlying issues and take a simplistic approach to a complex industry. At best they will add further process and cost for little incremental benefit; at worst they will create further confusion and overlap between other legislative change and regulations.

Given the strength of the convictions and apparent political will, we think it is highly likely that many of them will be implemented. Some of the recommendations could be positive if they are implemented in a meaningful way. Our concern is that political considerations and expediency will force the opposite result.

In an attempt to more actively engage and shape the implementation of these recommendations, we have put forward our predictions and what you need to be aware of on the following recommendations:

A new focus on banking competition and making it easier for new banking entrants

Empower consumers (data sharing and use)

Independent review of risk management framework

Carnell Inquiry: Non-Monetary default

Now is the time to be conscious of these recommendations and understand the potential implications they may have.

“One-stop shop” EDR: the “Banking & Financial Sector Tribunal”

Recommendation: The Government amend or introduce legislation to establish a “one stop shop” Banking and Financial Sector Tribunal by 1 July 2017. This Tribunal should replace the Financial Ombudsman Service, the Credit and Investments Ombudsman and the Superannuation Complaints Tribunal.

Our prediction: This recommendation will be implemented, and with an increased monetary threshold for both claims and compensation. It is a practical solution to a key problem of the multiplicity of existing tribunals, and is inevitable given the government and industry positions in respect of them. However, it is still a work-in-progress, as the hard work of the design and detail of the one-stop shop has been delegated to the Ramsay review. The devil will be in the detail of what is suggested by that review.

What to watch for: Whether the recommendation solves the problem, and gets right the balance between pragmatism and legalism.

The interim report of the Ramsay review recommends that the claim and compensation limits under the existing EDR schemes be significantly increased for small business and consumer complaints. The Carnell report suggests a limit of $5 million. Ramsay currently recommends that the new EDR scheme be an industry ombudsman scheme, while the Committee recommends that it be a statutory banking tribunal. Consumer groups have also been strong advocates of a tribunal model. The difference is that a statutory banking tribunal is likely to have more comprehensive appeal rights, be more accountable and be more legalistic than an industry scheme.

In our opinion, an “all powerful” tribunal with higher limits and compensation thresholds will, by default, become more “legalistic” and some of the perceived benefits of the current EDR schemes, and their more informal and speedy processes and outcomes, will not be preserved. This could be an advantage for banks, as the appeal rights in relation to the existing EDR schemes are limited, and it is likely that more comprehensive appeal rights would be available for banks should a banking tribunal be established.

The consumer response to this change will need to be managed and positioned as a result of government policy which was supported by consumer groups, rather than as a result of a bank’s behaviour toward the tribunal.

Senior executive/manager regime

Recommendation: That, by 1 July 2017, the Australian Securities and Investments Commission (ASIC) require Australian Financial Services License holders to publicly report on any significant breaches of their licence obligations within five business days of reporting the incident to ASIC, or within five business days of ASIC or another regulatory body identifying the breach.

Our prediction: The problems to solve include culture and enforcement. These are inextricably linked. The proposed solution will not address either problem and could worsen them. It is simplistic, takes no account of the strong systems in banks, currently overseen by APRA, and will have at least two unintended consequences:

first, the time period for disclosure could result in a fast but wrong decision which in turn creates a culture of non-disclosure for fear of an arbitrary outcome or the prospect of being a “scapegoat”. Further, a “significant” breach will require investigation and often systems based responses which take time to investigate and develop – customers and shareholders will be prejudiced if a thorough review and response is compromised;

second, the statement in the recommendation that the CEO-level reports within a bank have the greatest capacity to change the culture shows a lack of understanding of the banking industry and the scale of each bank division’s operations, as a “CEO-level” report is basically the CEO of each of those divisions. The problem can only be fixed by changing the culture through the entire bank, with a focus on training, education, accountability and reporting systems. Senior management can set values and oversee systems and processes, but implementation errors will often not be obvious until the issue is spotted. Speedy escalation of the issue needs to be supported and not feared.

What to watch for: The balance between culture and enforcement.

In terms of culture, banks recognise that they need to address issues in their culture and rebuild trust with the public, and that one element of doing so is to ensure that breaches are identified, reported and acted upon and that bad behaviour has consequences, at all appropriate levels. There have been failures to do this in the past that cannot be repeated.

To do so, a culture of disclosure rather than a culture of fear needs to be created. People within banks at all levels need to feel safe to report a problem by having a supportive environment in which possible breaches can be reported, assessed and actioned, not an environment where they are afraid to do so because of arbitrary standards, a time frame which could result in the wrong decision being taken or where there is the risk of adverse publicity which is not warranted by the underlying circumstances.

In terms of enforcement, the solution of a senior manager regime will create a problem of duplication between this regime, ASIC’s current powers to penalise behaviour of senior office holders under the Corporations Act and APRA’s current powers under the fit and proper person regime. Which will have priority? How will competing claims between regulators and the courts be managed?

In our opinion, the better solution is to improve these existing laws and clarify and coordinate their enforcement – and actually use them – rather than creating a further set of laws that will not solve the problem and will likely cause further cost and complexity for the industry for little additional benefit, and distract banks from their priority of serving customers’ needs.

For this sort of regime to be workable and fair, there needs to be a tiered approach of notification, an appropriate time to investigate and then reporting of the proposed action to be taken and the involvement of management. Given the draconian consequences, our view is that these proposals will inevitably lead to a conservative view being taken of what is a “significant breach”, which will not be much different to the current regime. An approach which encourages and rewards the reporting of breaches, and building a strong relationship between the industry and the regulator, is more preferable and would go further towards solving the current problems.

A new focus on banking competition and making it easier for new banking entrants

Recommendation: that the Australian Competition and Consumer Commission, or the proposed Australian Council for Competition Policy, establish a small team to make recommendations to the Treasurer every six months to improve competition in the banking sector, and suggest any changes required to improve competition.

Our prediction: The recommendation is a triumph of process over substance that may not deliver any tangible results or achieve any significant change in levels of competition.

What to watch for: Political pressure driving further bad policy and another unwarranted inquiry into the banking industry.

“Competition” is a motherhood problem that always generates a motherhood statement: while everyone will always say that they want more competition, and will welcome more competition, the real questions to be asked and answered are:

What is improved competition? Is it more banks, or increased competition between existing banks or both?

How will improved competition be achieved? Will it involve legislative reform to lower barriers to entry and expansion, or to increase demand-side power or will the other reforms, including those directed at changing culture in the banking sector, achieve the underlying objective?

How should the increased competition be measured? Should it be measured in increased productivity, or increased consumer welfare, or reduced profitability?

In the fuel sector, the ACCC claimed that “shining a light on petrol prices” improved competition. But, is there any enduring evidence to support this?

To solve the problem, we think that the government needs to take a holistic view of the future banking industry, not tinker with the current. That is:

first, reduce the barriers to entry by creating a more supportive environment for new entrants and start-ups (including a UK style “two stage” licensing system for new entrants) as well as reviewing the APRA process for licensing and prudential regulation to achieve a better balance between APRA’s obligations to promote stability and competition as well as different capital applications for different sized lenders (as the US is moving towards, and as the report contemplates);

second, reduce the height of those barriers in terms of access to customer data, portability of customers, prudential requirements and infrastructure costs; and

third, recognise that the new suppliers are less likely to be traditional financial institutions but rather technology companies which both have and need access to data (such as Amazon, Google, Alibaba, Apple) and that a regulatory environment that both encourages their entry into the Australian market while preserving the ability of the current suppliers to access capital and funding is the best way of ensuring better long term competition in the Australian market.

One thing is certain. Access to foreign debt capital is critical for the Australian Banking system and the cost of that capital directly affects the cost of mortgage loans to mums and dads. The Government needs to tread very carefully here.

Therefore, a comprehensive and well thought through, holistic solution to all of these related issues is required, not a further series of knee jerk reactions that will never be implemented or, if implemented, will not solve the problem of improved competition.

Empower Consumers (data sharing and use)

Recommendation: that Deposit Product Providers be forced to provide open access to customer and small business data by July 2018. ASIC should be required to develop a binding framework to facilitate this sharing of data, making use of Application Programming Interfaces (APIs) and ensuring that appropriate privacy safe guards are in place. Entities should also be required to publish the terms and conditions for each of their products in a standardised machine-readable format.

The Government should also amend the Corporations Act 2001 to introduce penalties for non-compliance.

Our prediction: While we are still waiting for the Federal Government’s response to the final recommendations of the Productivity Commission on data availability and use, our prediction is that a new regime of open data for consumers and small business is inevitable. This train has left the station. The only questions are what model will be implemented and how it will be implemented.

What to watch for: These recommendations bring the questions of data “front and centre”. Data is the current and future asset of value in the industry. However, there are two critical aspects to this:

first, the recommendations are in several ways inconsistent with (or critical of) the approach taken by the Productivity Commission in its draft report. We need one model that reflects the culture and values of the Australian industry and consumers; and

second, competition cannot be improved without a solution to the questions of: who owns the data; how will it be secured; who can access it; how is that access provided; how is privacy maintained; who is accountable and who bears the risk if the data security is lost?

A key challenge for the industry is that a customer-centric model of open data may not be fully consistent with the industry’s business model or needs, and that the industry’s role in developing that model will need to be carefully managed given the range of stakeholders’ interests in play.

Independent review of risk management framework

Recommendation: that the major banks be required to engage an independent third party to undertake a full review of their risk management frameworks and make recommendations aimed at improving how the banks identify and respond to misconduct. These reviews should be completed by July 2017 and reported to ASIC, with the major banks to have implemented their recommendations by 31 December 2017.

Our prediction: This will be implemented as it is a no-brainer for the government. At least it doesn’t require a “culture audit”. It provides a customer, not a prudential, framework for the risk management of conduct. However, the time-frame will need to be longer: all banks have existing detailed risk framework and processes which need to be taken into account.

What to watch for: Will it solve the problem? No, as a review alone will change nothing. It needs to be seen as part of the solution to the culture and enforcement problem (described above) and to assist a bank in reviewing and making wider changes to its organisation and behaviours that will help it to drive a different culture. Nothing is gained by simply reviewing the current systems, or just creating a new penalty or threat for employees.

A review of this nature needs to be undertaken by an independent party that genuinely understands the banking industry, its consumer products, its current legal framework and regulation and the current steps being taken by the banks to reform their systems of culture, incentives, accountability and enforcement. It needs to be part of the solution and assist a bank in making these wider changes to its business.

Carnell Inquiry: Non-monetary default

Recommendation: That non-monetary default clauses be abolished for loans to small business. If the banks do not voluntarily make this change by 1 July 2017 then the Government should act to give effect to this Recommendation.

Our prediction: The recommendation will solve the perceived problem of allowing a lender to enforce for a non-monetary default, and this is already being actioned by the industry. However, it will simply create a different problem for a customer: the term of a loan could be shorter (say, between 12 months and 3 years) and be charged at a higher interest rate, as the recommendation transfers more risk to the bank. So a customer could get less certain and more expensive credit as a result.

What to watch for: The problem is said to be one of unfairness, in that a lender should not be able to default a loan except if the borrower has not paid interest or principal on time. A non-monetary default gives too much power to the lender to take action even when a customer might be making those payments on time.

The reality is that there are too many non-monetary default provisions, and they can be simplified. They are also rarely, if ever, used. However, they underlie the relationship between the bank and the customer, and in some cases reflect prudential risk management requirements on the bank and give each of them a catalyst to discuss improvements to the customer’s business that may increase its ability to pay or the adequacy of the security given to the bank for the loan, rather than calling a default. Banks currently use non-monetary default provisions as “early warning signs” to enable banks to meet the risk requirements imposed by prudential regulation and work with customers with deteriorating businesses to turn them around before customers commit monetary defaults.

The balance between the term of the credit (more than 12 months to give certainty of funding to small business) and the terms of the credit (to allow banks to monitor and manage their exposures, and ultimately their capital) needs to be fair between them and put into the right balance.

What now?

The next few months are critical, as not only the Committee but many commentators are calling for implementation of these recommendations. A firm but fair approach by the banking industry, which recognises its issues to be addressed which is accompanied by meaningful suggestions, is required to all stakeholders.