According to Moody’s, the US equity market can help divine the path to be taken by the high-yield default rate. However, changes in the market value of US common stock are not the equity market’s primary channel of

prediction. Rather, the VIX index, which estimates the implied volatility of the S&P 500 stock price index over the next 30-day span, offers the more reliable guide to where defaults may be headed.

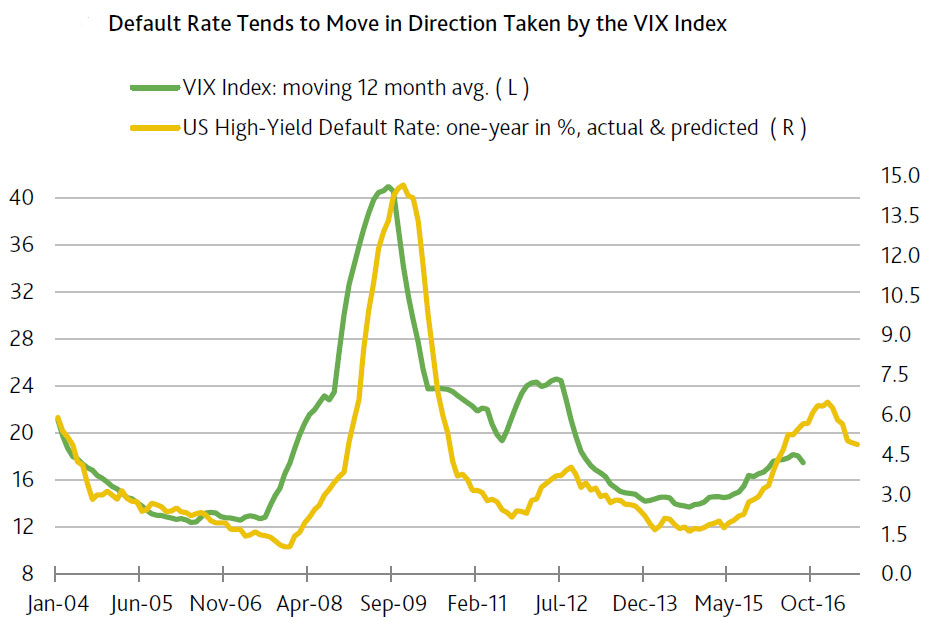

The VIX index estimates the equity market’s expectation of stock price volatility. As the market becomes more worried over a possible deep sell-off of equities, the VIX index rises. By itself, such fear may reduce financial market liquidity, including the willingness to lend to high-yield credits.

The uncertainty that drives the VIX index higher often stems from signs of an extended stay by weaker corporate earnings. Significantly lower earnings, if not outright losses, will increase defaults among more marginal business credits. Downwardly revised earnings prospects, more frequent defaults, and heightened equity market volatility can only boost risk aversion and, thereby, diminish systemic liquidity.

These adverse developments will add to the difficulty of raising cash via asset sales and will lessen the willingness of healthy companies to purchase financially stressed businesses.

Since year-end 2003, the high-yield default rate has generated a very strong correlation of 0.91 with the moving yearlong average of the VIX index from three months earlier. As opposed to an average measured over a shorter span, the VIX index’s moving yearlong average helps to explain the default rate partly because the default rate is measured over a yearlong span.

As derived from a regression model, the VIX index’s latest moving yearlong average of 17.2 predicts a midpoint of 2.9% for the high-yield default rate of three months hence. Though few, if any, expect the default rate to sink from its recent 5.5% to 2.9% three months from now, the VIX index’s recent trend weighs against an extended climb by the default rate that might distend the already above-trend yield spreads of medium- and speculative-grade corporate bonds.

Nevertheless, the VIX index’s predictive power might now be criticized on the grounds that it has been skewed lower by expectations of a prolonged stay by a very accommodative monetary policy. The equity market may have concluded that the FOMC will not dare risk a deep slide by share prices that could slash confidence and diminish liquidity by enough to bring a quick end to the current business cycle upturn. A recent ultra-low VIX index of 12.1 points suggests that the equity market is supremely confident of monetary policy’s willingness and ability to quickly remedy a potentially disruptive slowdown by business activity.