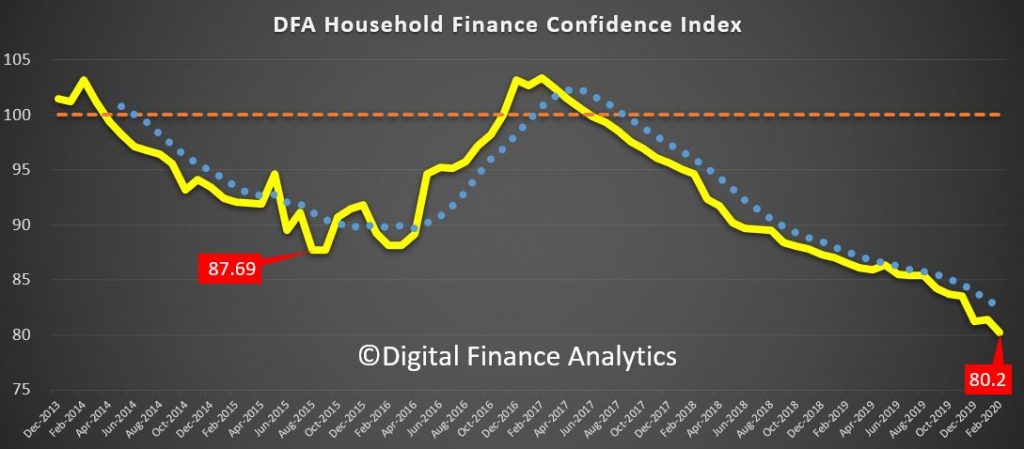

The latest data from our household surveys to the end of February 2020 shows that the impact of Covid-19 are hitting home. The index dropped again, into uncharted territory, to an all time low of 80.2. I even had to change the scale of the chart to accommodate the fall!

We ask households to compare their levels of confidence today compared with a year back across a number of dimensions, from job security, income, costs of living, debt, savings and overall net wealth (assets less debts). This gives us a comparative series from the 52,000 households in the rolling sample.

Households are reacting to the uncertainty about the future trajectory of the economy, and recent survey results (we run a rolling series to the 5th March), have captured recent stock market falls. The falls are broad based, though households with a property remain relatively more positive, believing that property remains largely immune – we will see.

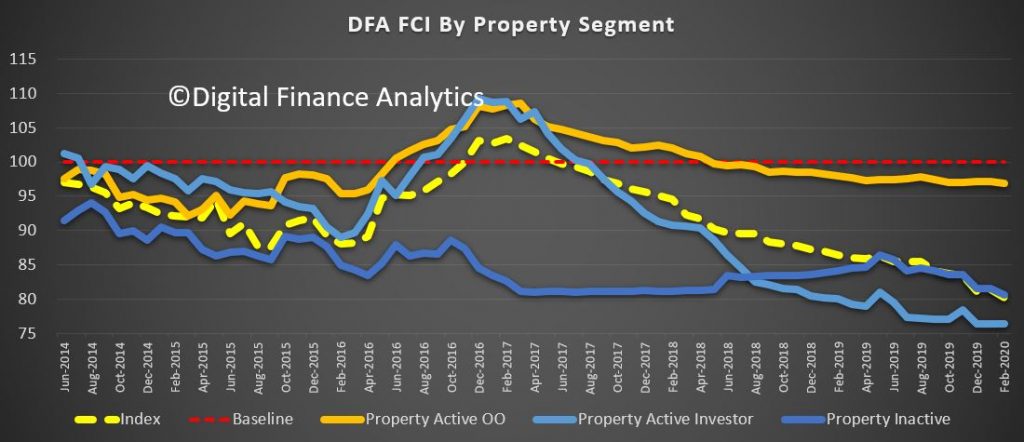

Within the property segmentation, property investors are on the mat now, as rentals continue to grind down, and property values especially among units have not recovered as much as the generic indices may suggest. Households renting are finding more choice, and lower rents in a number of centres (Hobart excepted). Supply is quite strong.

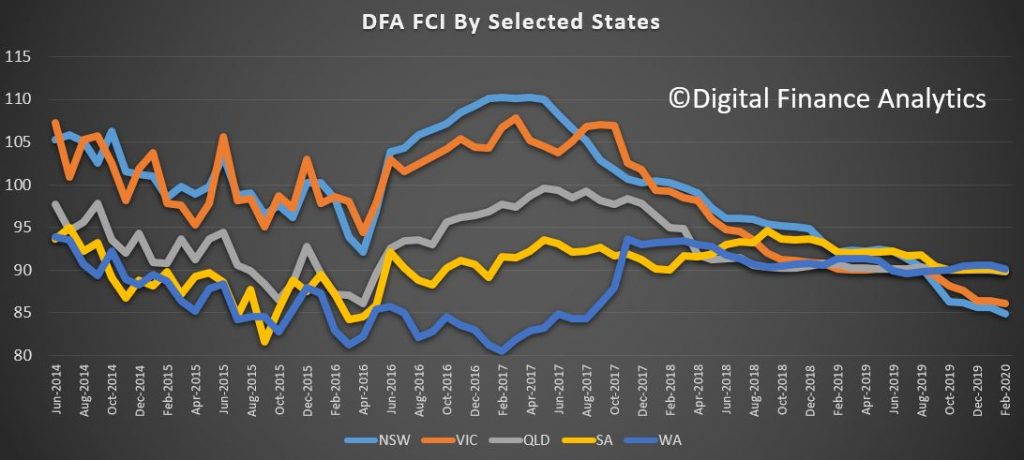

Most states moved lower, with NSW and VIC taking quite a hit this past month. NSW at 84.9 is the lowest scored state now, thanks to the higher debt leverage there where large mortgages predominate. WA, QLD and SA are bunched higher at around 90.

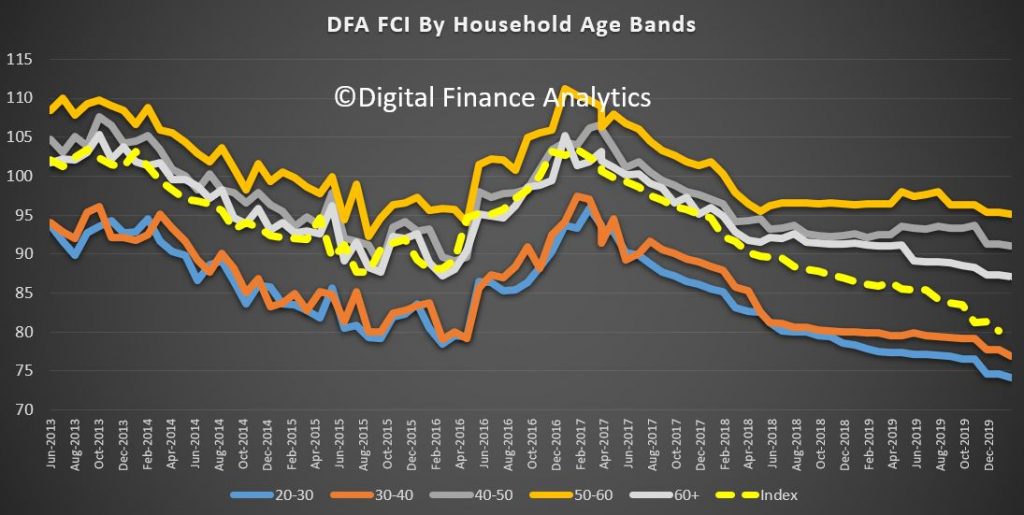

Across the age bands, we see falls across the board. The financial pressures on younger households of 20-30 and 30-40 are piling up as they continue to feel the issues most severely, older households are buttressed a little more by share portfolios (which are falling) and savings (where rates are falling). But all ages bands fell this month.

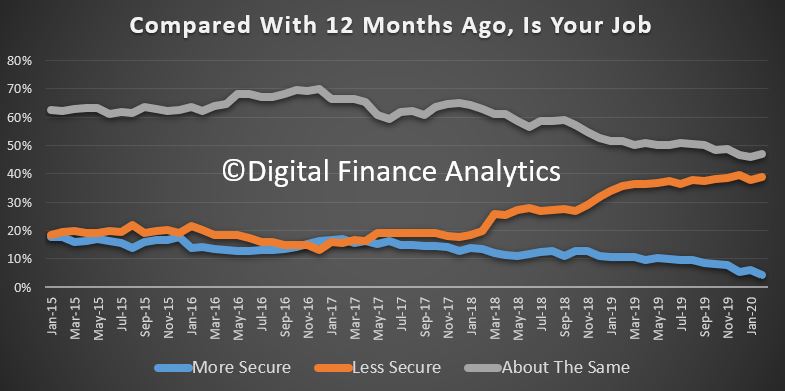

Within the index we can look at the elements which drive the scores. Job security slid 1.66% compared with last month with just 4.3% saying they feel more secure than a year ago. 38% feel less secure, an increase of 1.1% from last month, and 47% about the same. The full potential impact on jobs has yet to be absorbed by the community, but around 3 million are working in gig type “flexible” roles. And others will be “encouraged” to take leave to try to stem cash flow issues among businesses.

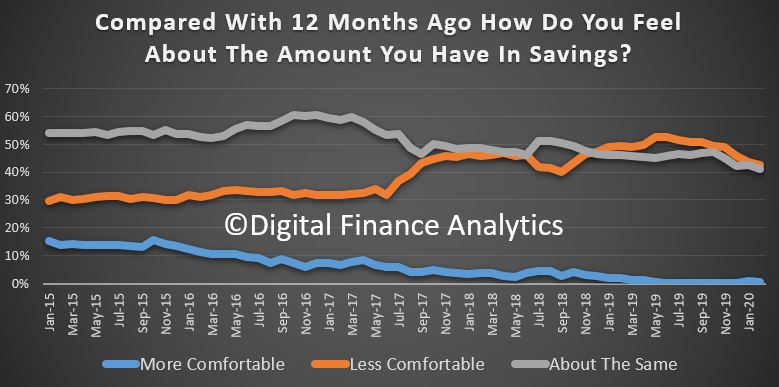

Households are taking a beating on savings at the bank, with rate cuts eroding returns to the point many households are not getting enough income to cover the basics. And the stock market is off (and falling as I write), with the supply side shock of the virus now translating to a potential liquidity crisis. Safe havens are hard to find for the fortunate few who have savings. Many of course have none and live from pay credit to pay credit.

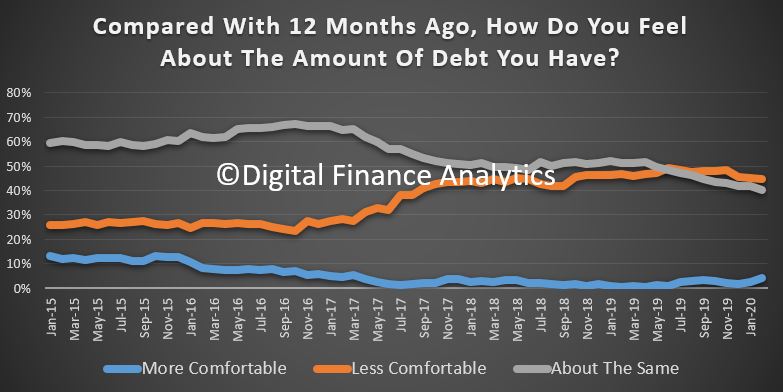

The cost of debt is falling, so many are seeking to refinance (again) to grab the lower rates available to some. However, only 4.2% are more comfortable with their level of debt compared with a year back, and of course if income from employment falls, paying the mortgage becomes a nightmare. 42.5% are less comfortable than a year ago. Those who recently obtained new mortgage finance appear to be in for the biggest shock thanks to looser underwriting standards of late.

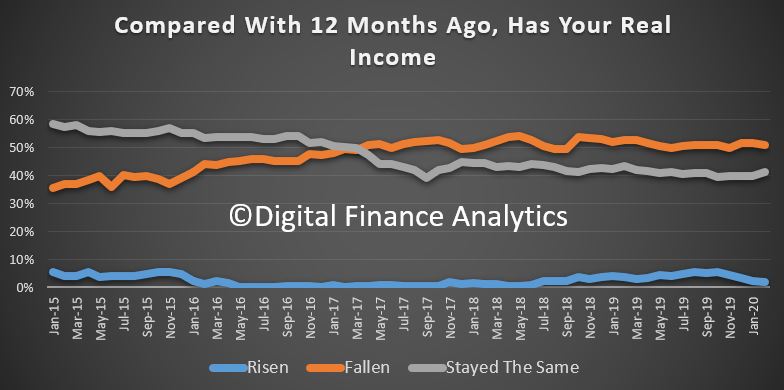

Pressures on incomes remain centre stage with just 1.7% of households saying their real incomes have risen in the past year. More than half of households have seen their incomes fall in real terms over this period, and 40% see no change. Incomes will evaporate for many should the supply side shocks continue.

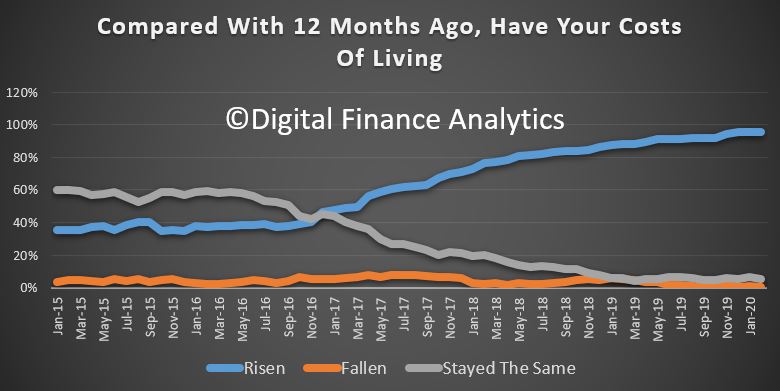

Costs of living on the other hand continue to bite, with more than 95% of households reporting rising costs over the past year. 5% reported no change, almost no households reported they had fallen. Categories of costs which are impacting including the usual suspects, from energy, fuel, child care and health case costs, plus council rates. But the most insidious are those relating to everyday expense at the supermarket, where drought related hikes abound. The falling exchange rate is also hitting some imports and making them more expensive. Around 25% of households have less than 1 months cash available to meet their commitments if they income seized up.

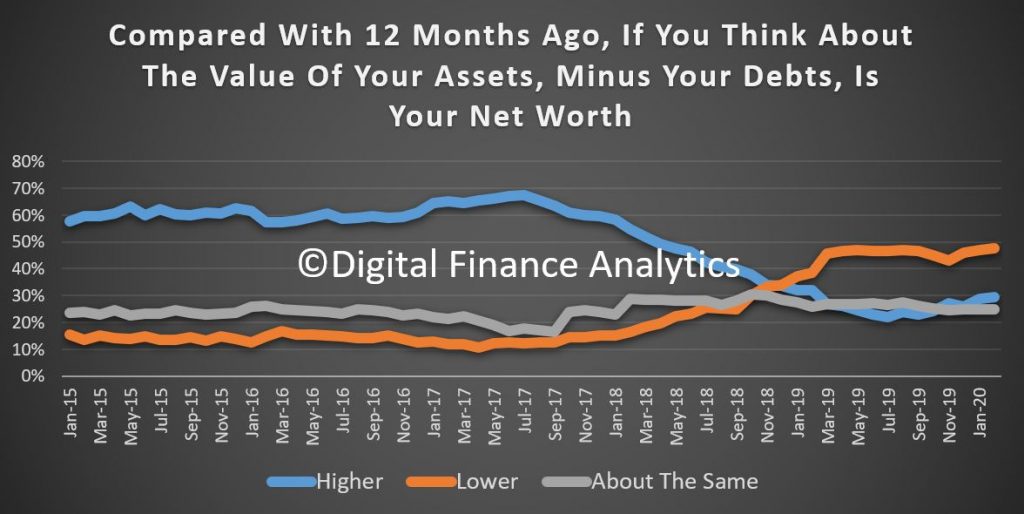

Yet, overall, the net worth of households improved slightly, with property values higher in a number of locations, though recent stock market falls are dragging wealth down for some.

The big strategic question now is whether the Government understands the true significance of what is happening. Whilst they are talking up a $10 billion package, it appears to be shaping towards investment allowances and other tactical measures. In fact, the level of confidence we are recording in our surveys suggests that households will not be able spend (consumption being a significant share of the economy) and many small businesses will struggle to employ, yet alone survive. The quantum they are discussing is too little too late. I expect confidence to erode even more as things play out and the true horror the economic predicament we are in hits home. And then the following financial crisis also strikes.