The RBA and APRA both released their data for March today. There were some pretty shocking movements, which reflect only the very early stages of the virus impacting the economy.

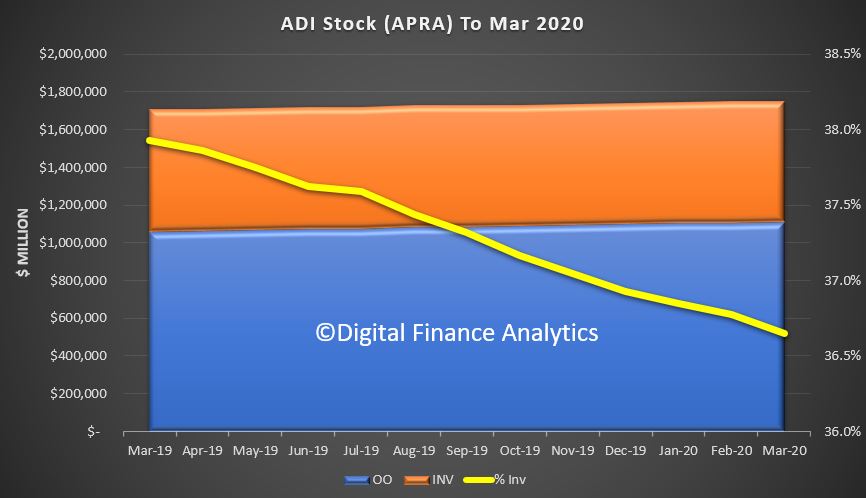

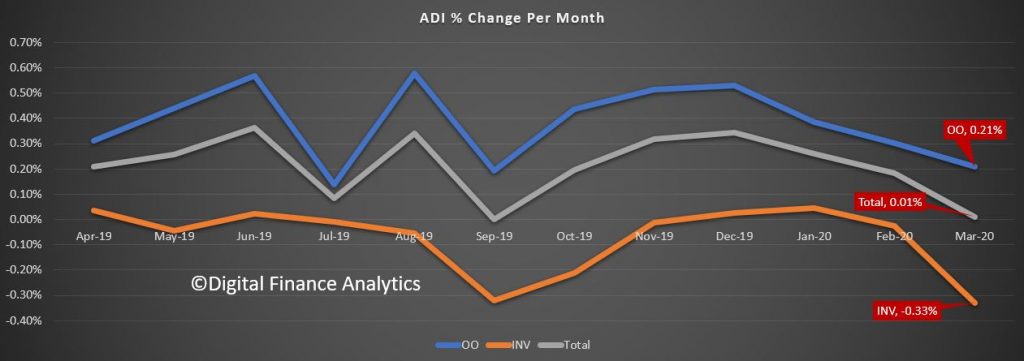

Looking at the APRA data first, total credit for home lending rose overall by just $193 million dollars, up 0.1%, the smallest rise for many months. Within that, lending for owner occupation rose $2.3 billion to $1.10 trillion up 0.21%, while lending for investors fell 0.33% down $2.1 billion to 0.$64 billion. Investment mortgages fell to 36.8% of all loans, and continues to track lower. This is a combination of more households paying down, and slowing new loans.

The monthly trends are tracking lower.

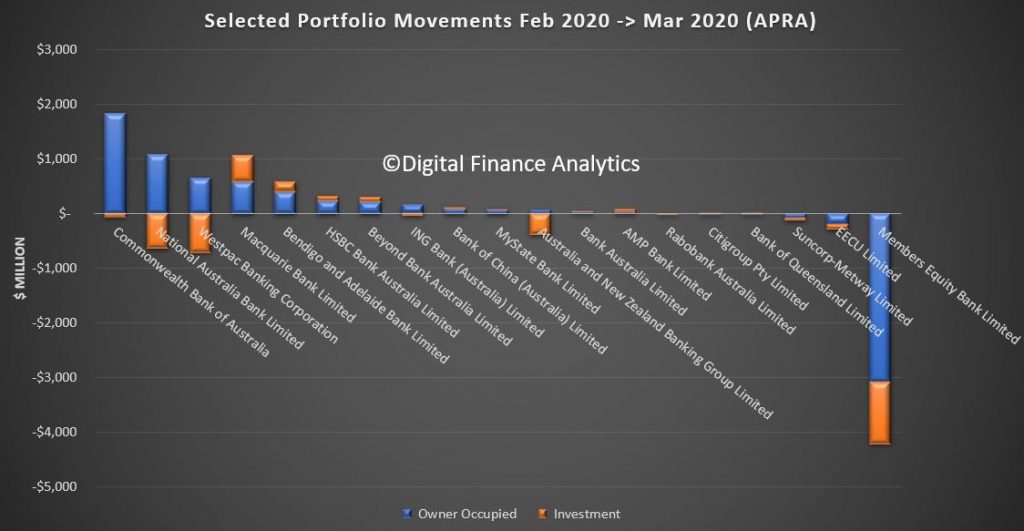

Looking at the individual players, we see some different outcomes, with Macquarie still growing their owner occupier and investment portfolios, while the majors are shrinking their investment portfolio, will expanding owner occupation. We includes a selection from the long list. The standout is ME bank who dropped the value of both their owner occupied and investor lending. This is because they securitised a significant mortgage pool, and so those loans no longer show on the ME Bank APRA return. The usual caveats apply, this is based on data as received by APRA, and may not be complete.

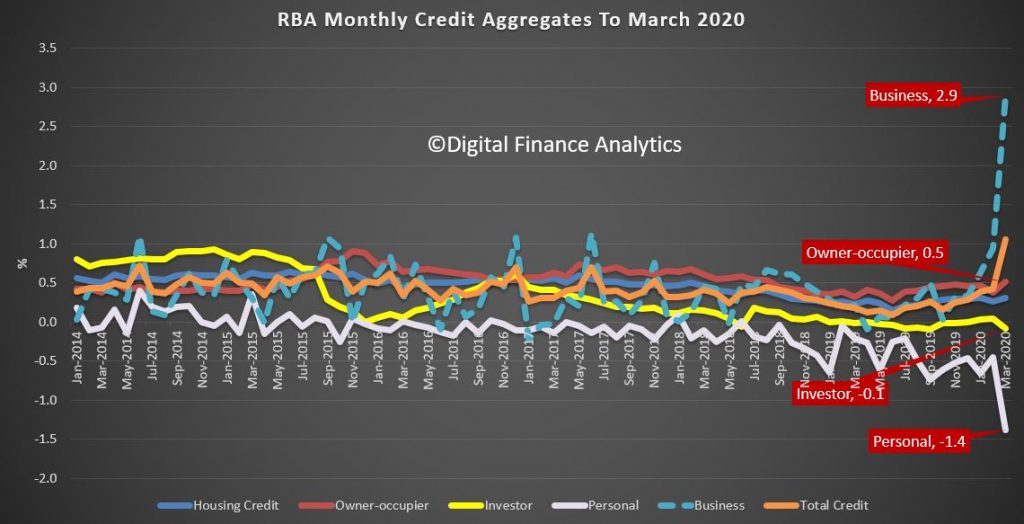

Turning to the RBA data, the monthly trends showed a large spike in business lending in March, as firms drew down on their existing credit lines. Business rose 2.9%, while personal credit fell 1.4%, owner occupied loans rose 0.5% and investor loans fell 0.1%.

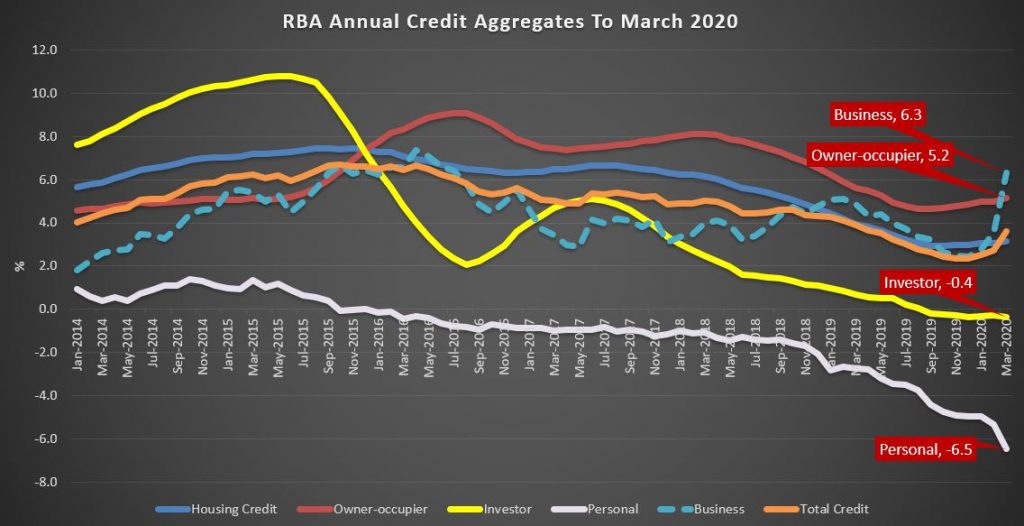

The March data represents the largest monthly rise in credit across the private sector since December 2007, before the GFC. The annual rate of business credit growth moved up to 6.3%. Lending for owner occupied borrowers sat at 5.2% annualised, while investment lending was 0.4%. Personal credit was down 6.5%.

Ahead the impact of the economic slowdown will continue to hit the credit numbers. Some businesses will start to cut costs and reduce inventory, which may reduce their need for credit, while JobKeeper payments will start to flow, but not until May, so we should expect more business lending. House purchases have slowed to a crawl, so demand for new mortgages will be off, though refinancing to lower rate products is likely to continue.

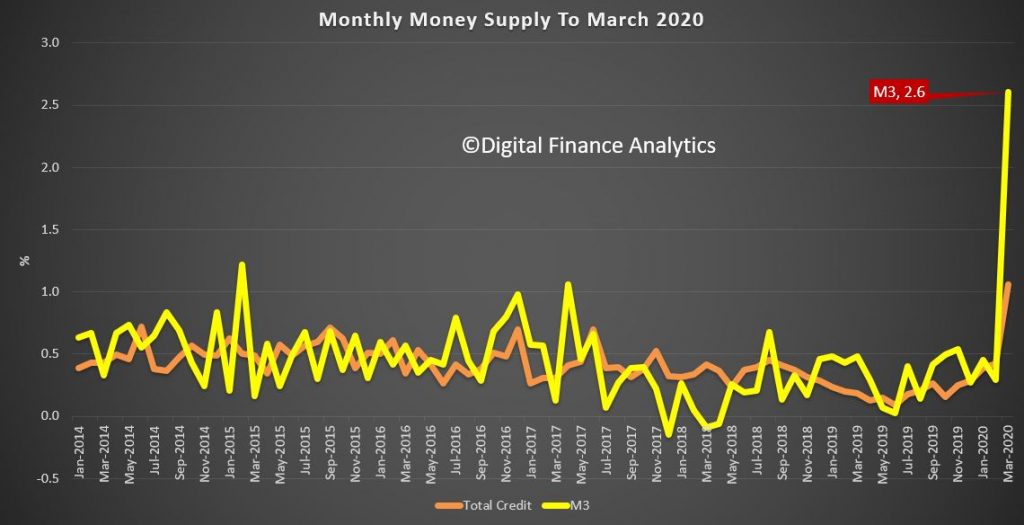

Finally, it is worth noting the jump in money supply, as a result of the various schemes launched. Growth in M3 was 2.6% – and strongly maps to the increase in business loans. Banks will benefit from higher interest charges as a result.