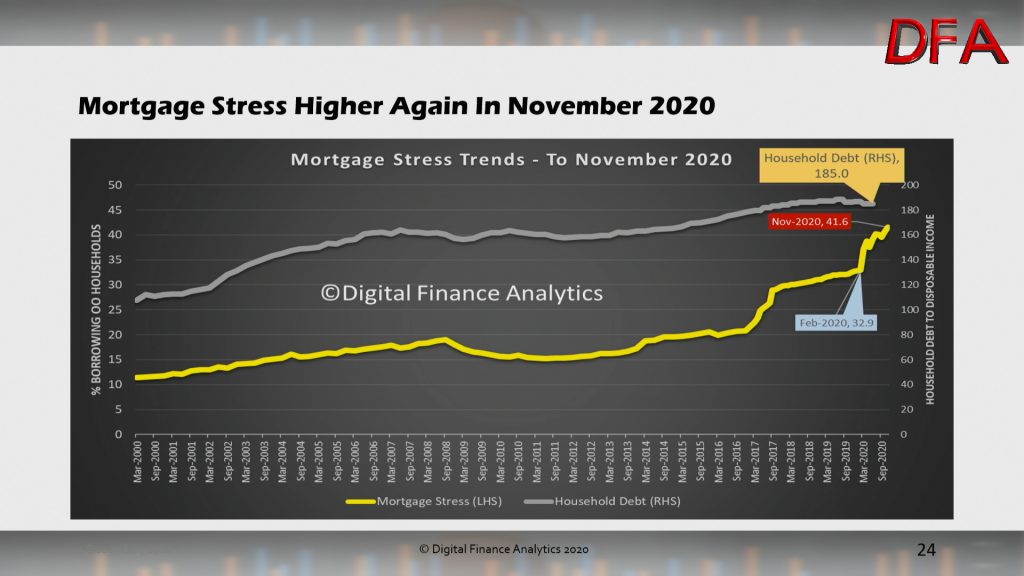

This was not meant to happen – after all the official story is we are in recovery mode – yet the latest results from our rolling household surveys tells another story as unemployment and underemployment rise further, even as Government financial support is tapered down. As a result mortgage stress – those households with a mortgage and cash flow pressures – rose to an astonishing 41.6% in November. Before the pandemic we sat at 32.9% in February, so nearly 10% more households are now feeling the pain.

The surveys showed some mixed drivers of this result. Sure, a number of larger firms have come off JobKeeper as the economy reopenes but more smaller firms are putting people on JobKeeper, even as the level of support is reduced. This was confirmed by the segmental analysis of the latest payroll data which showed growth among larger firms but a fall among smaller firms.

More households have had to recommence mortgage repayments now, with the ABA reporting that among the top 7 largest banks, deferred loans dropped from a peak of $250 billion down to $86 billion in November, with home loan deferrals by the seven largest banks are down to fewer than 145,000. But this has placed considerable pressures on households recommencing, even as unemployment continues to rise – to 7% in November according to the ABS and remember this is artificially understating the true picture as JobKeeper recipients are excluded.

The unemployment rate increased 0.1 pts to 7.0% (1.7 pts higher than a year ago)

Unemployment increased by 25,500 to 960,900 people (and increased by 238,900 over the year to October 2020)

The youth unemployment rate increased 1.0 pts to 15.6% (and increased by 3.1 pts over the year to October 2020)

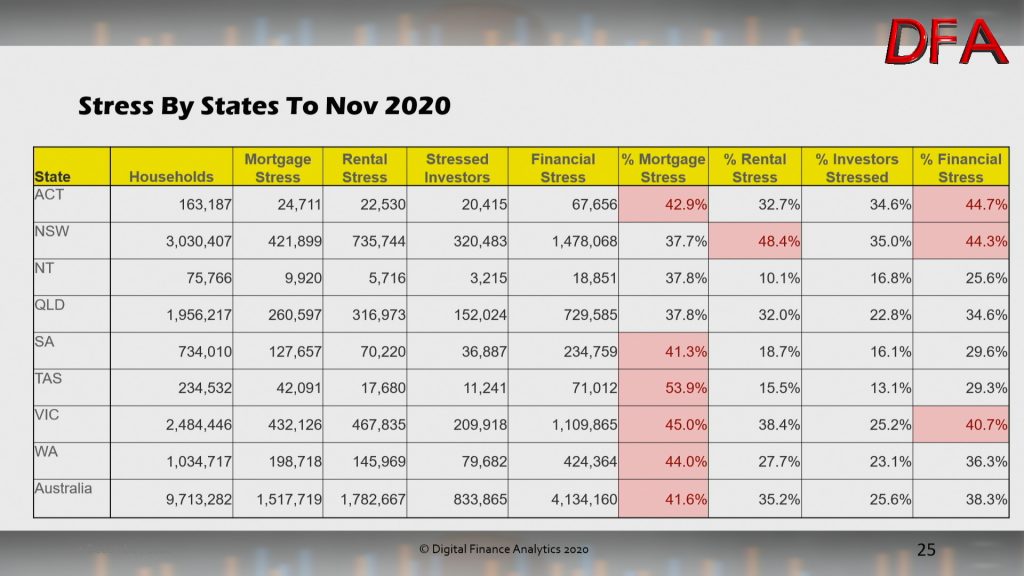

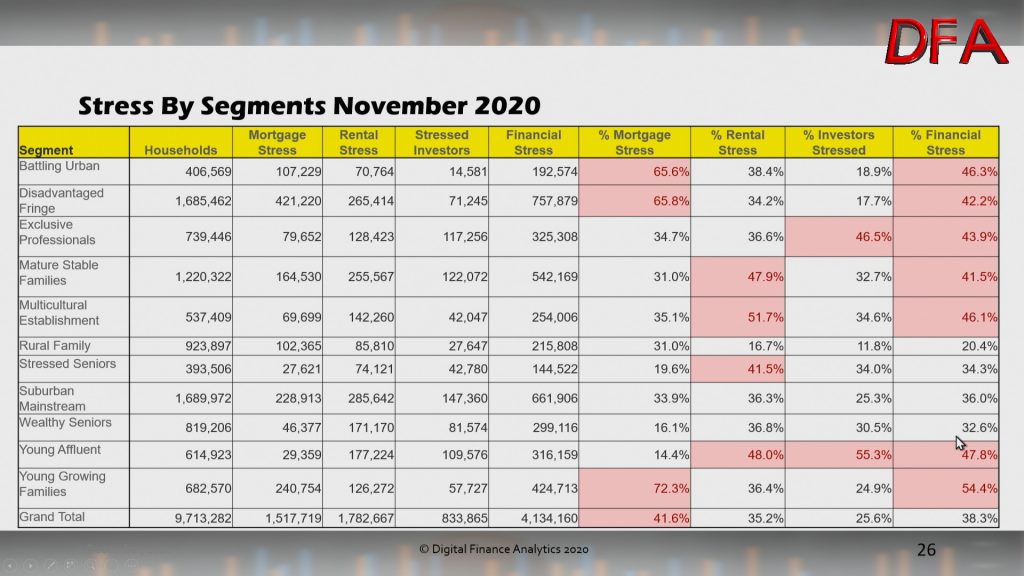

Our analysis also examines Rental Stress, Property Investor Stress and overall Financial Stress by state and household segment.

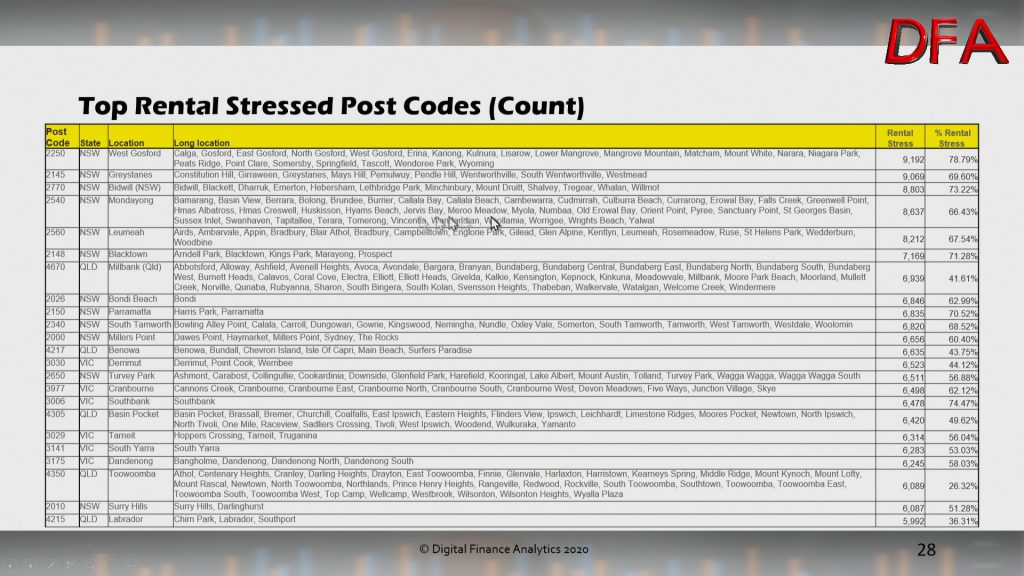

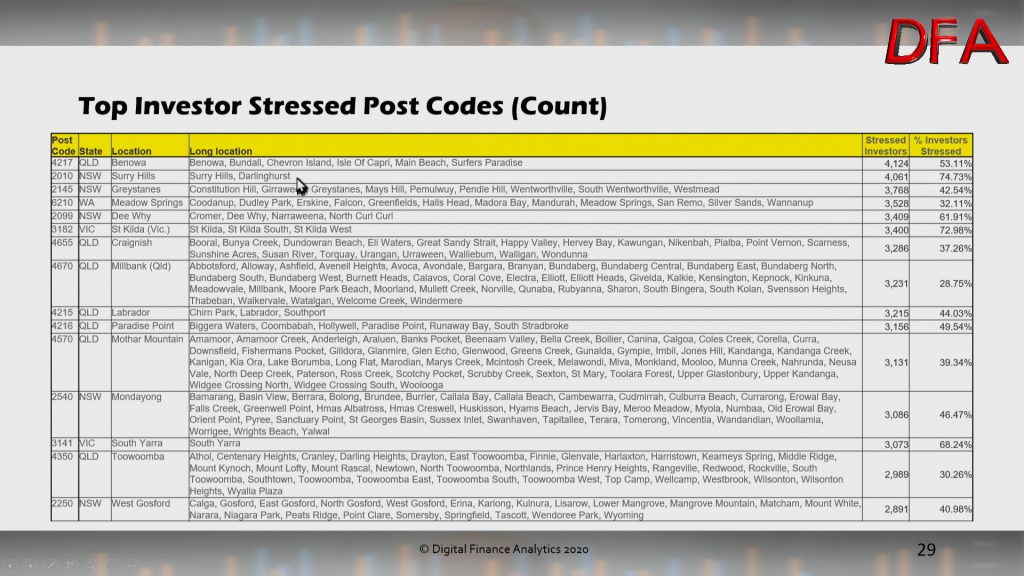

Across the states, Tasmania still retains top mortgage stress spot in in percentage terms, followed by Victoria and Western Australia. Rental stress is highest in New South Wales and Victoria, and across Australia. On average 35.2% of those renting have cash flow issues. Among property investors, 25.6% reported a cash flow deficit, as rents fall, and vacancies rise. More are still considering selling – especially those holding high-rise apartments in Sydney and Melbourne.

Across our segments, mortgage stress is highest among young growing families, which includes many first time buyers who were attracted into the market by Government incentives. This will not end well. Those living in the high growth corridors are also under pressure, especially on the urban fringe. And we see more affluent households caught up in stress, thanks to higher levels of unemployment – and high leverage.

Rental stress is broad based, with many first generation migrants under pressure, as well as young affluent.

Many affluent households with investment property are stressed, thanks to the proliferation of multiple properties, and high leverage, even as rentals fall in some areas. Once again, units are most exposed.

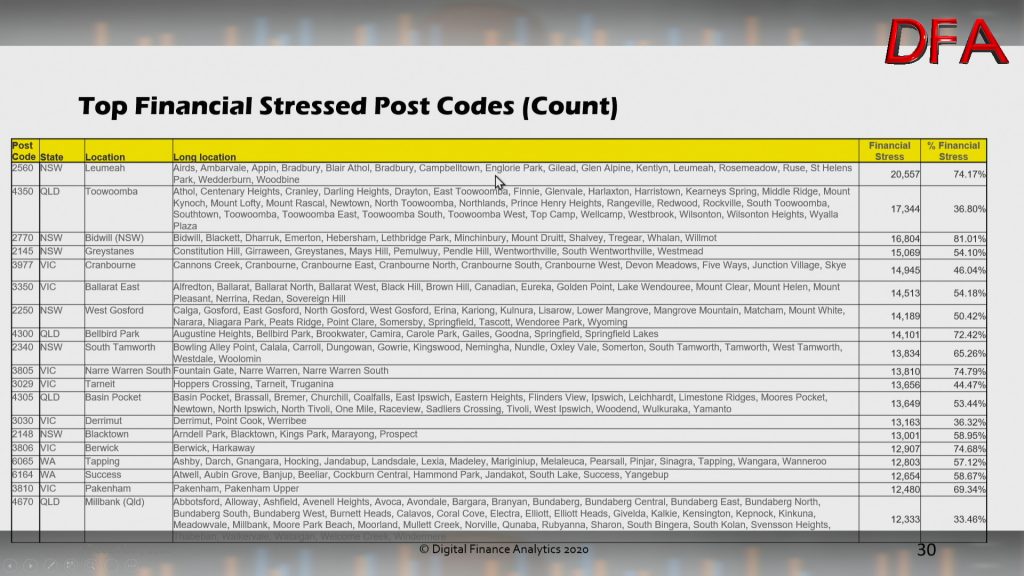

Overall financial stress (an aggregate of the three elements we discussed) is broad based across our segments. This is a significant structural issues – and one which was already in play BEFORE the pandemic. But it is significantly worse now.

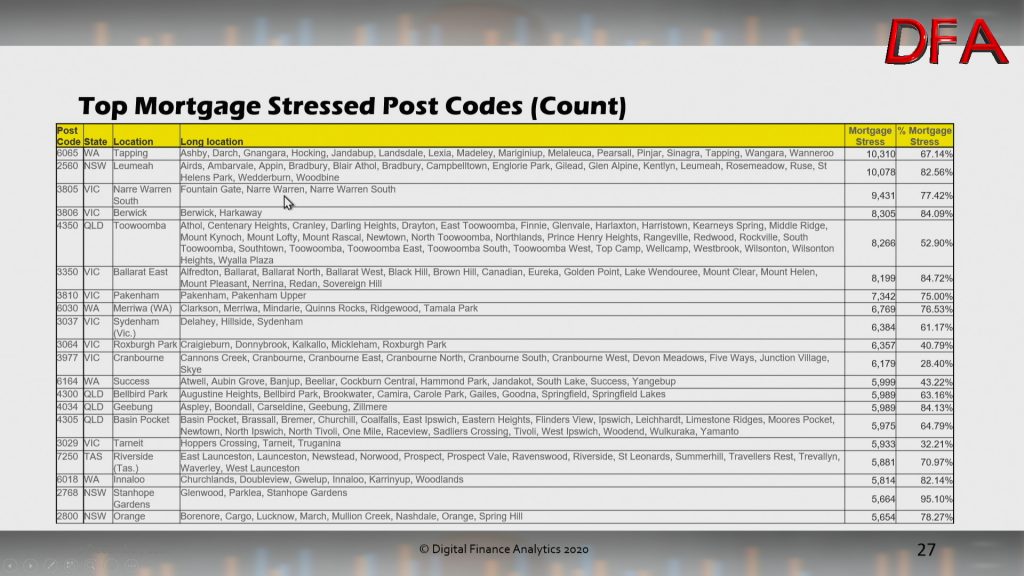

The top postcodes by mortgage, rental and investor stress are presented below. This data is sorted by the number of households impacted by stress (again in cash flow terms). We see high representation in high growth corridors across the country, as well as some inner City suburbs.

Investor postcodes show the location where the investor resides, not necessarily the location of their investment properties.

Overall financial stress is highest in the high growth corridors, areas where many households are under pressure, yet also areas where more development in under way and home land packages are being pushed very hard though the current Government schemes.

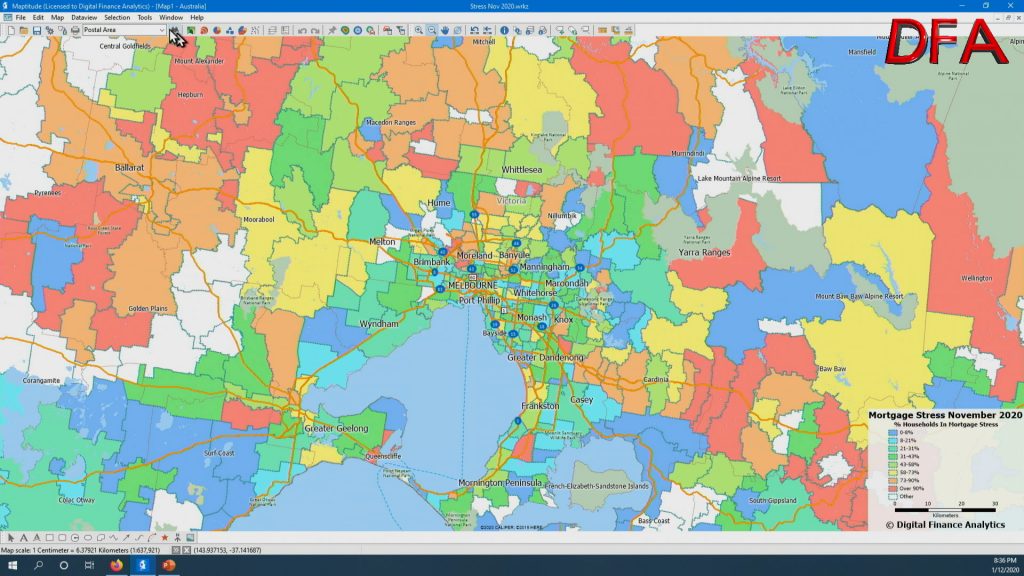

We also mapped the stress – here is an example of mortgage stress in Melbourne. This is to illustrate the patchwork nature of stress (orange and red are high stress areas).

Two final points, as Government support is wound back further, especially in the March quarter next year it seems likely stress will continue to bite, unless unemployment turns around faster than expected.

And as the ABA said recently

“Don’t wait till you are in over your head, talk to your bank, they’ll help you find a way through this. Don’t tough it out on your own”,

This is excellent advice, and should sound a note of caution to those who are considering a property move in the current environment. Mortgage stress can put considerable pressures on households, and often leads to a sale later. So new purchasers should be cautious, and develop their own cash-flows prior to committing – just because a lender agrees to make a loan, this does not necessarily mean its a sensible decision from a borrowers point of view – a bank has a completely different view of “risk”. So buyers beware!