The monthly data from APRA on the banks for September makes interesting reading. This month we will focus on the home loan story (cards and deposits being pretty much as normal). First the total value of home loans in the bank’s books rose by 0.84% to $1.388 bn (compared with a total market of $1,495 bn as reported by the RBA – the gap is the non bank sector). Among the ADI’s, owner occupied loans rose 1.48% to $856 bn, whilst investment lending FELL by 0.57% to $532 bn, and is 38.3% of all home lending. We saw a fall the previous month in investment loans of 0.75%, so investment lending continues to drift lower as the pressure from the regulators finally flows through.

Of course, the banks still need the mortgage lending drug, so they have switched to grabbing owner occupied refinance loans, and are discounting heavily now (thanks to the back book repricing they have shots in the locker).

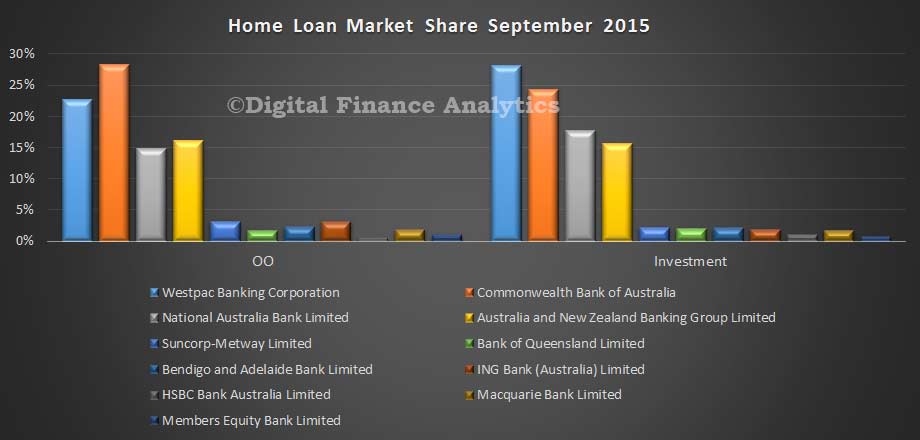

Looking at the bank specific data (and yes, we think the data is still noisy), the market shares in September look pretty similar, with Westpac still the king pin for investment lending, and CBA the champion of owner occupied loans.

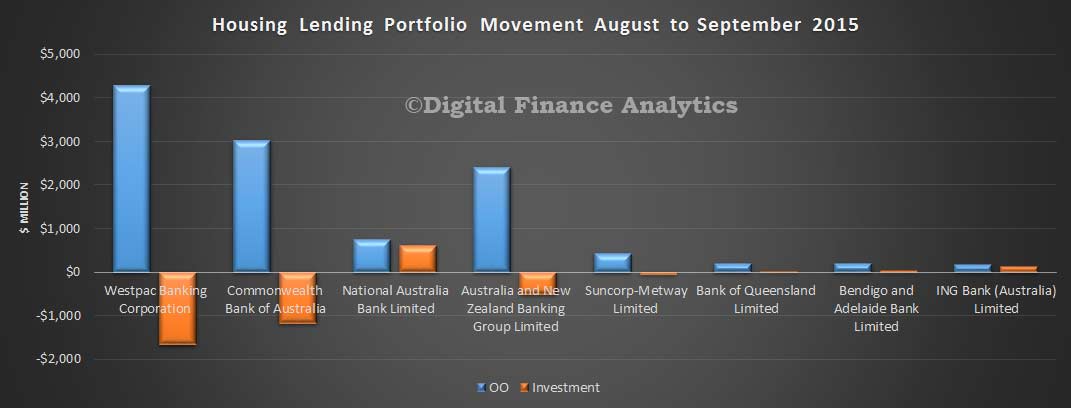

Looking at the portfolio movements though, from August to September, we see a significant swing at three of the big four, with Westpac, CBA and ANZ all dropping their investment loan portfolio a little, whilst driving owner occupied loans really hard. Suncorp also went backwards on investment lending. The focus is clearly owner occupied loans.

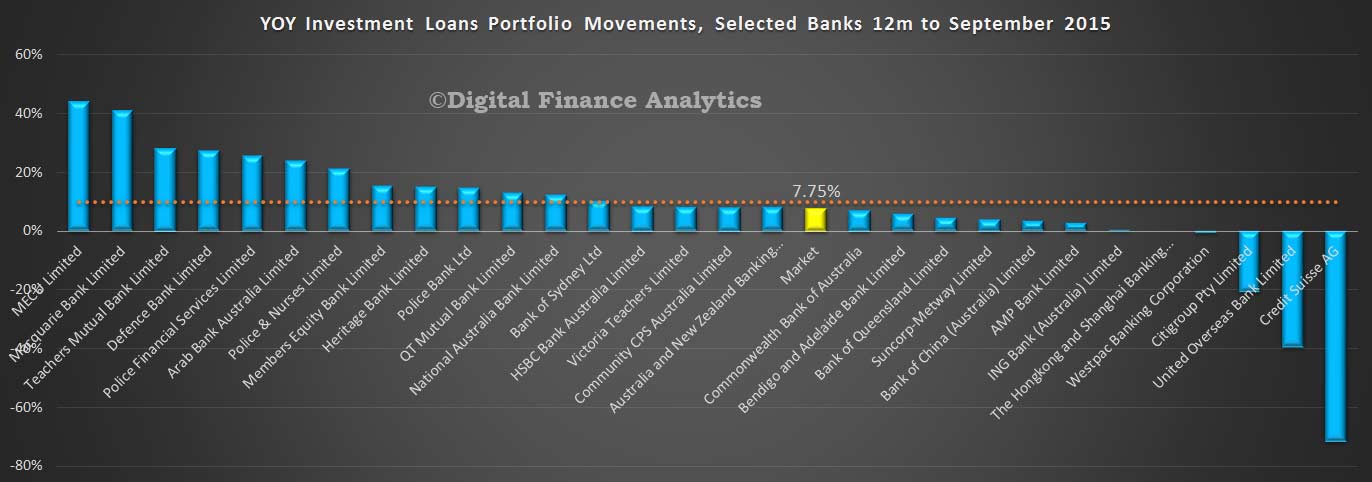

Looking at the 12 month moving data on investment loan portfolio growth, we see that some are still above the 10% speed limit, but several of the majors are now below the hurdle. The industry average is now at 7.75%. We expect it to fall further, because more banks will need to throttle back to keep their annual rates below 10%.

Looking at the 12 month moving data on investment loan portfolio growth, we see that some are still above the 10% speed limit, but several of the majors are now below the hurdle. The industry average is now at 7.75%. We expect it to fall further, because more banks will need to throttle back to keep their annual rates below 10%.

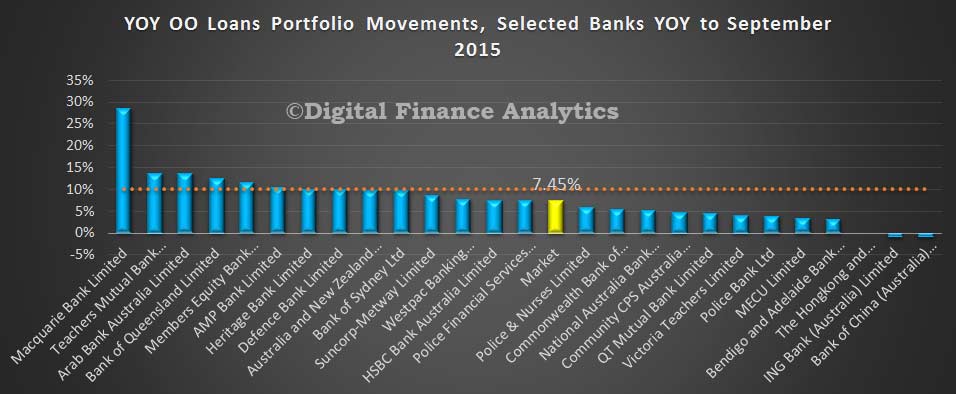

Growth in owner occupied loans is stronger now than it has been for some time. The market annual average is 7.45%, and we expect the rate of growth to continue to rise. This begs the question, at what point will the regulators decide to erect a speed trap on the owner occupied side of the ledger?

Growth in owner occupied loans is stronger now than it has been for some time. The market annual average is 7.45%, and we expect the rate of growth to continue to rise. This begs the question, at what point will the regulators decide to erect a speed trap on the owner occupied side of the ledger?

The deep discounting of new owner occupied loans more than offsets any price increases on the headline rates for existing borrowers. We do not think the RBA should cut rates, as this will just stoke owner occupied demand further.

The deep discounting of new owner occupied loans more than offsets any price increases on the headline rates for existing borrowers. We do not think the RBA should cut rates, as this will just stoke owner occupied demand further.