Virtual currencies (VCs) and especially their underlying technologies are a potentially important advance for the financial sector that could increase efficiency and financial inclusion, but can also serve as vehicles for money laundering, terrorism financing, and tax evasion. Achieving a balanced regulatory framework that guards against risks without suffocating innovation is a challenge that will require extensive international cooperation, says a new IMF staff paper, “Virtual Currencies and Beyond: Initial Considerations,” released by the International Monetary Fund (IMF) during the World Economic Forum.

The report provides an overview of virtual currencies, how they work and how they fit into monetary systems, both domestically and internationally. It discusses the potential implications of the technological advances underlying virtual currencies, such as the distributed ledger system, before examining the regulatory and policy challenges posed by VCs, in the areas of consumer protection, financial integrity (money laundering and terrorism financing), taxation, financial stability, exchange and capital controls and monetary policy. The paper also sets out principles for the design of regulatory frameworks for VCs at both the domestic and international levels.

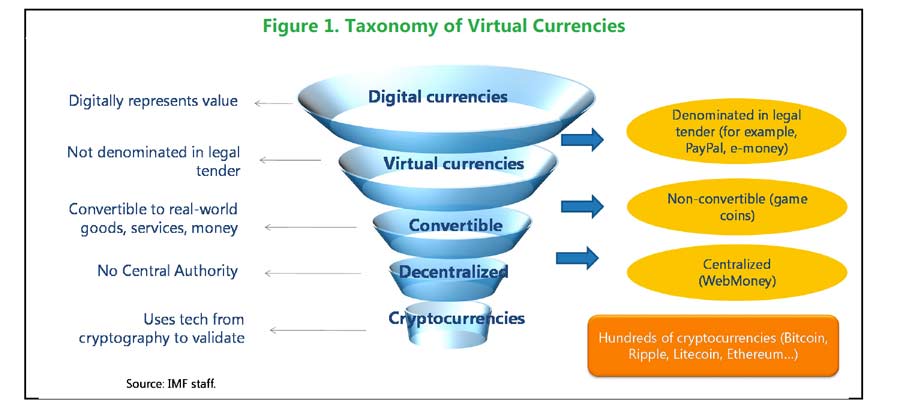

As digital representations of value, VCs fall within the broader category of digital currencies (Figure 1). However, they differ from other digital currencies, such as e-money, which is a digital payment mechanism for (and denominated in) fiat currency. VCs, on the other hand, are not denominated in fiat currency and have their own unit of account.

High price volatility of VCs limits their ability to serve as a reliable store of value. VCs are not liabilities of a state, and most VCs are not liabilities of private entities either. Their prices have been highly unstable (see Figure 2), with volatility that is typically much higher than for national currency pairs. Both prices and volatility appear to be unrelated to economic or financial factors, making them hard to hedge or forecast.

High price volatility of VCs limits their ability to serve as a reliable store of value. VCs are not liabilities of a state, and most VCs are not liabilities of private entities either. Their prices have been highly unstable (see Figure 2), with volatility that is typically much higher than for national currency pairs. Both prices and volatility appear to be unrelated to economic or financial factors, making them hard to hedge or forecast.

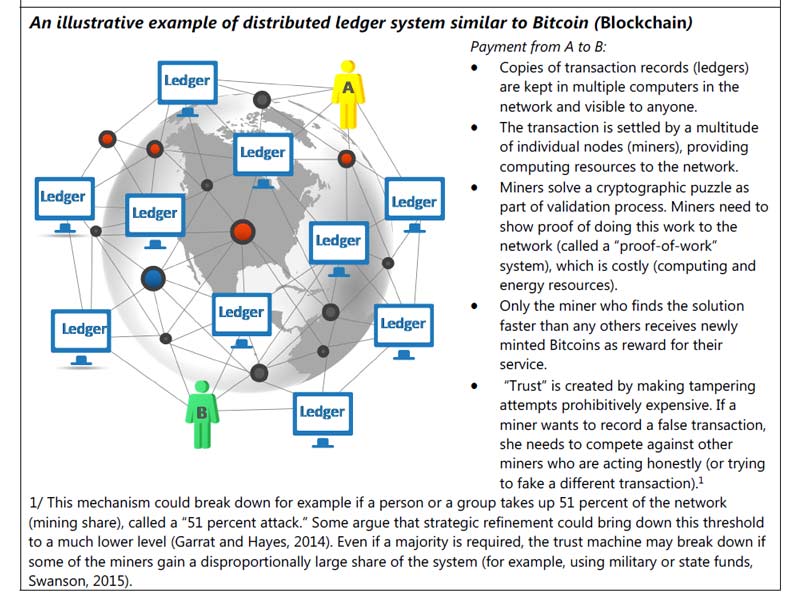

Computing technology has made possible decentralized settlement systems built on distributed ledgers distributed across individual nodes in the payment system. Centralized systems have a master ledger keeping track of transactions maintained by a trusted central counterparty. In a distributed ledger system, multiple copies of the central ledger are maintained across the financial system network by a large number of individual private entities. The network’s distributed ledgers—and hence individual transactions—are validated by using technologies derived from computing and cryptography, most often derived from the so-called blockchain technology. These technologies allow a consensus to be achieved across members of the network regarding the validity of the ledger. This distributed ledger concept underpins decentralized VCs—for example the blockchain technology behind Bitcoin. The distributed ledger provides a complete history of transactions associated with the use of particular units of a decentralized VC. They provide a secure permanent record that cannot be manipulated by a single entity and do not require a central registry.

A key conclusion of the paper is that the distributed ledger concept has the potential to change finance by reducing costs and allowing for deeper financial inclusion in the longer run. This could be especially important for remittances, where transaction costs can be high, around 8 percent. Distributed ledgers can also shorten the time required to settle securities transactions, which currently take up to three days, as well as lower counterparty and settlement risks.

“Virtual currencies and their underlying technologies can provide faster and cheaper financial services, and can become a powerful tool for deepening financial inclusion in the developing world,” said IMF Managing Director Christine Lagarde, who presented the report at the World Economic Forum, in Davos, during the panel Transformation of Finance. “The challenge will be how to reap all these benefits and at the same time prevent illegal uses, such as money laundering, terror financing, fraud, and even circumvention of capital controls.”

Note: Staff Discussion Notes (SDNs) showcase policy-related analysis and research being developed by IMF staff members and are published to elicit comments and to encourage debate. The views expressed in Staff Discussion Notes are those of the author(s) and do not necessarily represent the views of the IMF, its Executive Board, or IMF management.

One thought on “Will Virtual Currencies Go Main Stream?”