In a Speech “The Evolving Risk Environment”, Malcolm Edey RBA Assistant Governor (Financial System) discussed some of the risks to financial stability, both globally and locally.

Much of the story has been told before, the economic uncertainties surrounding oil, China, Europe, high debt levels and locally the risks (and how they have been controlled) in the housing market, and potential risks in the commercial property sector.

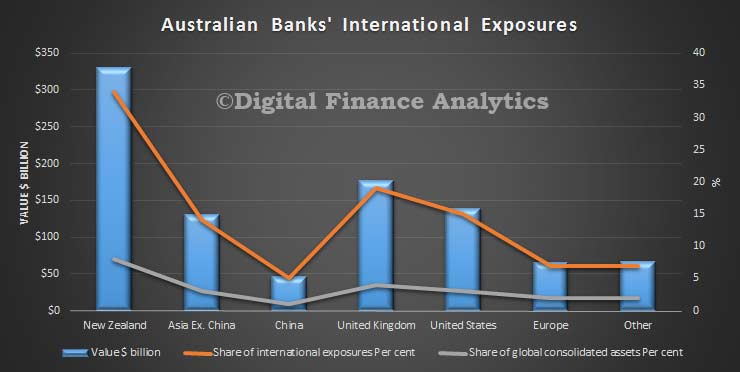

One specific issue he covered was the potential international exposures Australian banks may face. He focussed specifically on the assets Australian banks hold overseas.

Direct exposures of Australian banking institutions to the risk factors I have been describing are quite limited Exposures to the euro area have been scaled back in the wake of the crisis and now represent only around 1 to 2 per cent of Australian banks’ consolidated global assets. Although exposures to the Asian region have been growing quite rapidly over recent years, they are still a relatively small share of consolidated assets – around 4 per cent. Many of these exposures are shorter-term and trade-related, factors that should lessen credit and funding risks. That said, operational and legal risks around these exposures could be relatively high, particularly given the rapid expansion of these activities in recent times.

Fair point. However, there are two other exposures to also consider. First banks here are funding their lending partly via capital markets overseas, because there is a gap between the value of deposits held and loans made. Different banks have different footprints. But this means if the international capital markets froze for any reason this would be a significant risk locally. This was demonstrated during the GFC. In any case, in the current environment, spreads are rising, and funding is becoming more expensive. To an extent, given limited competition here, they can just raise rates to customers. But there will be some limits. Recently we have seen a number of lifts in some mortgage rates and to the SME sector.

The other exposure is from international investors and fund managers who invest in the shares of the banks here, and who are also thinking about risk profiles, local economic performance and other factors. We often get asked to provide a picture of things here by such investors. They will consider levels of returns and risks implicit in these returns. Given that going forwards, it is likely banks will find it harder to maintain current dividends than in the past, we may see a change in the wind here too. If international investors were to jump ship, expect market prices to fall.

So, my simple point is that banks are exposed to global forces, well beyond those risks of default on loans, and these additional should be factored into discussions of financial stability.

I would also highlight that not all banks are equally exposed, as underscored by the batch of results declared in the past couple of weeks.