We have been highlighting the battle for market share, and the varying discounts which are available to some. Today we deep dive into the world of discounts, drawing data from our market model. We conclude that households, on average, get better discounts which using a broker, discounts for investment loans are more generous, and reconfirm that more affluent households get the best deals. We also see that competition and deep discounts are making many loans unprofitable to the banks who make them (taking fully absorbed costs into account). As such, the current deep discounts are unsustainable.

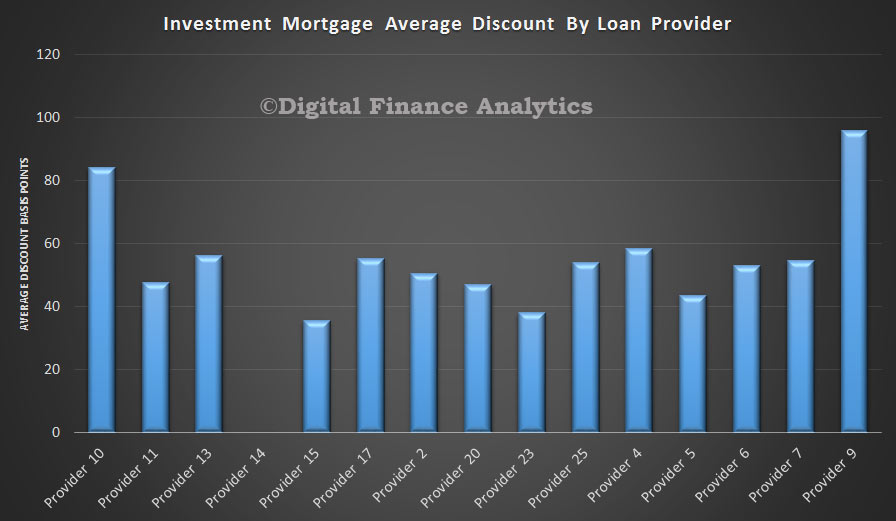

We start by looking at the average discounts in basis points individual loan providers are offering. Some are significantly more aggressive than others. We have hidden the real names of the lenders concerned. We see that there are more banks offering owner occupied loans than investment loans. The best average discount for an investment loan is from provider 9.

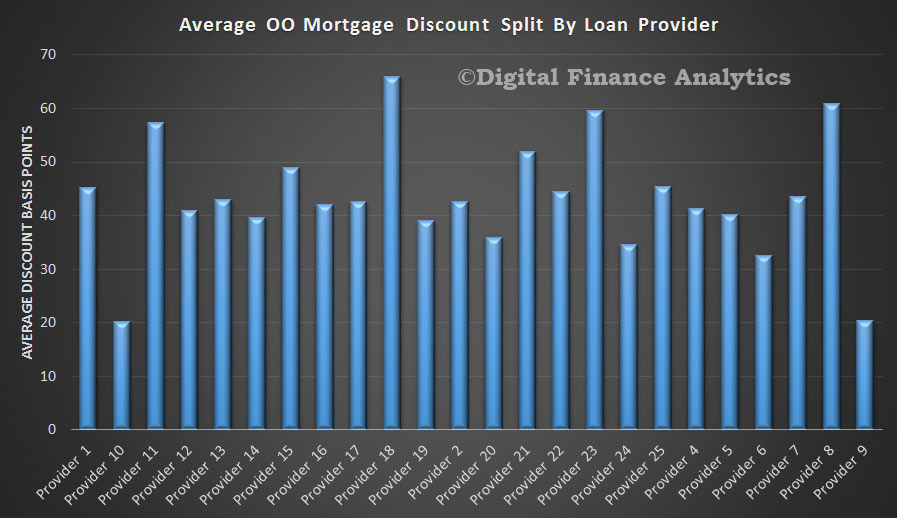

Some of the owner occupied providers are quite generous in their discounts, but generally investment loans get bigger discounts at the moment.

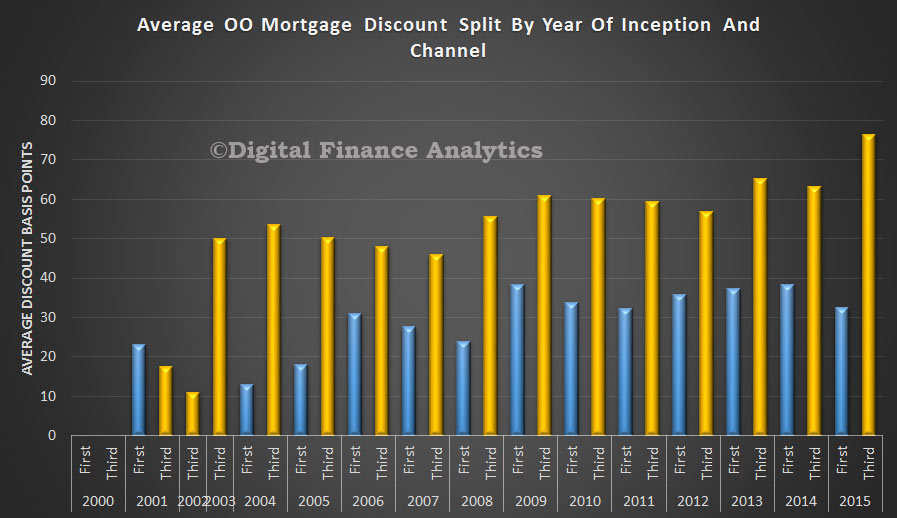

Looking at channel of origination, and year of inception of the loans, we see that consistently third party (broker) loans get bigger discounts, and that the discounts have been growing in recent years. In the owner occupied sector, discounts for loans via the branch (first party) are slightly lower in 2015.

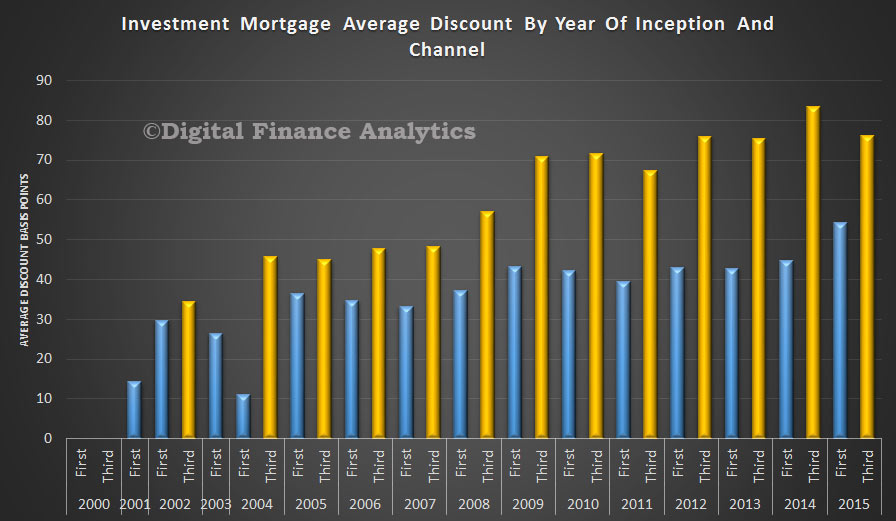

In the investment loan sector, we see a trend of growing discounts in recent years, with third party originated loans getting a better deal.

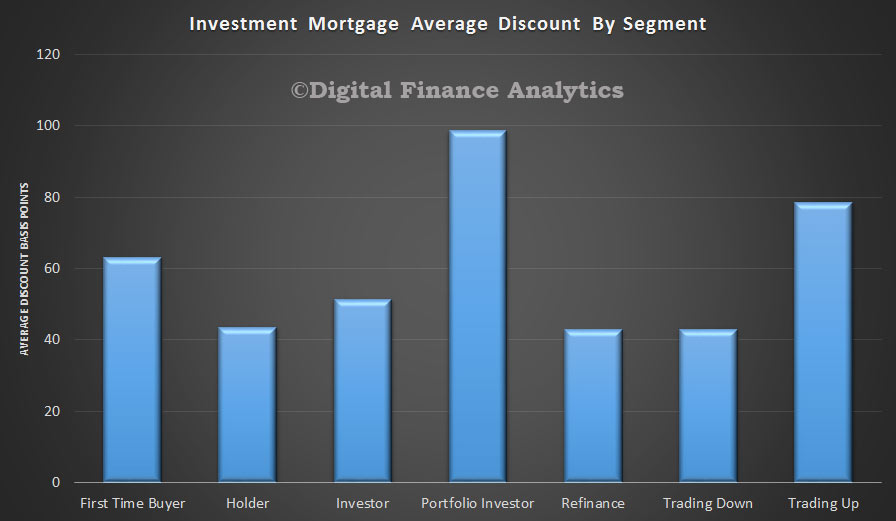

Turning to the DFA property segments, in the investment loan category, we see that portfolio investors are getting the very best discounts, whilst first time buyers are not doing so well, but they are slightly ahead of holders, refinance and trading down households.

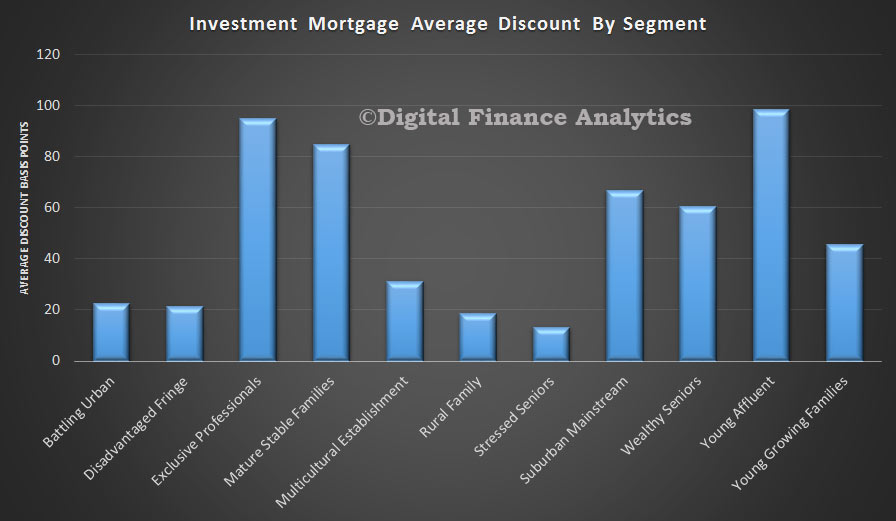

Looking at our master household segments, we see that the wealthy – professionals and young affluent get the best deals. Those with less bargaining power do not do so well.

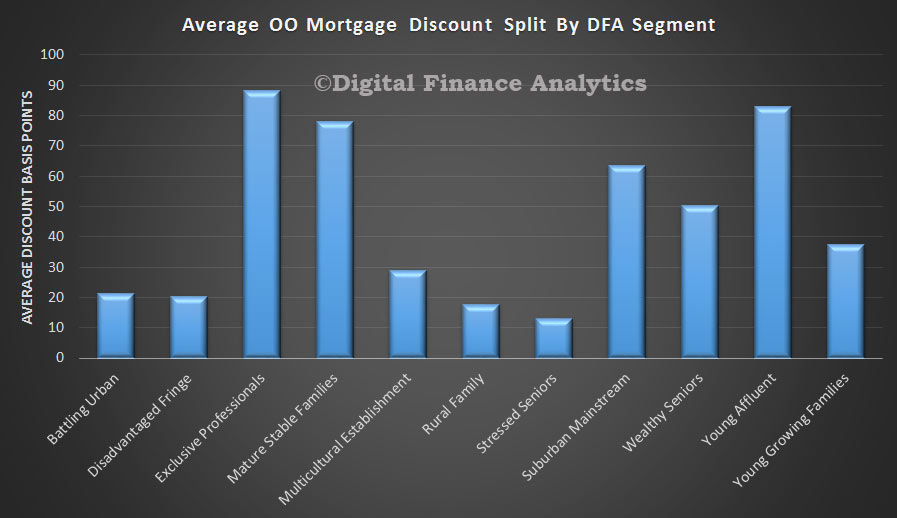

This is true of both investment mortgages (above) and owner occupied mortgages below, though we see that in the latter case, the discounts are slightly less generous.

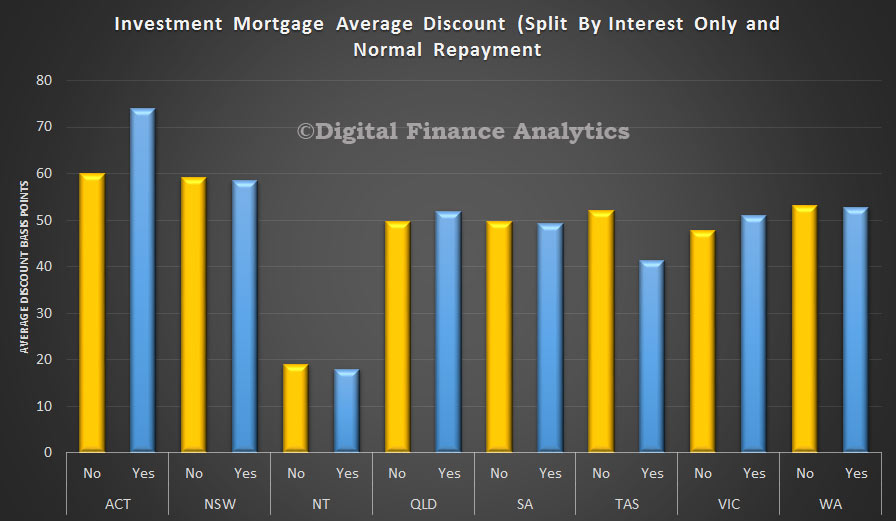

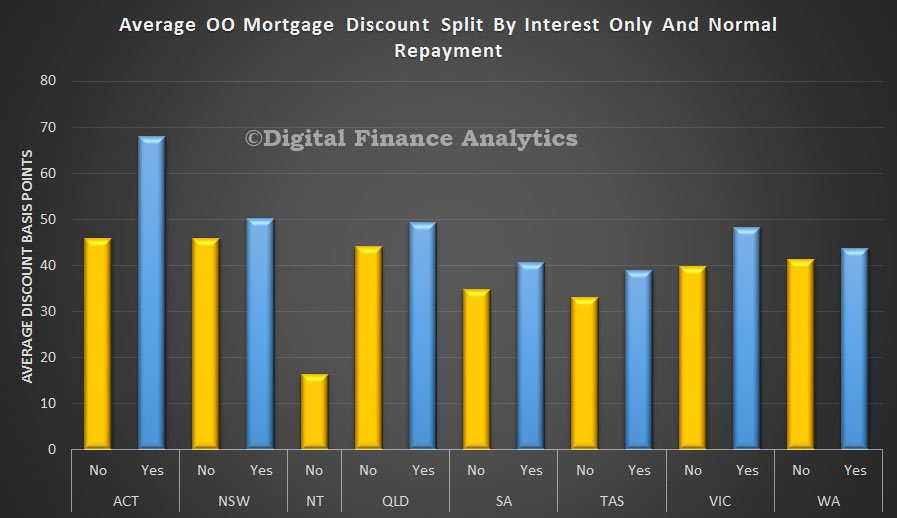

We also see that interest only loans command a larger discount in some states, especially in ACT. Others are more line ball.

In comparison interest only owner occupied loans can consistently command a larger discount, than normal repayment loans, but as highlighted already these discounts are on average a little lower than in the investment sector.

So what is the profit impact of these discounts? DFA has calculated the relative profit of each loan and using an index we can display the relative profit contribution in cash terms. For owner occupied loans, up until 2013, most years were net profitable to the lenders. We note that this changed in 2014 and 2015 as discounts expanded, and competition increased. Overall in cash terms they are making a slight net loss on some loans written now. This is partly explained by the one off costs of setting up a new loan, and initial broker commissions. As loans age, they on average become more profitable.

So what is the profit impact of these discounts? DFA has calculated the relative profit of each loan and using an index we can display the relative profit contribution in cash terms. For owner occupied loans, up until 2013, most years were net profitable to the lenders. We note that this changed in 2014 and 2015 as discounts expanded, and competition increased. Overall in cash terms they are making a slight net loss on some loans written now. This is partly explained by the one off costs of setting up a new loan, and initial broker commissions. As loans age, they on average become more profitable.

The investment loan profit footprint is very interesting, as here we see a consistent fall in the profit index since 2010, with the largest drops in 2014 and 2015. This is explained partly by the significant growth in volumes, and the deeper discounting. Again, older loans become more valuable. Most banks would calculate an amortised cost of origination, spread over a number of years, but we prefer a true cash view.

We conclude from this that recent loans for many providers (especially those less efficient) will be loosing money initially, and the portfolio will be supported by the older more profitable loans. We also think that discounts are unsustainable at current levels, and will see them come off over the next few months.