Interesting piece from the St. Louis Federal Reserve looking at the connection between age and wealth and its implications for aging and wealth inequality.

An individual’s wealth varies with age. Most people are born with little to no financial wealth and, as they age, they save part of their income to accumulate wealth or sometimes borrow to finance education, which creates debt. Once people reach retirement, they stop accumulating wealth and start spending down their savings. Thus, the richest people can often be found among those who are about to retire.

Age is not the only determinant of wealth. People’s wealth varies with how much they are given by their parents, their income, and their decisions on how much to consume or save and how to invest their wealth.

In this essay, however, we focus on the connection between age and wealth and its implications for aging and wealth inequality. The issue is salient because the U.S. population is aging and inequality is a frequent concern. Today, less than 15 percent of the overall population is 65 years of age or older, and that share is projected to rise above 30 percent by 2030. Is this going to exacerbate or mitigate wealth inequality in the United States?

The figure shows wealth per capita (black line) by age group in 2010. As indicated earlier, the richest people tend to be 65 to 74 years of age. The figure also shows the fraction of wealth (dashed line) held by households, ranked by the age of the head of household. A key message is that age is a significant source of inequality: The largest and youngest groups hold the least wealth—those under 35 years of age (blue line) represent over 25 percent of the population but hold only about 5 percent of total wealth. If the dashed and blue lines overlapped, each group’s share of the population and share of wealth would be the same and age would not contribute to wealth inequality. In this case, the black line would be flat: Each individual would hold the same amount of wealth, regardless of age.

One can examine the effect of the age distribution using a standard measure of wealth inequality: the Gini index (sometimes called the Gini coefficient), which varies from 0 to 1. A value of 0 indicates no inequality—everyone holds the same wealth. A positive Gini index indicates some inequality. If one individual held all the wealth—maximal inequality—the Gini index would equal 1. In the United States, for example, the richest 1 percent of the population holds 42 percent of total wealth.1 As the figure shows, the age group with the highest share of wealth—those 55 to 64 years of age—holds almost 31 percent of the wealth but represents only about 16 percent of the population. The Gini coefficient implied by the figure is 0.385.2 Because this Gini coefficient measures only the dispersion of wealth by age group, it omits additional sources of wealth inequality and therefore understates the true Gini coefficient for the United States.

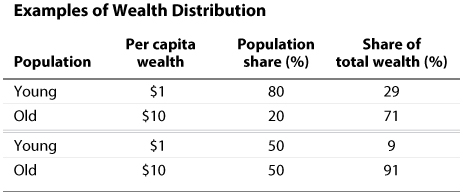

A simple example helps illustrate that wealth inequality by age contributes to overall wealth inequality: Consider an economy, as shown in the table, with 100 people. Each young person holds $1 of wealth, while each old person holds $10 of wealth (top panel). The population shares of young and old are 80 percent and 20 percent, respectively. Note that this panel represents, in a stylized way, the features of the U.S. economy displayed in the figure: There are many more young people than old people, but the old hold more wealth than the young. The total wealth of this economy is $280, where the young collectively hold $80 and the old collectively hold $200. The young’s share of total wealth is (80/280) = 29 percent, which is noticeably less than their 80 percent share of the population. The Gini coefficient associated with this distribution of wealth is 0.51.

Suppose now that the economy ages and there are 50 old people and 50 young people (bottom panel). Because older people have more money, total wealth in the economy rises from $280 to $550. If each young person still holds $1 of wealth, their share of total wealth becomes (50/550) = 9 percent instead of 29 percent—a decline of 20 percentage points. But their share in the population decreased by 30 percentage points, from 80 percent to 50 percent, so the Gini coefficient declines from 0.51 to 0.41.

So the aging of the population, per se, is a factor that can reduce wealth inequality. This example, however, must be interpreted with caution. It does not imply that the forecasted aging of the U.S. population will be accompanied by a reduction in wealth inequality. As mentioned in the introduction, the calculation presented here abstracts from other forms of inequality not related to age. It is conceivable that these other forms of inequality may increase as the population becomes older and offset the effects described here.