Moody’s says not only did the wide majority of experts incorrectly predict the outcome of the US Presidential election, pundits also were far off the mark regarding how markets might react to an improbable Donald J. Trump victory. Instead of conforming to pre-election expectations of an equity market sell-off and lower interest rates, both share prices and bond yields have soared since Trump’s victory. Whether they remain higher depends on a widely anticipated acceleration by business sales vis-a-vis employment costs that may not materialize.

As inferred from recent market performance, the economic, taxation, and regulatory policies of the past eight years curbed business activity considerably and, by doing so, reined in the growth of attractive job opportunities. To the degree existing policies limited US business activity, they very much facilitated Donald Trump’s Presidential upset. Perhaps, “secular stagnation” is partly the offshoot of suboptimal government policies that helped to slash US real GDP’s average annual growth rate from the 3.3% of the 10-years-ended 2006 to the 1.3% of the 10-years-ended 2016.

Nevertheless, unprecedented demographic change that is beyond the scope of an immediate government remedy is one of the major drivers of “secular stagnation”. The aging of the US population complements the deceleration of growth quite nicely.

When the US economy grew by 3.3% annually during the 10-years-ended 2006, the number of Americans aged 65 years and older rose by 310,000 annually, on average, while the number aged 16 to 64 years — a proxy for the working-age population — expanded by a much greater 2.36-million annually. By the 10-years-ended 2016, the average annual increase in the number aged at least 65 years soared to 1.28 million as the annual addition to the working-age population sagged to the same 1.28 million.

Notwithstanding the likely implementation of more stimulatory policies, US growth during the next 10-years-ended 2026 will still be constrained by projected average annual increase of only 470,000 for the number of 16- to 64-year old Americans, which is far less than the forecasted average annual addition of 2.05 million to the ranks of those 65-years and older.

If, as expected, the US working-age population grows by 0.5% annually during the next 10-years, then a likely range of 1.0% to 1.5% for the average annual rate of labor productivity growth suggests that US real GDP will increase by between 1.5% and 2% annually through 2026, which is much slower than its 3.2% average annualized increase of the 25 years ended 2006.

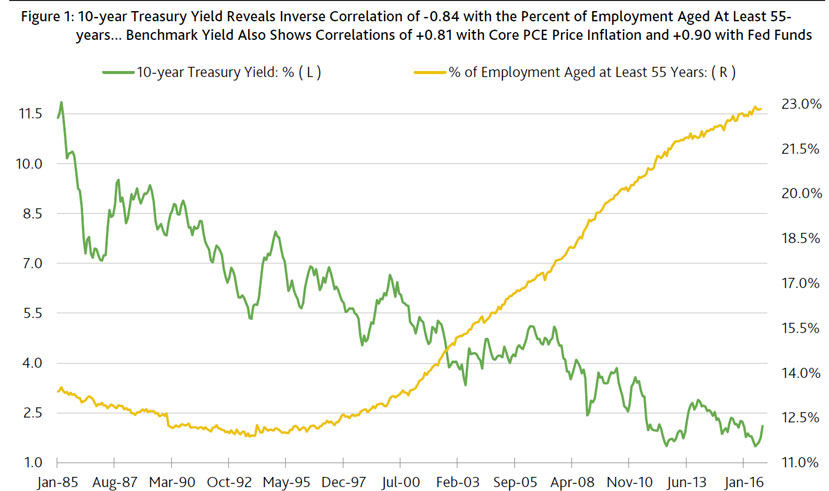

Older workforce may keep 10-year Treasury yield under 3% to 5% range. In addition to the overall population, the US workforce is also getting older in a manner never seen before. Since June 2009’s end to the Great Recession, the cumulative 8.5% growth of household-survey employment was unevenly split between a 3.9% increase in the number of employees aged less than 55 years and a 28.0% surge for the employment of Americans aged at least 55 years.

If employment growth remains skewed toward older workers, part-time workers will probably constitute an above-trend share of employment, while the growth of both personal income and household spending will be slower than otherwise. The underlying growth of both income and spending slowed as the share of workers aged at least 55 years soared from October 1996’s 12.1% to October 2016’s 22.8% of total US employment.

Some now warn of an impending climb by the 10-year Treasury yield to a range of 3% to 5%. However, an older workforce weighs against a much higher benchmark Treasury yield. An older workforce and an aging population are expected to limit the upsides for inflation risk, private-sector borrowing, and household expenditures growth by enough to prevent the 10-year Treasury yield from becoming stuck in a range of 3% to 5%.

Credit Markets Review and Outlook

As illustrated by Figure 1, the 10-year Treasury yield maintains a strong correlation of -0.84 with the share of employment aged at least 55 years. Getting to a forecast midpoint of 3% for the 10-year Treasury requires that the employment of Americans aged at least 55 years drop from October 2016’s 22.8% to roughly 20% of total employment. Such a rejuvenation of US employment is highly unlikely. The impossibility of making America young again renders it all the more difficult to make America great again. (Figure 1.)

Equity rally helps to drive benchmark yields sharply higherThus far, earnings-sensitive markets view the Republican sweep of the House, Senate, and Presidency positively. Since November 8’s election, the market value of US common stock was recently up 1.9%. Moreover, after the VIX index’s average soared from October 2016’s 14.6 points to the 20.0 points of November’s first eight days, this equity market “fear factor” subsequently dropped to a recent 14.6. The latter has been statistically associated with a 430 bp midpoint for the high-yield bond spread, which was thinner than November 9’s band of 508 bp.

The post-election equity rally stems from improved prospects for business activity and profits. The Republican sweep boosts the odds favoring a fiscal stimulus package that includes lower tax rates on personal and corporate income, as well as stepped-up infrastructure spending. Moreover, a much reduced rate of taxation on the repatriation of corporate cash held overseas is probable.

In addition, business operating costs are likely to be effectively reduced by the repeal of the Affordable Care Act and a broad-based easing of federal regulations. On the regulatory front, Bloomberg reports that Trump’s Financial Services Policy Implementation team will devise a strategy that aims to dismantle 2010’s Dodd-Frank Act. Expectations of both Dodd-Frank’s demise and Fed rate hikes have driven the KBW index of bank stock prices up by more than 9% since November 8.

Nevertheless, upwardly revised outlooks for business activity and corporate earnings quickly drove the 10-year Treasury yield up by 27 bp from November 8’s close to a recent 2.13%. Not since January 2016 has the 10-year Treasury yield been this high.

Recent auctions of new 10- and 30-year Treasury bonds were weak. The 2.22:1 bid-to-cover ratio for November 9’s $23 billion auction of 10-year Treasury notes was the lowest since March 2009. In addition, foreign participation was weak at both sales. Trump’s surprising victory may have temporarily scared off foreign buyers of US Treasuries.

Nevertheless, the dollar exchange rate has climbed higher since the election. The recent widening of the yield spreads between US Treasuries and the sovereign government bonds of other advanced economies may help to further firm the dollar exchange rate, where expectations of an even stronger dollar may contain Treasury yields by (i) reducing inflation expectations, (ii) boosting foreign purchases of US Treasuries, and (iii) lowering the outlook for US corporate earnings.

Credit Markets Review and Outlook

Despite a costlier dollar exchange rate, industrial metals prices have soared. On November 9, Moody’s industrial metals price index was up by 29.4% from a year earlier.

However, the still relatively modest pace of global industrial activity questions the sustainability of the latest surge by base metals prices. Perhaps, speculative buying in anticipation of a lively rejuvenation of global industrial activity now drives base metals prices higher. If the world’s consumers fail to cooperate and spending does not rise by enough to support costlier base metals, base metals price deflation will return.

Given the persistent price deflation afflicting tangible consumer goods, manufacturers will have difficulty passing on higher materials costs to final product prices. In October, the annual rates of price deflation were -2.3% for the consumer durable goods’ component of the PCE price index and -0.6% for the core consumer goods price index. The underutilization of the world’s production capabilities should continue to contain prices of internationally tradable products regardless of forthcoming stimulus and deregulation.A fundamentally excessive climb by Treasury bond yields could sink share prices and widen spreads. Thus, credit-sensitive activity may offer insight as to how high interest rates might climb. In view of how unit home sales recently slowed amid a less than 3.5% mortgage yield, an impending climb by the mortgage yield to a range of 3.75% to 4% risks an outright year-over-year contraction by home sales.