Household debt in Australia continues to rise. But the strongest growth at 15%, is found in the sub prime Alternative Lending Personal Credit sector.

So it is worth considering the personal credit market holistically.

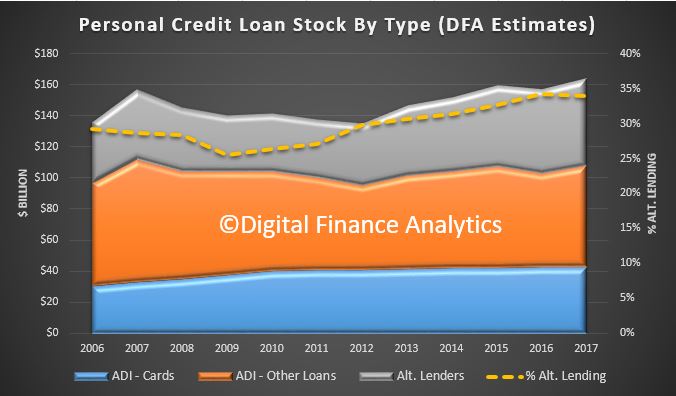

Drawing data from our cure market models we estimate total personal credit to the ~9.2 million Australian households currently amounts to $164 billion. This is separate from the $1.7 trillion secured debt for owner occupied and investment housing.

Within that banks and mutuals (ADI’s) hold $42 billion in credit cards, and $66 billion in personal loans of all types. But this leaves Alternative Lenders, (non-banks) with around $56 billion, or 34% of all personal credit. The chart below shows the relative shares since 2006. The Alternative Lending sector is growing faster than credit from ADI’s.

Relatively, overall personal credit has grown at around 2.6% in the past 3 years. Within that, credit card debt has been static, ADI personal credit rose 2% but Alternative Lending credit rose 5%.

Relatively, overall personal credit has grown at around 2.6% in the past 3 years. Within that, credit card debt has been static, ADI personal credit rose 2% but Alternative Lending credit rose 5%.

In fact ADI’s have stepped up their personal lending as mortgage lending has eased, with an 8% rise in the past 12 months. We expect this momentum to continue, with a strong focus on vehicle credit, another risk area!

Alternative Lenders include many large well established companies, as well as a rising tide of new online lenders, including P2P loan providers. In fact online has become the predominate origination channel. As they are not banks, ASIC is the primary regulatory body.

But looking in more detail, the sub prime segment of Alternative Lending has growing significantly faster at around 15% per annum over the past three years, compared with 5% for all Alternative Lending. We define sub prime as households with VedaScore/Equifax Score below 622, or a poor credit history, or adverse personal circumstances.

There are a range of products taken by households in the sub prime segment, including unsecured personal loans, Medium Amount Credit Contracts (MACC), Small Amount Credit Contracts (SACC), secured and unsecured car loans or loans on other capital goods, and loans secured by assets, such as cars post purchase.

Our surveys show that a considerable number of highly in debt households with mortgages also hold loans with Alternative Lenders. Such loans might be difficult spot during an assessment of a mortgage loan application, thanks to the negative credit records which are only now morphing into comprehensive credit.

This is a concerning trend and is further evidence of the debt laden state of many households. It also helps to explain the gap between stated finances on a mortgage loan application and the real state of household finances.

Note SME’s are excluded from this analysis.