The Bank of England just published a staff working paper “Specialisation in mortgage risk under Basel II“. Lenders using the less sophisticated risk models (generally smaller banks) are found to have a higher concentration of higher-risk mortgages than those using the advanced models.

They looked at the two models which were introduced under Basel II, lenders’ internal models (IRB) and the less risk-sensitive standardised approach (SA) by using a dataset covering 7 million UK mortgages from 2005-15. The switch to Basel II gave lenders using IRB models a comparative advantage in capital requirements (compared to lenders using the SA approach), particularly at low loan-to-value (LTV) ratios, and this was reflected in prices and quantities. They concluded:

They looked at the two models which were introduced under Basel II, lenders’ internal models (IRB) and the less risk-sensitive standardised approach (SA) by using a dataset covering 7 million UK mortgages from 2005-15. The switch to Basel II gave lenders using IRB models a comparative advantage in capital requirements (compared to lenders using the SA approach), particularly at low loan-to-value (LTV) ratios, and this was reflected in prices and quantities. They concluded:

First, mortgage risk is concentrated in lenders using the SA approach, which is typically used by smaller lenders, suggesting a potential higher failure rate than among IRB banks.

Second, macroprudential tools may affect the strength of the specialisation mechanism. This should be accounted for in calibrating such tools.

Third, they validate the view from competition authorities who have identified the cost of adopting IRB as a potential barrier to entry and expansion. IRB provides a competitive advantage in low LTV ratio mortgages.

Finally, the effect, is not specific to the mortgage market and this needs further research.

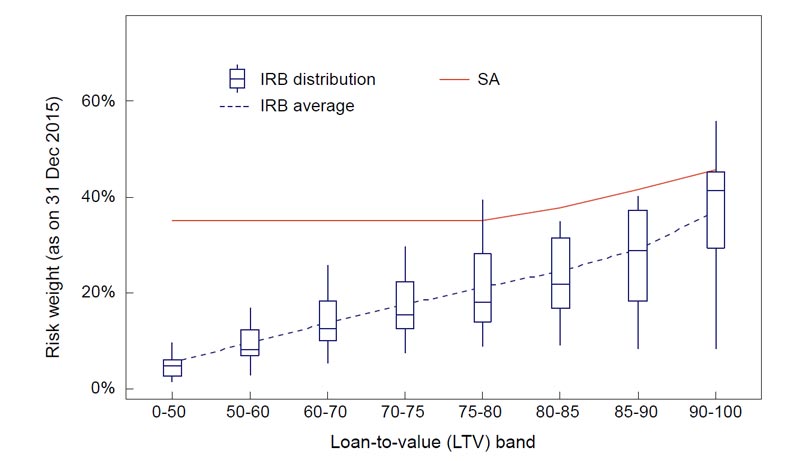

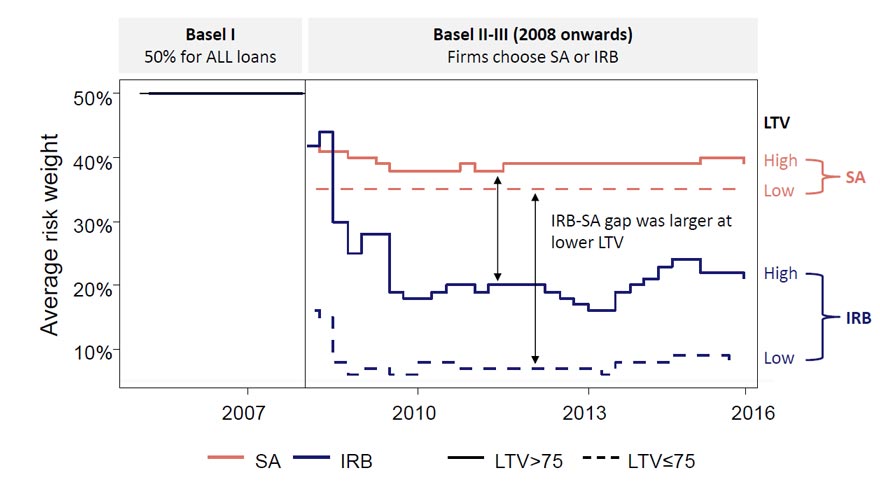

IRB risk weights increase with the LTV ratio, the main indicator for credit risk used by UK mortgage lenders. In contrast, SA risk weights are fixed at 35% for LTV ratios up to 80%, and are then 75% on incremental balances above the 80%

LTV threshold. IRB risk weights tend to be lower than SA risk weights across most LTV ratios, but the gap is larger for lower LTV ratios. In 2015, the gap between the average IRB risk weight and the SA risk weight was about 30 percentage points for LTV ratios below 50%, compared to less than 15 percentage points for LTV ratios above 80%. The scale of variation in risk weights between IRB lenders is smaller than the gap between the IRB average and SA risk weights, at least at lower LTV ratios.

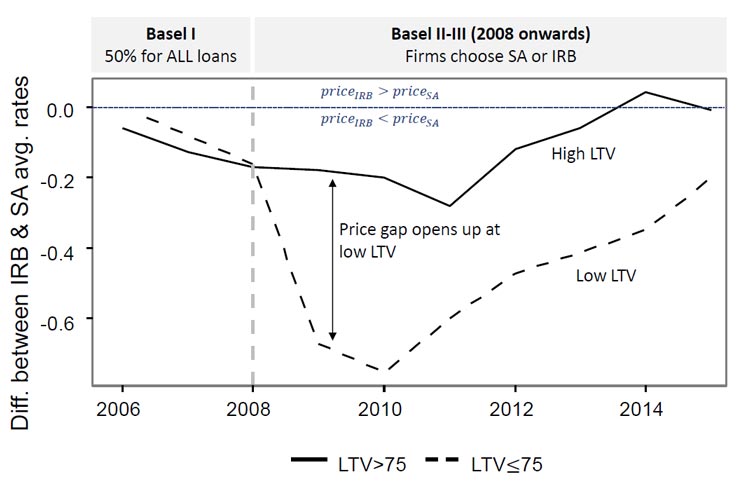

IRB lenders gain a comparative advantage in capital requirements compared to SA lenders, particularly at low loan-to-value (LTV) ratios. This comparative advantage is reflected in prices and quantities.

We expect all lenders to price lower for lower LTV mortgages. But under Basel II versus I, IRB lenders did so by 31 basis points (bp) more, and increased the relative share of low-LTV lending in their portfolios by 11 percentage points (pp) more, than SA lenders. Such specialisation leads to systemic concentration of high risk (high LTV) mortgages in lenders who tend to have less sophisticated risk management.

With an average 30 percentage point gap between IRB and SA risk weights for LTV ratios below 50%, this corresponds to an economically significant price advantage of 30bp. From the perspective of a typical borrower at this LTV level, with a 50% LTV mortgage against a $200,000 property, repayable over a remaining 15 year term, 30bp translates to around $170 per year or 0.7% of median household disposable income. From the lender’s perspective, a 30bp disadvantage translates to several places in `best buy’ tables, and thus likely material loss of market share.

If instead of risk weights we consider directly the variation in capital requirements, which is driven by both risk weights and lender-specific capital ratio requirements, a 1pp reduction in capital requirements causes a 6bp decrease in interest rates. These latter results can also be interpreted as `pass-through’ rates from lender-specific changes in risk weights or capital requirements to prices, subject to limits on external validity due to the Lucas critique.

Finally, we find that the pass-through from capital requirements to prices is significant only when lenders have low capital buffers (the surplus of capital resources over all regulatory requirements). Lenders with a buffer below 6pp of risk-weighted assets increase prices by 1.7bp basis point for a 1pp increase in risk weights.

Note: Staff Working Papers describe research in progress by the author(s) and are published to elicit comments and to further debate. Any views expressed are solely those of the author(s) and so cannot be taken to represent those of the Bank of England or to state Bank of England policy. This paper should therefore not be reported as representing the views of the Bank of England or members of the Monetary Policy Committee, Financial Policy Committee or Prudential Regulation Authority Board.