Yesterday we took a deep dive looking at how sensitive borrowing households are to a prospective rise in their owner occupied mortgage rates. A fundamental, though valid assumption we made was to look at the relative number of households impacted. This distribution led the analysis.

However, we can look at the data through a lens of relative mortgage value, not household count. This changes the perspective somewhat and today we explore this additional dimension.

We use the same movement in rate scenarios, from under 0.5% up, to more than 7% and show the relative portfolio distribution by value of outstanding loans and the tipping point where the household would fall into mortgage stress.

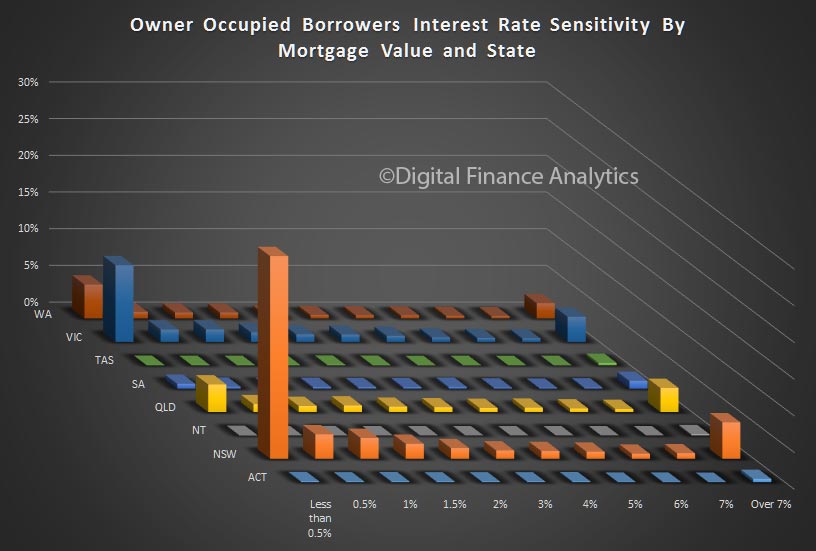

Using this lens, we immediately see that from a value perspective, a significant proportion of value resides in NSW (larger home prices, bigger loans). Within the NSW portfolio, more than 20% of the value would be impacted by a small incremental rise in mortgage rates. We also see some value impacted in VIC and WA, but to a lessor degree. In other words, the more highly leveraged state of households in NSW means a small rise in real mortgage rates will bite hard here. This despite all the focus in the press on WA and QLD!

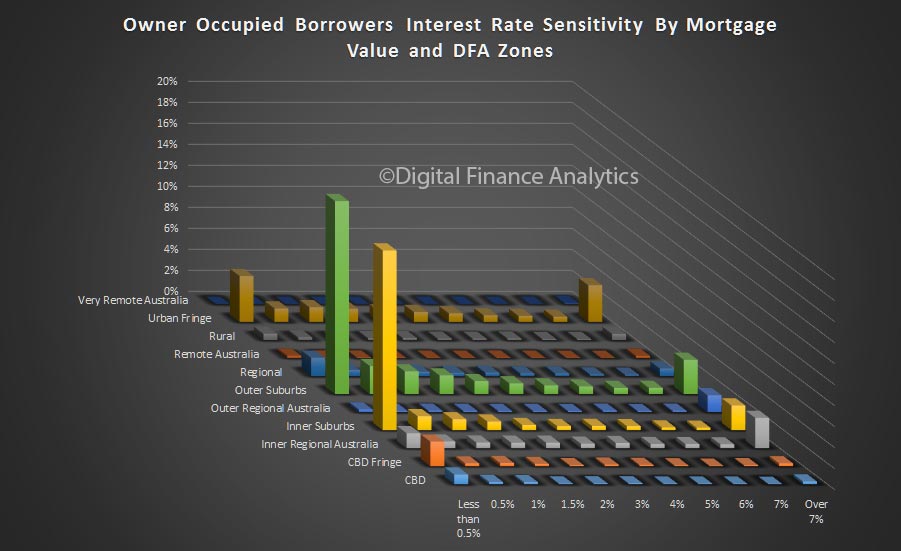

Another interesting view is created by using our geographic zoning definitions, radiating from the central business district (CBD) in the middle, in concentric rings, out to the suburbs, and into the regions beyond. The areas where sensitivity is highest to small rate rises are the inner and outer suburbs, plus the urban fringe. This is because mortgages are quite large, relative to incomes. In other words, there is a geographic concentration risk which needs to be taken into account.

Another interesting view is created by using our geographic zoning definitions, radiating from the central business district (CBD) in the middle, in concentric rings, out to the suburbs, and into the regions beyond. The areas where sensitivity is highest to small rate rises are the inner and outer suburbs, plus the urban fringe. This is because mortgages are quite large, relative to incomes. In other words, there is a geographic concentration risk which needs to be taken into account.

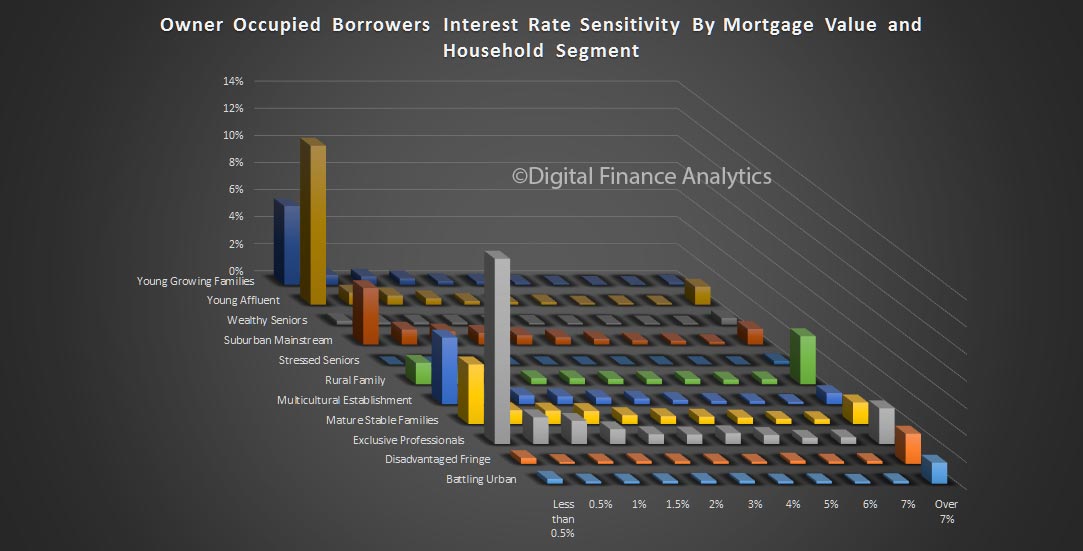

Our household segmentation models highlights that from a value perspective, young affluent and exclusive professionals have a dis-proportionally large share of value, and a significant proportion of this would be at risk from even a small rise.

Our household segmentation models highlights that from a value perspective, young affluent and exclusive professionals have a dis-proportionally large share of value, and a significant proportion of this would be at risk from even a small rise.

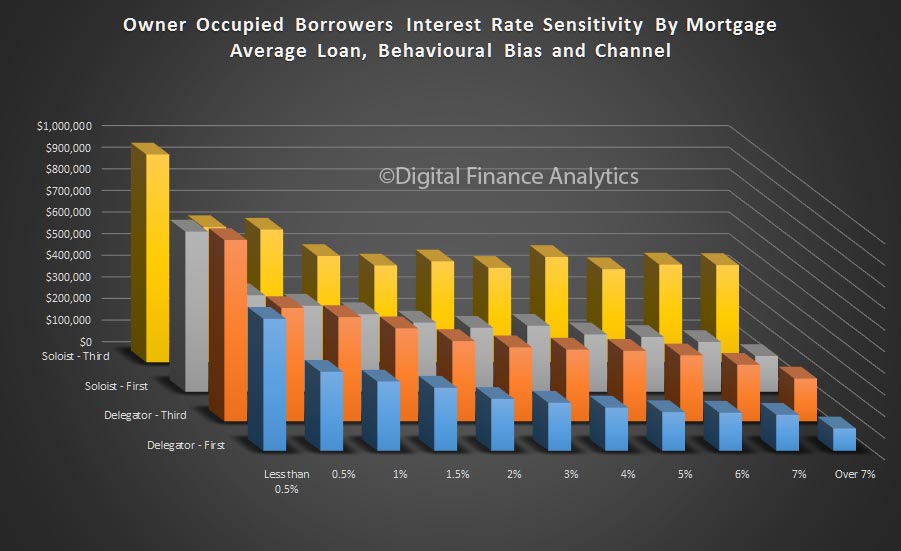

Finally, again using our value lens, we can see that the largest segment which would be impacted by a 0.5% or less rate rise are soloists (see our earlier post for definitions) who got their mortgage via mortgage brokers. In comparison, delegators who get their loans direct from the bank, without an intermediary, are least exposed.

Finally, again using our value lens, we can see that the largest segment which would be impacted by a 0.5% or less rate rise are soloists (see our earlier post for definitions) who got their mortgage via mortgage brokers. In comparison, delegators who get their loans direct from the bank, without an intermediary, are least exposed.

So, we conclude it is essential to look at the mortgage portfolio both from a value AND count perspective. But in fact, it is the value related lens which provides the best view of relative risk. This is how risk capital should be allocated.

So, we conclude it is essential to look at the mortgage portfolio both from a value AND count perspective. But in fact, it is the value related lens which provides the best view of relative risk. This is how risk capital should be allocated.

Larger loans, via brokers are inherently more risky in a rising rate environment.

One thought on “Another Perspective On Rate Sensitivity”