ANZ released their trading update for 3 months to 31 December 2016. Whilst the information is selective, and unaudited, we see growth in home lending supporting retail banking, along with deposit growth, but group net interest margin “declined several basis points” (not specified) and capital ratios down a little. Cost management was a highlight. Disposal of “non-core” assets will help the result. The credit environment is marginally better than expected, they say.

The unaudited results show a statutory net profit of $1.6 billion up 8% compared to the quarterly average of the second half of FY16. Cash Profit was $2.0 billion up 31% (Adjusted Proforma up 20%) benefited from a good performance in Australia and New Zealand Retail and in Institutional along with a lower provision charge and the sale of 100 Queen Street.

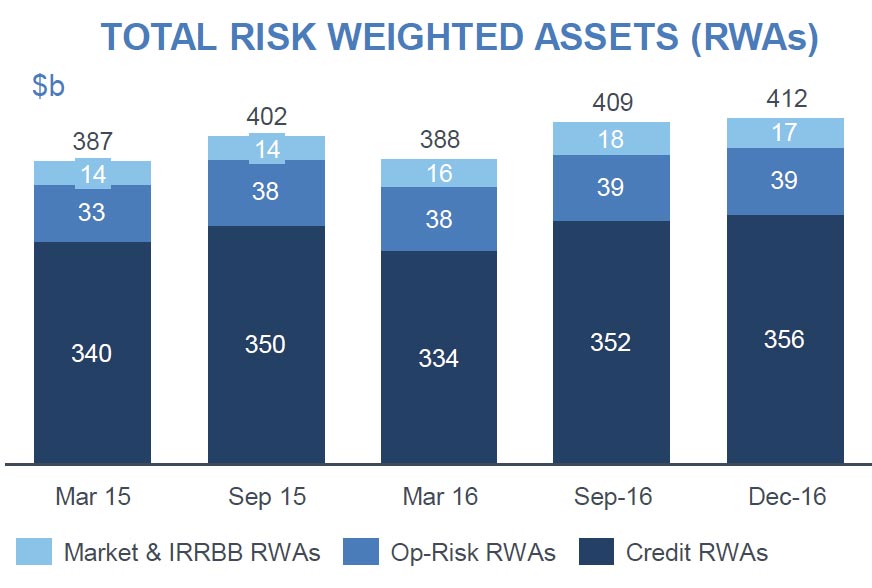

Profit before Provisions was up 17% (Adjusted Proforma up 9%). Revenue was up 7% (Adjusted Proforma up 4%), expenses down 4% (Adjusted Proforma down 1%) driven by current and prior period productivity initiatives and tight cost management. Total risk weighted assets (RWAs) rose from $409 bn in Sept 16 to $412 bn in Dec 16.

However Group Net Interest Margin (NIM) declined several basis points (bps) reflecting lower earnings on capital and higher funding costs driven by improving liability mix from strong deposit growth.

However Group Net Interest Margin (NIM) declined several basis points (bps) reflecting lower earnings on capital and higher funding costs driven by improving liability mix from strong deposit growth.

In Australia, home lending volumes grew, whilst commercial lending volumes were more subdued. Deposit growth was strong.

Institutional banking benefited from favourable trading conditions on the back of movements in the USD and yield curve.

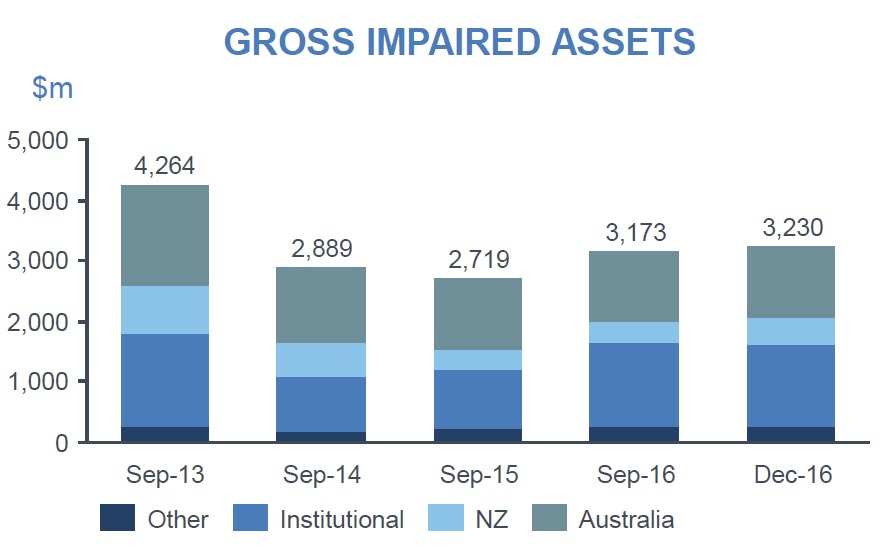

Gross Impaired Assets increased 1.8%.

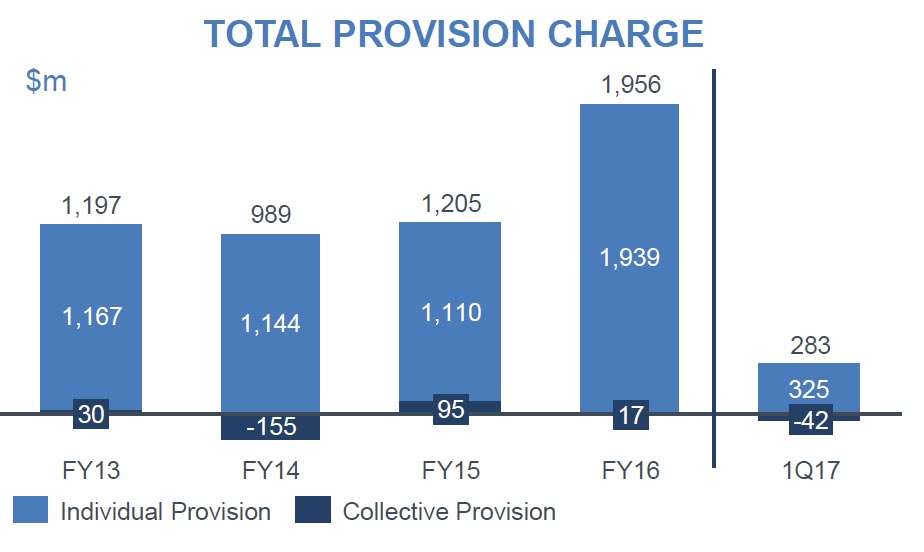

The Total Provision charge was $283 million with the Individual Provision (IP) charge $325 million. A Collective Provision release of $42 million was assisted by portfolio composition improvement and exposures transferring to IP. There were no changes to management overlays.

The Total Provision charge was $283 million with the Individual Provision (IP) charge $325 million. A Collective Provision release of $42 million was assisted by portfolio composition improvement and exposures transferring to IP. There were no changes to management overlays.

APRA Common Equity Tier 1 (CET1) ratio was 9.5% at 31 December, compared with 9.7% in June 16. Excluding the payment of the 2016 Final Dividend (net of the Dividend Reinvestment Plan), CET1 increased 40 bps in the first quarter, primarily driven by organic capital generation of 48 bps which is substantially stronger than the Post Basel III 1Q average of 21 bps.

APRA Common Equity Tier 1 (CET1) ratio was 9.5% at 31 December, compared with 9.7% in June 16. Excluding the payment of the 2016 Final Dividend (net of the Dividend Reinvestment Plan), CET1 increased 40 bps in the first quarter, primarily driven by organic capital generation of 48 bps which is substantially stronger than the Post Basel III 1Q average of 21 bps.

There was no capital benefit from asset disposals in the quarter.

Strong deposit growth and solid progress with the Group’s term wholesale funding plan has contributed to a further improvement in the Group’s liquidity and funding position. The Group’s average Liquidity Coverage Ratio (LCR) for the quarter was 137% (proforma 132% if adjusted for the $6.5 billion reduction in the Committed Liquidity Facility effective January 2017). ANZ’s Net Stable Funding Ratio (NSFR) is estimated to be in excess of 108%.

The Basel III leverage ratio is 5.1%.

Since the start of FY2017, ANZ has signed agreements to sell its 20% stake in Shanghai Rural Commercial Bank (SRCB), the UDC Finance business in New Zealand and ANZ’s Retail and Wealth businesses in five Asian countries. The transactions are expected to complete in the second half of FY2017 and 1H2018 subject to regulatory approvals. For the purposes of comparison, if the earnings from the businesses being sold were to be excluded from Cash Profit performance for 1Q17 it would show an increase of 33% (+31% including).

In FY2016 a number of actions were classified as Specified Items which formed part of the Group’s Cash Profit. This classification assisted investors and analysts to look through the impact of strategic initiatives to determine underlying business performance trends and included the disposal of Esanda, restructuring charges, a write down of the valuation for the investment in AmBank, and accounting methodology changes. In 2017 the classification of Specified Items will be limited to the impact of disposals.

These transactions outlined above will boost ANZ’s APRA CET1 position by ~$2.7 billion or ~70bps upon completion further improving ANZ’s capital flexibility.

Here is ANZ CEO Shayne Elliott speaking to BlueNotes on video after the announcement.